FX Daily Strategy: Asia, Jun 18th

FOMC lives up to the hype, dollar breaks higher

Otherwise focus turns to the UK, with data, BoE and by-election.

SNB seen unchanged and CHF comments to be ignored unless escalated

Some notable events on the schedule today, but much of the agenda is going to be set digesting the FOMC and the price action that has followed.

Viewed through one lens, the composition of the dots made for a far more equivocal and divided picture on the Fed than you might get from the headline dot median forecasts alone. And even on the main (but less than half the board) view the rate forecasts only barely validated what was already in the money market heading into the meeting. From this view point, the Fed can still remain on hold this year, albeit staying 'higher for longer', if data does start to cool on the inflation side as supply chain restrictions hopefully abate.

All that given, the market reaction and resulting short-end spread moves clearly reinforce the US outperformance narrative and psychologically play to the current market dalliance with a return to 'US exceptionalism' and potentially more lasting dollar near-term support than previously delivered by just the recent haven bid. In other words, with the hoped-for Iran exit-ramp, the dollar then flips to the opposite side of the 'dollar smile' to renew an albeit different bid.

On EUR/USD, break of the 1.15~ lows brings the bigger 1.1450/10 base from March/early April back into frame. Cable similarly has 1.32/150.

USD/JPY meanwhile is being 'speed-checked' into the previous highs, clearly with one eye on elevated intervention risks. Clearly, MoF have a tricky decision to navigate now as broad-dollar-driven gains would be hard to fight single handed. Crosses have also actually set back, as have equities, if so far modestly. MoF may want to hang back then until and unless the yen starts showing speedy breakout action and an acceleration in the existing short base to squeeze.

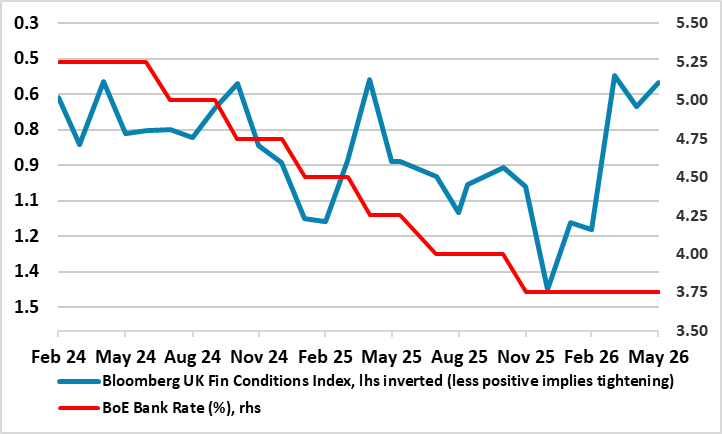

Outside of that dominant driver, Thursday sees focus partially shift back to the UK, with the Labour market data, BoE decision, and later the count for the political important by-election.

On the former, HMRC data may continue to show slowing in employment while pay data may show fresh slowing from its recent retreat. Data is then unlikely to offer any challenge to the view, supported by recent CPI, that the BoE is not just on hold this meeting as universally expected, but likely reiterating that it sees risk-reward favouring an ongoing pause.

Although there may be some split on the board, the meeting should support the market’s shift towards assuming on-hold through the summer and receding risks of a hike later in the year (our view is on hold throughout).

