FX Daily Strategy: Asia, Jun 9th

Still a battle to head off escalation, at least Trump seems keen on an exit

Backfilling after mini risk correction, but further long shakeout still seems a risk

Dollar still seems to have two paths to gains (outperformance or risk spike)

Ebb and flow in the news continues. When Trump is the voice of reason when it comes to geopolitics (if less so the mechanics and ‘fairness’ of monetary policy), you know things have gone a bit wrong - though there is comfort to be had in how keen he is to get a deal across the line.

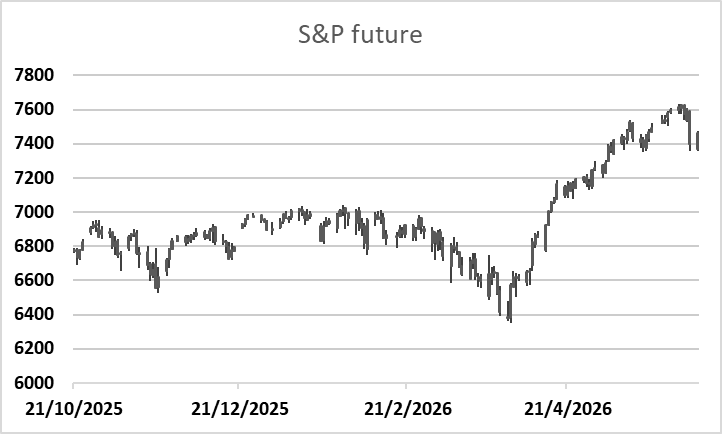

After Friday’s very-mini shakeout, there’s some backfilling and consolidation to be seen across the board in tech stocks, metals, volatility and to a lesser extent the dollar, but it is hard to view things as out of the woods. Taking a step back to look at the S&P for instance, the pullback was to the recent swing lows and shy of 23% of the April+ rally. And there’s no denying the dip buying mentality has been deeply engrained.

A fuller technical correction however does still seem the near-term risk in due course and that would be to the 7150-7000 zone 38%-50% and the latter the previous breakout area (these do frequently need to be re-tested at some point before the longer-term continuation).

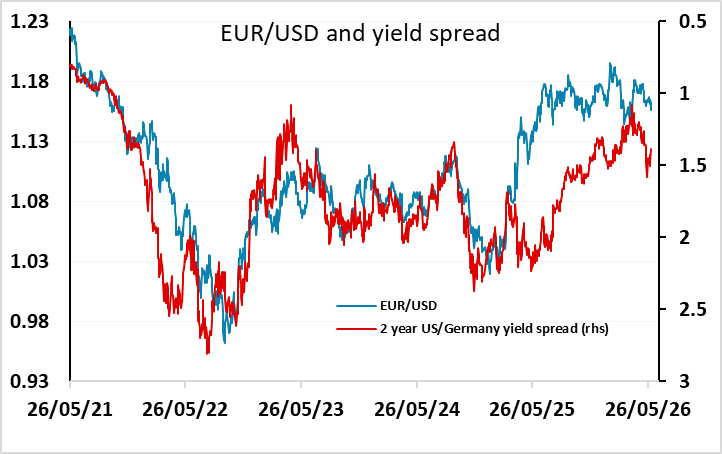

On the FX side, both sides of the so-called dollar smile (US outperformance or risk spike as dollar support) do remain plausible supportive forks in the road near-term. And in any case spreads as they stand have for a while being suggesting the likes of EUR/USD had been proving sticky on the rich side so from that perspective only partially realigning with the recent step downs.

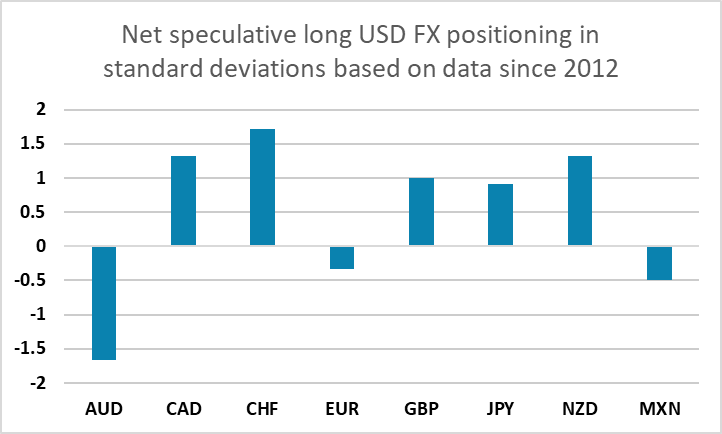

It was interesting that IMM data still continued to show EUR and more so AUD as the outliers in the broader pivot back to overall dollar long positioning so in that sense these were the counterparties with the greatest scope to fall into line.

