Norges Bank Review (Jun 18): Higher Rates Then Down?

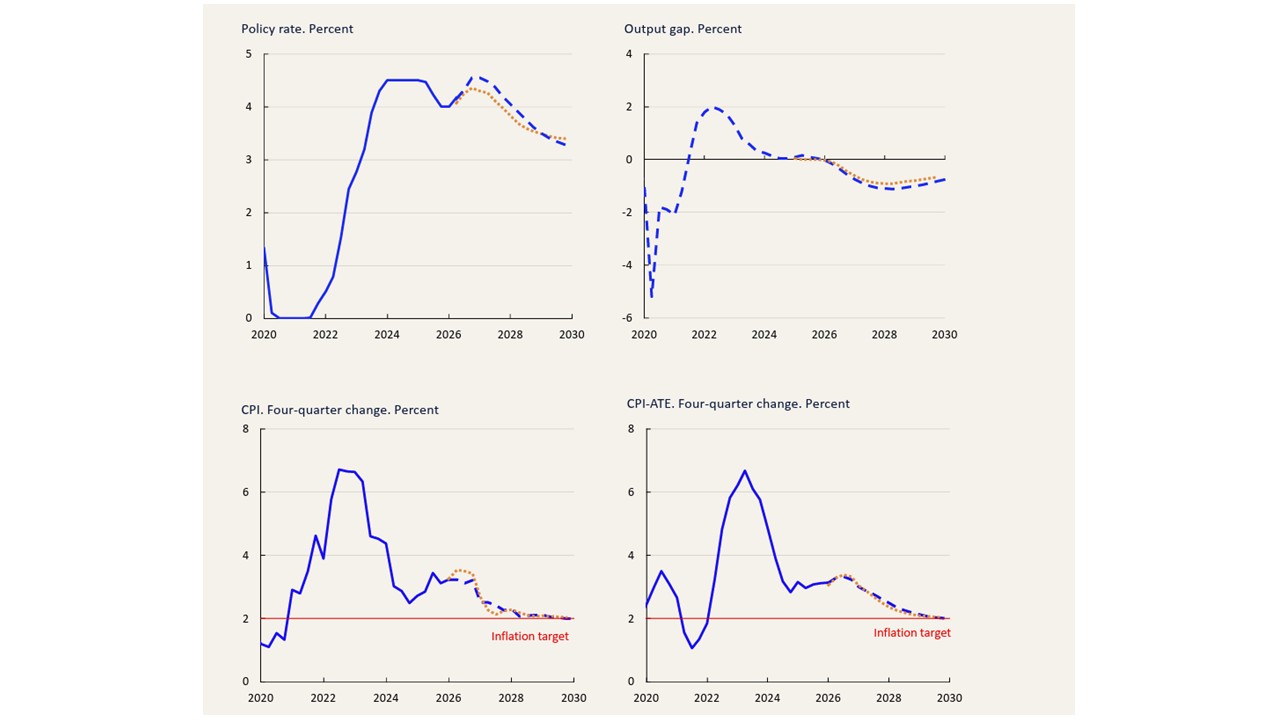

The June Norges bank statement had a hawkish bias with a higher policy rate profile than in March MPR (Figure 1) and concerns voiced again over persistent domestic inflation pressures. The Norges bank appear ready to move in September or November. However, the Iran/U.S. deal impact on energy prices could mean a downward inflation revision in September and mean no hike in 2026. Additionally, the nominal policy rate is close to twice the Norges Bank’s estimate of neutral and slowing the economy and creating an output gap, which we feel will deliver 2027 rate cuts.

Figure 1: Norges Bank Policy Outlook Suggests Short-Lived Hikes

Source: June Norges Bank Monetary Policy Report

Norges bank remain ready to undertake one final 25bps hike in September or November over concern on domestic inflation persistence. This was a hardening of the statement compared to previous meetings, which leaves the impression that the Norges currently want to hike. Even so, we think that the inflation persistence arguments, that actually prevented faster easing before the Middle East conflict broke out, are overdone and that even with no hike at all, the current Norges Bank policy stance is very restrictive. Even on its own assessment with the current policy rate is 1.5 ppt-plus above neutral despite (at worse) a mixed inflation backdrop.

Given the lags in such policy moves taking effect, this questions the need for such a temporary hike to 4.50% other than to underscore hawkish reputation. As a result, we feel the Board is being excessively hawkish.

Moreover, as suggested above, we question the extent to which the inflation forecast made by the Bank in the June report are realistic with the Board CPI-ATE now seen averaging 3.2% end 2026 and 2.6 % end 2027, Some of the forecast this year is due to the apparent fact that CPI data have been higher than expected, but is this an indictment of the Board’s forecasting as despite its assertions to the contrary underlying inflation has been reasonably well behaved. Indeed, underlying inflation short-term dynamics are far from unfriendly especially if food is excluded from the targeted CPI-ATE measure so as make a more familiar core measure.

Given Norges Bank hawkishness, we remain far less confident about the extent of any eventual easing, and our forecast is deferred into 2027. A 2026 hike is possible to 4.50%, but a rethink could stop this. Additionally, we envisage some 100 bp of cuts through next year. At 3.25%-3.5%, that would still leave the policy rate still at the end if next year well above its own estimated nominal neutral rate of just over 2%.