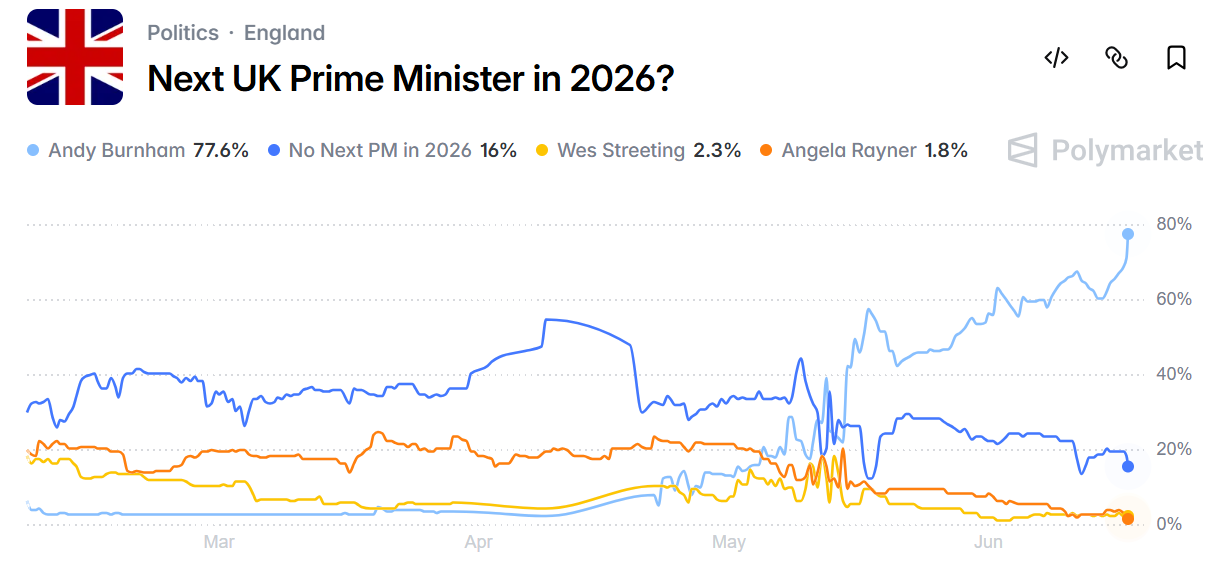

Regarding the byelection, most polls suggest a clear but modest lead for Burnham into the vote. Interestingly, his own popularity has dropped notably since mounting the leadership challenge though remains well ahead of his rivals including Starmer.

For markets, his victory in the seat and then likely victory in the eventual leadership contest is very much priced in. Sterling price action into the vote has also been pretty constructive and while EUR/GBP has been respecting its YTD range again and so mildly lifting off the recent base test, it seems unlikely that events will offer a strong negative sterling trigger.

Indeed, so long as geopolitical improvements remain in place and risk tone generally improved, sterling typically stands to gain from the reduced macro pressure and pro-cyclical bias.

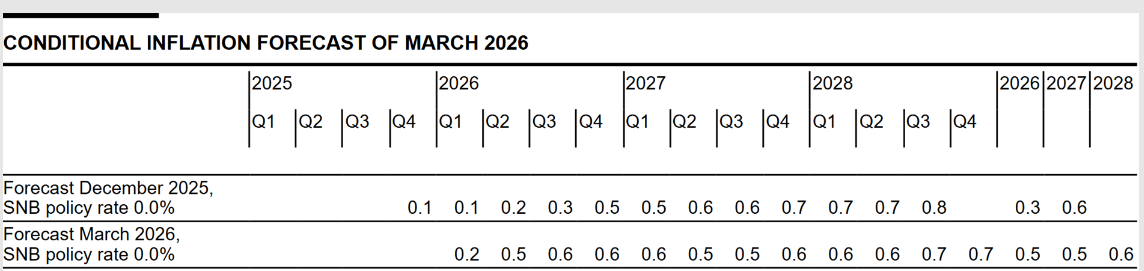

The SNB is a lesser focus with a clear unchanged outlook and little change expected in its forecasts.

There will be some likely reference to watching CHF strength and being able to willing to respond. But these comments are well aired now and are likely to be ignored without any material escalation in tone.

EUR/CHF range recovery has been capped by 0.9250 and has tended to roll back since the referendum passed off without event. 0.9150-00 is the recent limited range downside.

Interestingly, neither CHF upside nor JPY downside has shown a huge amount of inclination to shift from their respective contrasting Iran positioning as yet. Dollar-driven action has now taken over at present so it will be interesting to see if this terms-of-trade and safehaven reversals can start to get a look in.