FX Daily Strategy: Asia, Jun 24th

Dollar remains firm, testing or clearing various levels

Focus on position corrections, Fed re-pricing spillover, and equities

AUD CPI, IFO and US new home sales on the schedule

The dollar continues to rally across the board with most pairs either at or through important resistance levels. EUR/USD eventually took out support around 1.14 +/-, and if this holds, it can extend next to the 1.1355 Fibonacci retracement.

Similar USD/NOK, pressured additionally by the Iran unwind, is testing next up to the big highs around 9.8~

AUD/USD has made the break and is now accelerating for the next support at 0.69 and the March lows below that. NZD already at lows that threaten the full YTD retracement.

We discuss in the FX Outlook the broader backdrop to this, encompassing the current market Fed re-pricing, commodity position corrections, and other background forces (from El Nino to more noise in equities). We expect this broad trend to remain in place over coming weeks before fading later in the year, but with many cross-currents in play in terms of scale and timing of moves.

On the yen, some signs that cross driven action is at least just about dominating, if only stemming, USD/JPY so far amid the dollar driven action. It would likely need more impulsive setbacks in equities - after corrective activity and rotation kicked in yesterday but with so far limited spikes in volatility - for this to be gaining additional force. It does seem to be providing stronger capping action at the very least along with the ongoing background focus on intervention strategy going forward. USD/JPY needs to be back below 161 near-term to be looking flat/lower though.

As for Wednesday, Asia focus is on Australian CPI where the market looks for measures to tick up by 0.1pp. Market pricing currently hedges half way to a further hike but there are some big influences currently playing out that should carry more wiehgt than one inflation print unless its a huge surprise.

Germany has IFO business sentiment with some improvements expected on the back of geopolitical improvements.

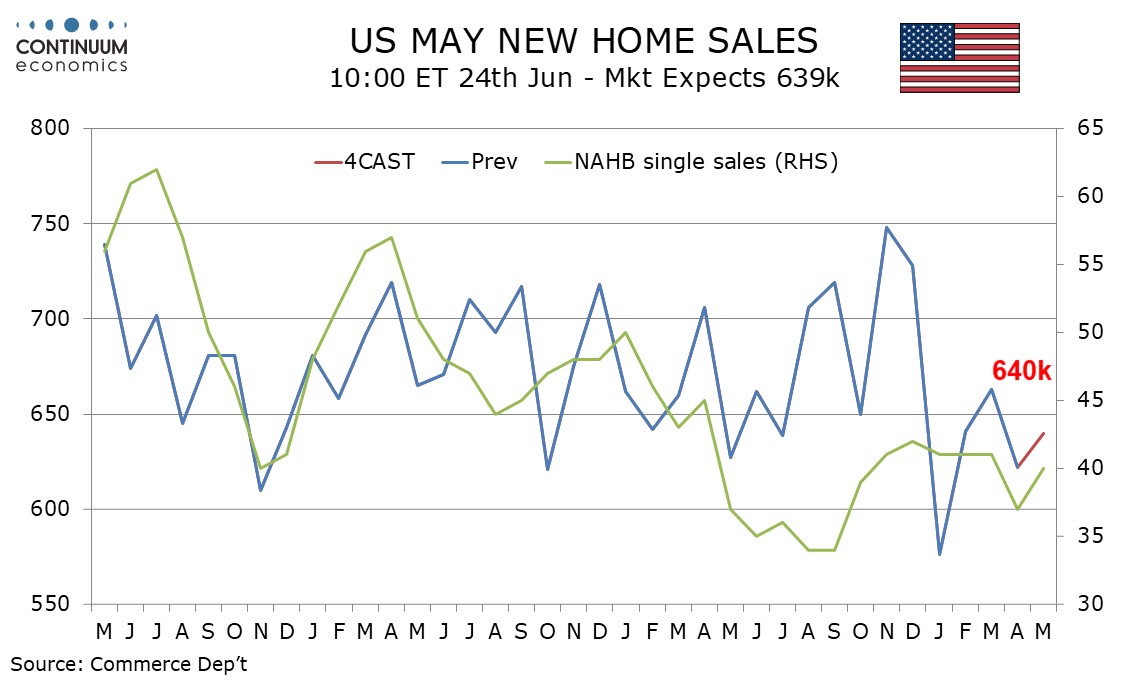

In the US, we expect the Q1 current account deficit to rise to $208.8bn from $190.7bn in Q4 and a 2.9% rise in May new home sales to 640k.