CBR Extends Easing Cycle but Slows Pace Amid Global Inflation Risks

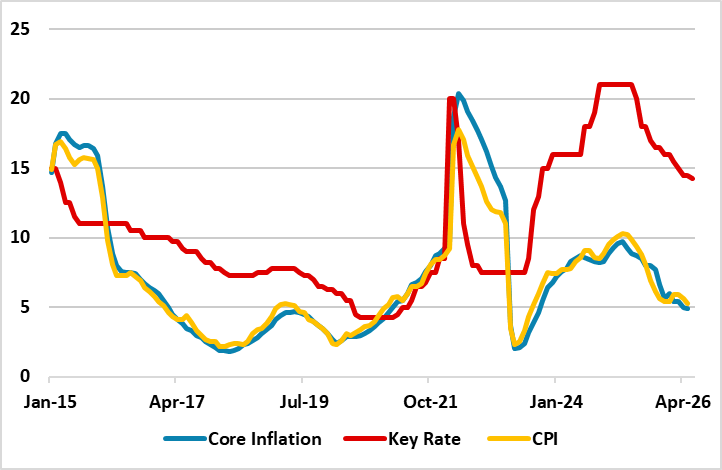

Bottom Line: Following 50 bps rate cut on April 24—driven by the disinflationary trend in H1— the Central Bank of Russia (CBR) extended its easing cycle on June 19. However, the bank opted for a smaller 25-basis-point reduction, lowering the key rate from 14.5% to 14.25% citing mounting global inflationary risks. Our end-year key rate forecast is now at 13.5% and 10.5% for 2026 and 2027, respectively, since CBR will have to keep rates high as the country need higher real yields. We think CBR will likely resume cutting rates (moderately) in Q4 and 2027 if the inflation trajectory allows and inflation expectations converge towards CBR’s forecasts.

Figure 1: CPI, Core Inflation (YoY, % Change) and Policy Rate (%), January 2015 – June 2026

Source: Continuum Economics

Following 50 bps rate cut on April 24—driven by the disinflationary trend in H1— the Central Bank of Russia (CBR) extended its easing cycle on June 19. However, the bank opted for a smaller 25-basis-point reduction, lowering the key rate from 14.5% to 14.25% citing mounting global inflationary risks.

In May, annual inflation slowed to 5.3%, driven by the lagged effects of previous monetary tightening, a resilient ruble, and moderate core inflation. (Note: The core inflation eased to 4.9% in May from 5% in the previous month). This trend was supported by improving inflation expectations; recent data showed household expectations edged down to 12.4% in June from 13% in May.

Following the MPC decision, CBR said in its written statement that pro-inflationary risks prevailed in the medium term when citing the warrant for restrictive monetary policy. CBR added that pro-inflationary risks are supported by the external backdrop of higher energy prices due to the war in the Middle East, higher energy prices domestically as refineries are targeted by Ukraine, and higher inflation expectations as wage growth outpaces productivity growth.

The CBR projects annual inflation will decline to 4.5–5.5% in 2026, aiming for a return to its 4% target by 2027. However, we still believe meeting this target range will be challenging in 2026. Persistent sanctions, the expected fall in oil prices after Iran conflict dissipates and sustained military spending are likely to prolong the disinflationary process beyond the CBR's expectations.

Our end-year key rate forecast is now at 13.5% and 10.5% for 2026 and 2027, respectively since CBR will have to keep rates high as the country need higher real yields. We think CBR will likely resume cutting rates (moderately) in Q4 and 2027 if the inflation trajectory allows and inflation expectations converge towards CBR’s forecasts. (Note: As an alternative scenario, a faster CBR easing cycle is possible in 2027 if a full scale peace deal is signed in Ukraine relieving the Russian economy, and President Putin could request a domestic demand boost as military spending slows).