FX Daily Strategy: N America, Jun 17th

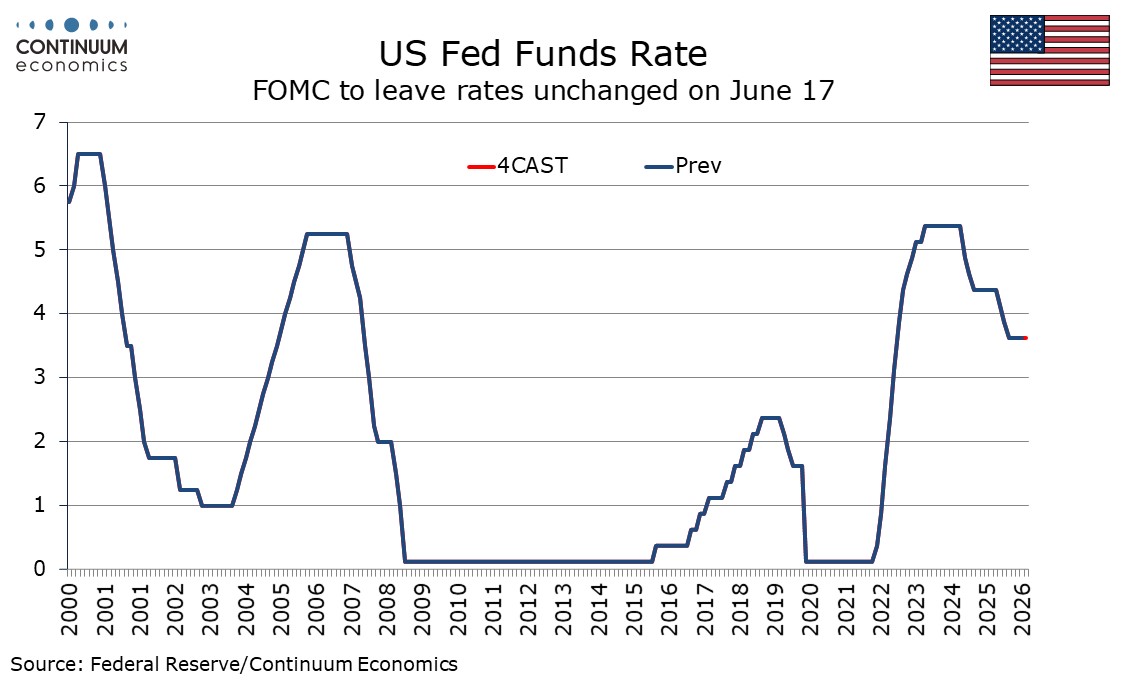

FOMC Dropping the easing bias

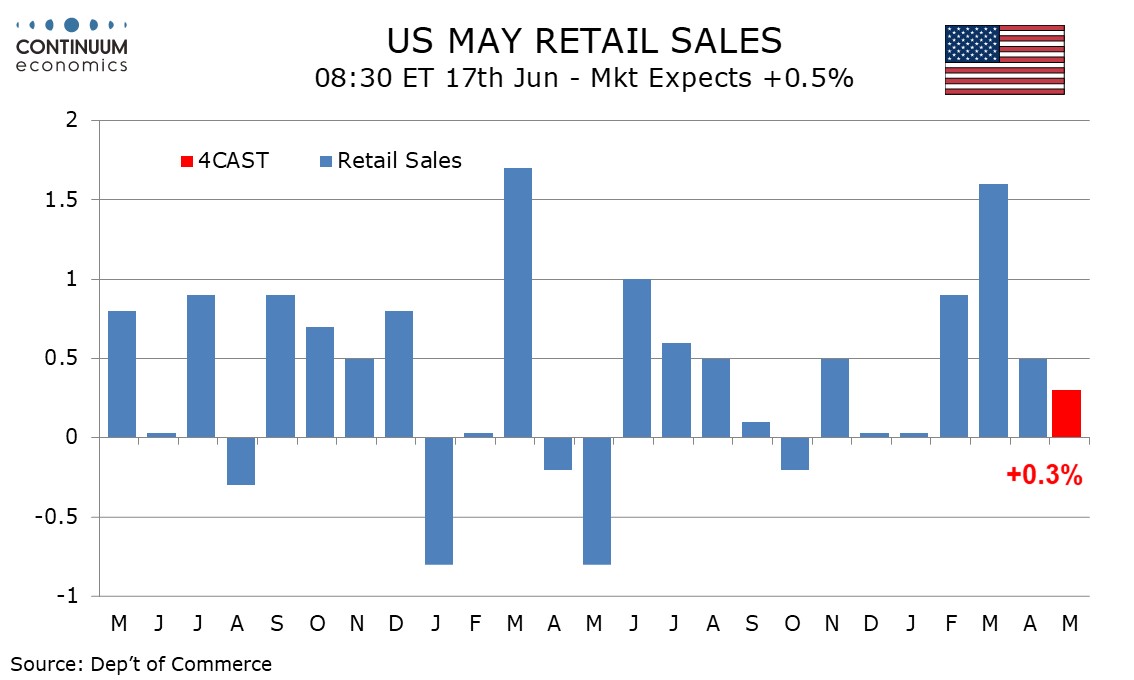

U.S. May Retail Sales a pull back

Riksbank Mild Tightening Bias to Persist But Not Exercised

UK CPI Peaking

The FOMC meets on June 17 and while a change in the Fed Funds target range from the current 3.5-3.75% is unlikely, the statement is likely to drop the easing bias. The median dots are likely to get a little more hawkish with a hawkish skew in the detail, with inflation forecasts, even ex food and energy, likely to see a significant near term upward revision. The post-meeting press conference will be of particular intertest, being the first from incoming Chair Kevin Warsh. He is likely to be less hawkish than some will feel upgraded inflation forecasts would justify.