On that pair, 1.1550/75 area now becomes support turned resistance and caps if we remain in overall dollar bounce mode. 1.1450 congestion then the 1.1410, March current year lows remain viable but may need intraday action to unwind and another trigger first.

AUD/USD has 7080/.7100 as the equivalent bounce resistance that would need to hold near-term to keep the focus on further retracement (.6950/00 congestion next lower).

The other side note from the spec positioning was that yen shorts are also now the largest for almost 2 years, albeit not huge in absolute standard deviation terms. Still, positioning is already showing a short base at the top of the tolerance area, and this is one of the factors helping to keep the pair checked at and just above the 160 figure. There’s also been a few days now where the Asia sessions looks to be running long before somewhat noisily covering late in the European morning, making for some 30-50 pip exaggerated intraday moves. Recent action has also provided a reminder that if volatility does manage a more than one session pick up, that too could ask some tougher questions of the looser carries.

Calendars are relatively light with nothing hugely significant until US CPI and ECB meetings. Tuesday has German industrial production (orders were on the soft side already Monday) in the European morning.

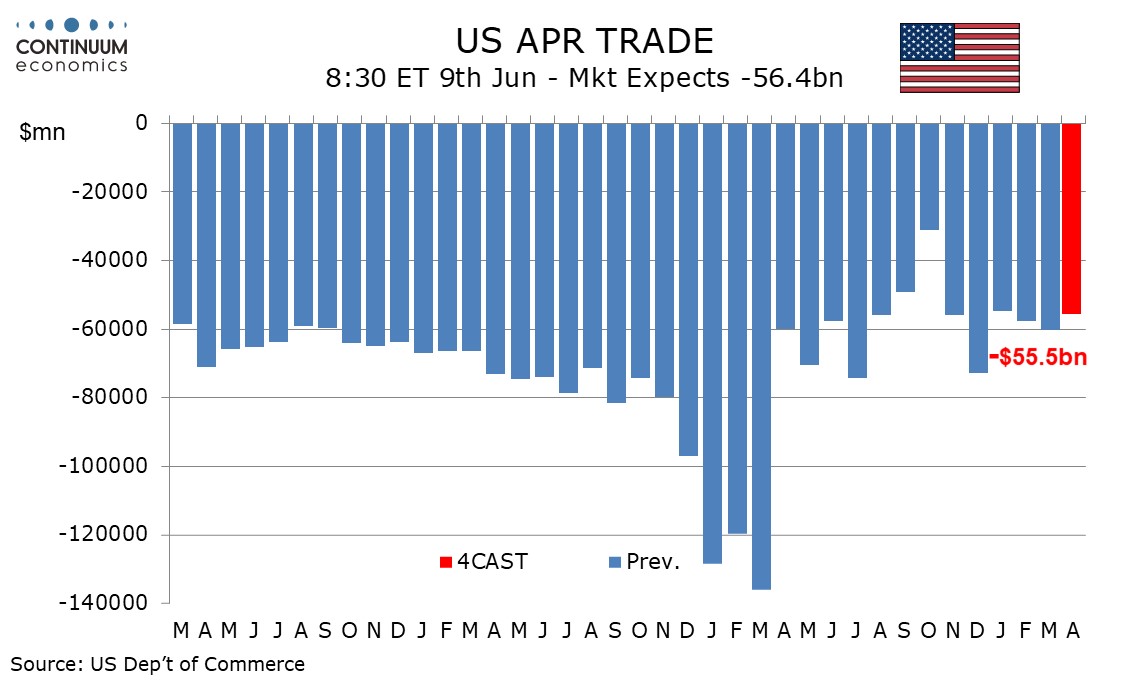

The US sees trade data and existing home sales. We expect a narrowing of the deficit to $55.5bn from $60.3bn. We also expect a 2.0% increase in May existing home sales to 4.10m