FX Daily Strategy: N America, Jul 9

FOMC Minutes and Trump Iran rhetoric to be digested

Oil and wider mkt left navigating the dangerous line between rhetoric and breakdown

FOMC Minutes last night failed to deliver any huge surprises. While a few participants did hint at a tightening bias, mildly, the spine of the debate centred on two competing scenarios for inflation and so policy calibration. The main message then was around scenario-dependent policy, uncertainty, and a division of biases on either side.

As has been the persistent theme for months, Iran again very much sets the context within which the text will have to be placed, especially with the discussion underscoring the importance of developments here, along with AI driven demand, for the near-term outlook.

Regarding geopolitics, attention turns to Iran's next comments if and when they turn up. On Trump's side, he already looks to be steering towards the usual good cop bad cop approach, with the latest suggestions that Iran called and wanted to make a deal - whether true or invented, it does suggest a quick pivot back to de-escalation again.

Oil, many times bitten, is erring to the optimistic version so far albeit encouraged to trim back from the $70 base on Brent. If agitations become a bit more embedded, then 38%~ back on the last leg down would be around $83 ½ or just below. $80-81 is also big figure and prior high/low area. So this zone marks the main limit on what would be corrective action. The lower side of this band has so far contained the initial scare.

USD/JPY remains its own kind of echo chamber where everything seemingly supports up (until it doesn’t). The Iran flare-up and oil bounce offering support to the pair, even though the prior $50 drop did nothing to do the opposite. Likewise, risk on lifts, while tougher equity days seemingly don’t depress. So it remains a vibe driven market that is currently showing few inclinations to change even if it could do so in a hurry at some point.

EUR/USD remains seemingly a bit trapped immediately around 1.14~ both by competing pulls and by a sequence of large expiries all in the vicinity over the remainder of the week. Upside has been in the 1.1450~ area and so far this continues to hold the relief moves. The dollar is generally a little long in the spec market on most pairs (other than euro) and that is tending to give the dollar a bit of a current top-heavy environment to work with.

In terms of Thursday’s calendar, the early interest comes from the Minutes to the ECB rate hike decision meeting, although there are probably few surprises to be had here given the way the decision was so well signalled prior and then dissected at the presser.

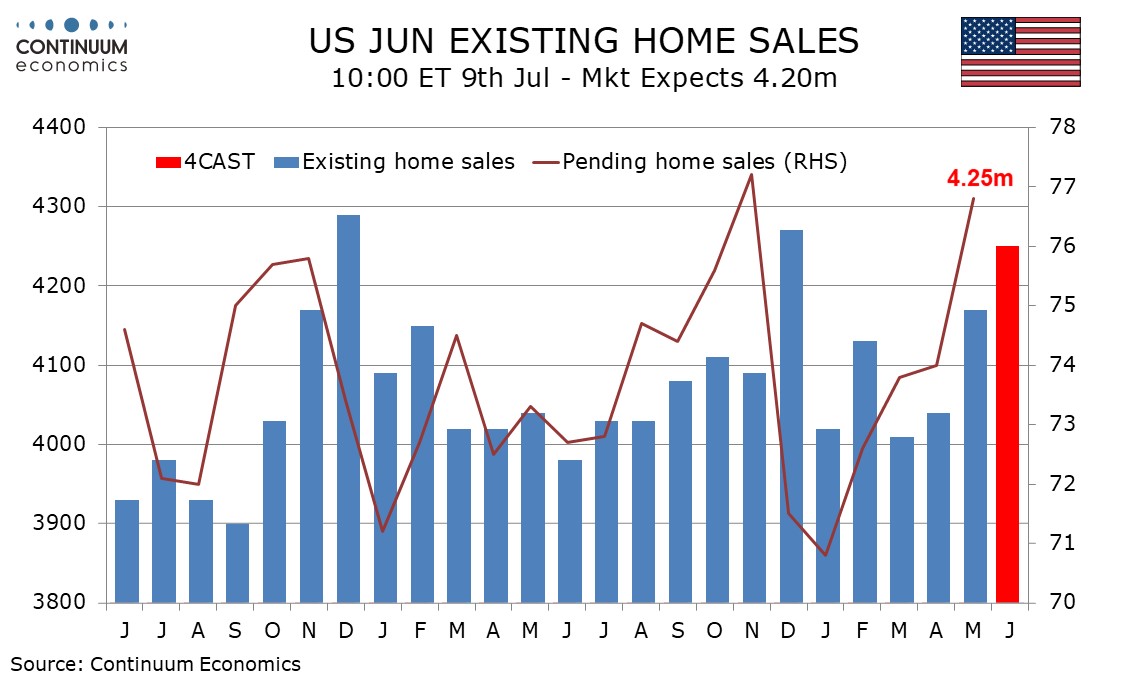

In the US, Thursday sees weekly initial claims and June existing home sales, which we expect to rise by 1.9% to 4.25m.