The last meeting on April 17 saw three hawkish dissents, from Cleveland Fed’s Beth Hammack, Minneapolis Fed’s Neel Kashkari, and Dallas Fed’s Lorie Logan, who wanted to drop an easing bias. Governor Stephen Miran dissented for an easing but he has now left the FOMC. Then Chair Jerome Powell hinted at the press conference that others were inclined to drop the easing bias, and minutes from the meeting stated that many were. This is likely to happen at this meeting, though given high levels of uncertainty the statement is more likely to be open to moving rates in either direction rather than giving an explicit tightening bias.

We expect May retail sales to increase by 0.3% both overall and ex autos, but with a 0.1% decline ex autos and gasoline, which would suggest that consumers are starting to pull back as elevated gasoline prices increasingly weigh on real disposable income.

Gasoline prices increased further in May, even if May’s gain, like April’s, was less sharp than in March. While gasoline looks set to be a significant positive on prices, autos look unlikely to have much impact. Industry data shows only a marginal increase in sales, not fully erasing a modest decline in April.

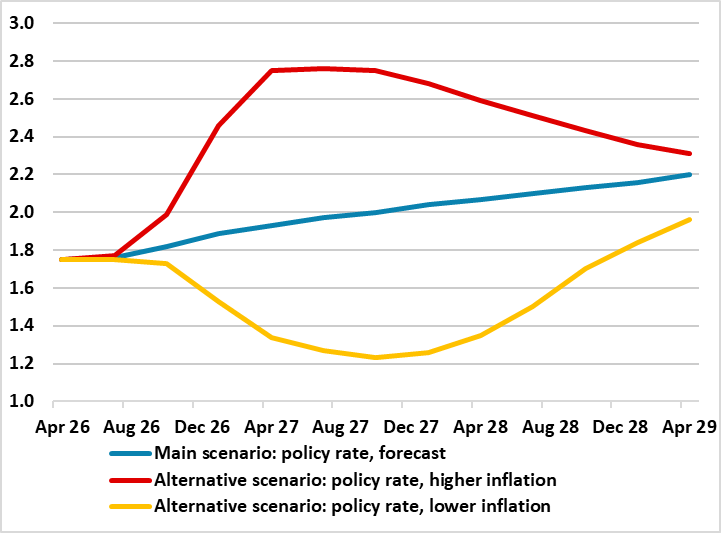

In Europe, the Riksbank meeting was largely as we expected - the tightening bias mildly reinforced, noting the risks of a tightening later in the year had increased, but forecasts that overall support the main view that policy is ‘well-balanced to leave unchanged’ amid low inflation and somewhat weaker than normal activity. Our view remains that the Bank stays on hold through this year. EUR/SEK currently more focused on the broader geopolitical and risk backdrop and that is tending to lean EUR/SEK back down in its established range of the last few months, so long as sentiment on Iran and supply chains remains improved.

Figure : Riksbank Policy Rate Scenarios

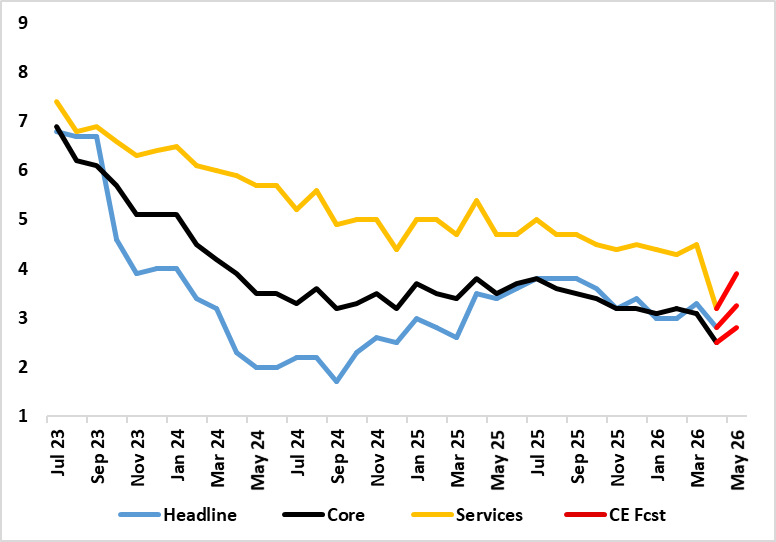

In the UK, inflation undershot expectations notably by holding at 2.8%y/y. While energy tariff increases will come through in July, the underlying data still supports our view that inflation can peak out albeit later in the year.

Figure: Headline And Core To Bounce Back?

The data helped reinforce the view that the BoE is more comfortably on hold through the summer and on our view for the remainder of the year. EUR/GBP still mildly lifting off its YTD range base but recent price action has been sterling constructive as the risk backdrop has improved and as the market has become less sensitive to the UK political backdrop, even into the byelection.