South Africa MPC Preview: Close Call on May 28

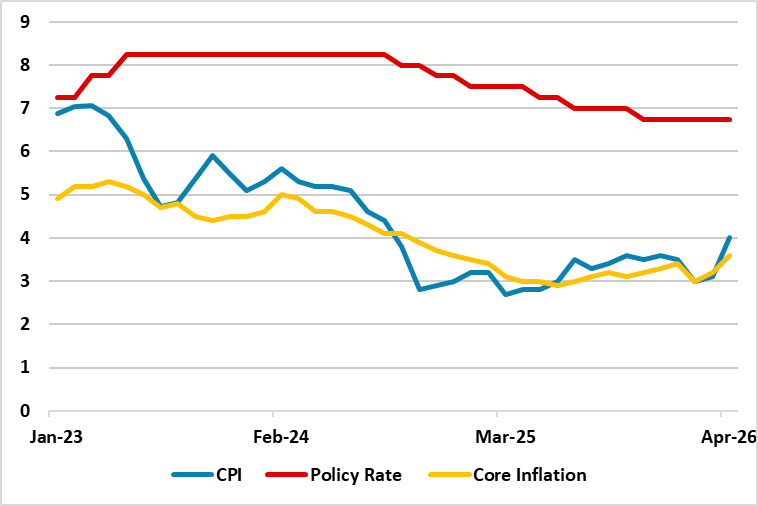

Bottom Line: Taking into account that annual inflation increased to 4.0% y/y in April due to higher energy and transportation prices, we think South African Reserve Bank (SARB) will likely consider hiking the rate by 25 bps to 7.0% during the next MPC scheduled on May 28 given plenty of upside risks to inflation including Iran conflict, surging costs and volatility of ZAR. The SARB will also be concerned with second-round effects from fuel-price inflation, as suppliers will pass rising fuel-related input costs onto consumers. The upcoming interest rate decision remains a close call since the SARB may hold the policy rate at 6.75% to assess incoming May/June inflation data and developments in the Iran conflict.

Figure 1: Policy Rate (%), CPI and Core Inflation (YoY, % Change), January 2023 – April 2026

Source: Continuum Economics

SARB’s MPC will convene on May 28, and the third key rate decision of 2026 will be announced. We foresee SARB will likely hike the key rate by 25 bps to 7.0% due to inflationary pressures despite the decision will be a close call. The SARB will likely focus on second-round effects from fuel-price inflation, given that suppliers are poised to pass higher input costs onto consumers. This pressure, combined with April's inflation uptick, remains the central bank's primary concern.

According to Stats SA’s announcement on May 20, South Africa’s inflation edged up to 4.0% y/y in April reaching its highest level since August 2024. This surge was driven by rising energy costs, a volatile ZAR, and climbing transportation and fertilizer costs resulting from the conflict in Iran.

South Africa’s inflation outlook remains highly vulnerable to the Iran war. As a net importer of petroleum products, the domestic economy is acutely sensitive to international energy market volatility, a risk underscored by an 18.2% m/m spike in the fuel index in April —the largest monthly surge recorded since 2008.

Conversely, slight m/m decline in April's core inflation could give the SARB room to hold the policy rate stable at 6.75%. Core inflation printed at 0.5% m/m (3.6% y/y) in April, slowing from the previous month’s 0.8% reading. The SARB may choose to monitor how May and June inflation data, alongside the Iran conflict, evolve before considering a rate hike decision on May 28.

Under current circumstances, we envisage cautious SARB proceeds carefully on interest-rate adjustments, given plenty of upside risks to inflation. We think the Iran conflict will remain a critical factor for the South African economy in the near term. Returning to the 3% inflation target range will likely be a (very) slow process unless the conflict loses momentum, geopolitical risk premiums dissipate, and oil prices decline in line with shifting market dynamics.