FX Daily Strategy: N America, Jun 4th

Tight ranges hold, though mood still defensive

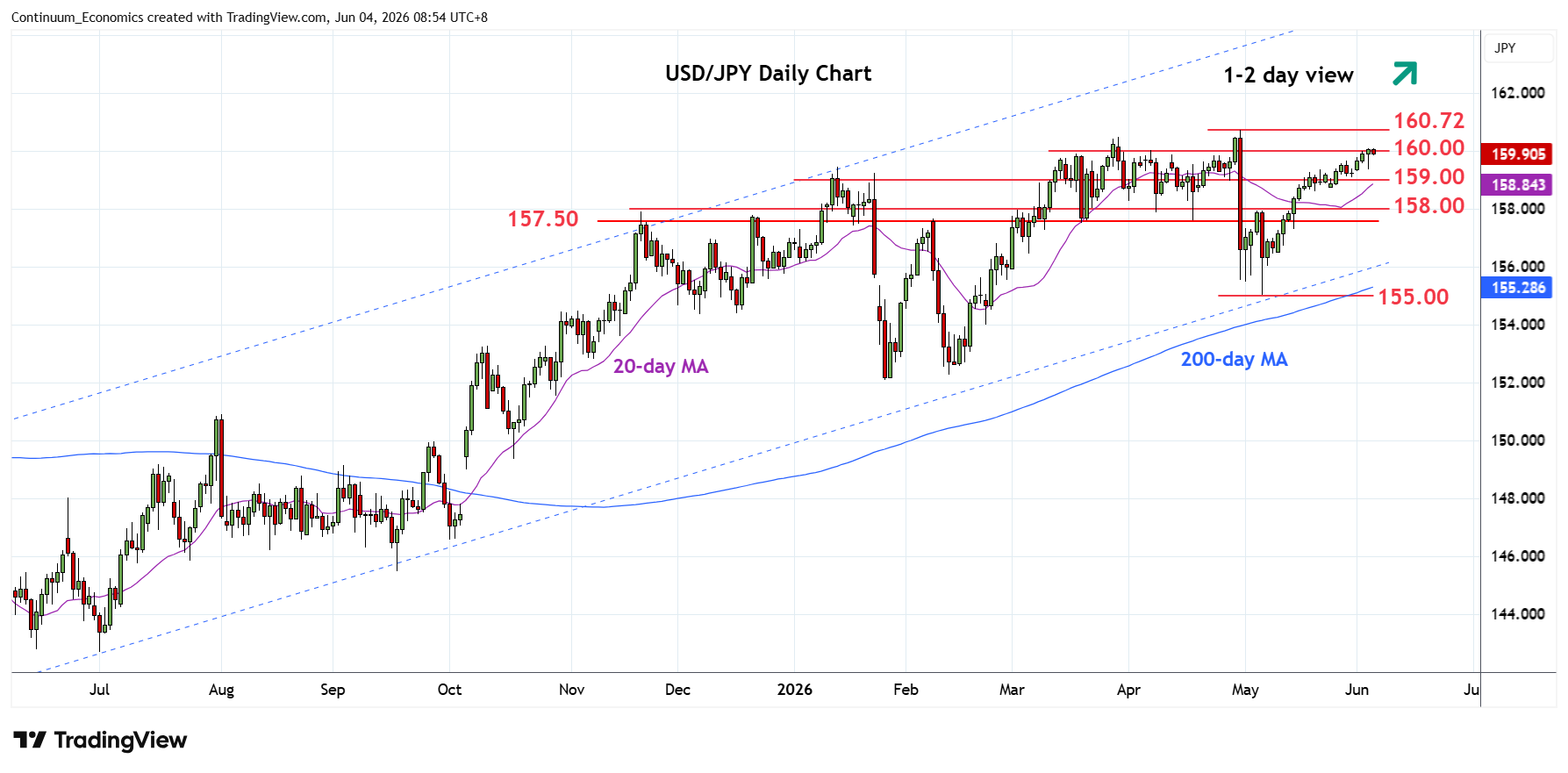

USD/JPY dancing on the edge of 160. Greater scope for intraday noise and spoofing

Focus turning to US payrolls, mkt bias to upside

It’s one of the functional ironies of the current market that the inherently volatile and high-risk background environment is tending to leave the market trapped rabbit-in-headlights like into declining volatility, EUR/USD 1mth for instance sapping nearer towards the bottom of the post 2020 range. This should be brewing an eventual breakout move but it’s a tough directional bet in a fickle environment.

As things stand, it’s the support at greater risk than resistance and EUR/USD could attempt to sustain its look below 1.16 but even then, next support comes in around 1.1550. The market bias is starting to nudge more towards downside protection as recent events have added to the sense of jeopardy while pushing back the timing of resolution. Market have also got wary of reacting too much to generic Trump comments on deal optimism - again suggesting chances of a weekend deal if it's going to happen - without this being backed up by Iran or paperwork. All that given, current trade is still always a headline away from turning. For now, the latest Israel-Lebanon ceasefire has checked the oil back up and the dollar lift, but the mood remains wary nonetheless.

USD/JPY is seemingly mustering itself for another go at 160, though intraday volatility here is on greater show - albeit partly of a slightly spoofy nature as the market sees mini bursts of abrupt positional adjustments before recovering.

MoF may be reluctant to ‘hold back the sea’ if price action remains broadly dollar led and might be willing to see if the market self-police a temporary stretch to 160.70~ to even 161. Any breakout that draws more momentum-based yen shorts in would, however, likely trigger more of a response. MoF is likely to consider a more mixed strategy going forward including comments, rate checking, and token visible presence alongside the heavier action to keep the market guessing.

In terms of the calendar, Thursday is a relatively light day ahead of the week’s key data release in payrolls on Friday. In Europe, the UK construction PMI tends to be ignored, but the latest further sharp drop to 6 year lows was quite notable and at the margin plays to the BoE's cautious stance.

Somewhat contrasting CPI prints elsewhere with Swedish picking up, though remaining below target, and Swiss remaining very weak, keeping the SNB not a great fan of CHF strength.

The US has the usual weekly initial claims prints.

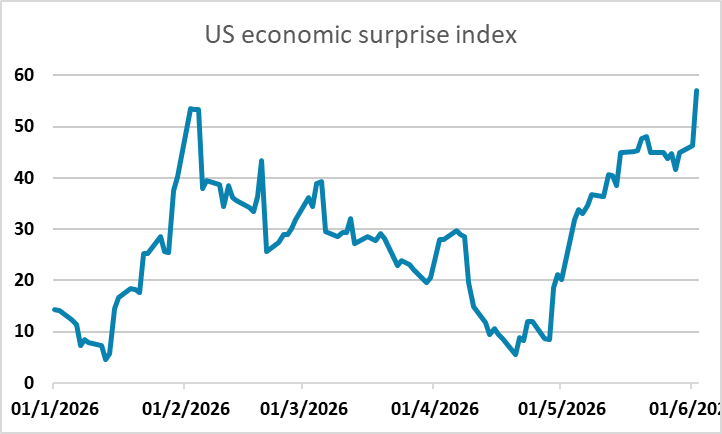

Focus starts to turn to Friday. In the build-up, the market is probably inclined to skew towards upside surprise from the key Friday payrolls release simply based on overall data and surprise trend and the fact that ADP is being assumed to post a modest (if normal) outperformance to the consensus. Subject to the dominant Iran developments that may tend to incline towards some pre-emptive dollar support in the runup.