FX Daily Strategy: Asia, Jul 17

Slate of U.S. Data

DXY Leaning lower in consolidation

Would Not be As Important As Middle East

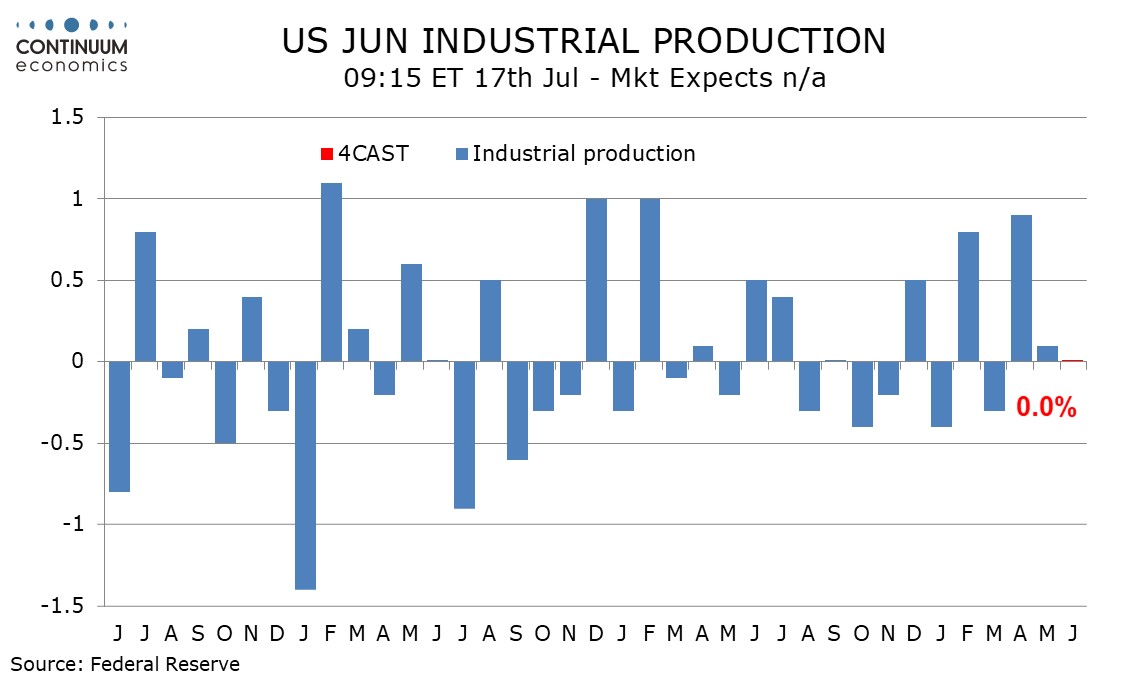

We expect an unchanged June industrial production outcome with a marginal 0.1% increase in manufacturing. This will be a second straight subdued month but still leaving a healthy Q2 given a strong increase in April. June’s non-farm payroll showed a decline in aggregate manufacturing hours worked after a flat May, though with most manufacturing indicators still positive we expect a 0.1% increase in manufacturing output after a flat May. Output usually outperforms aggregate hours given productivity gains.

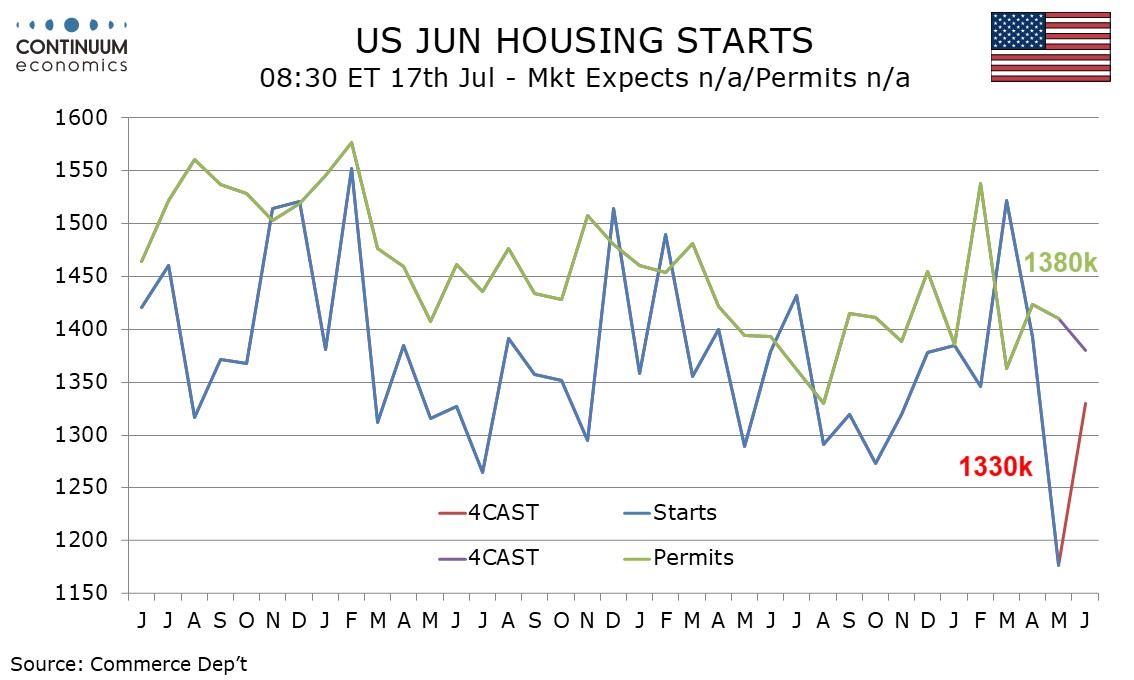

We look for June housing starts to bounce by 13.0% to 1.33m to correct a sharp 15.4% plunge seen in May, with most of the move again due to the volatile multiples component. We expect permits to suggest a modestly negative underlying trend, falling by 2.1% to 1.38m. May’s housing starts plunge was largely due to a 40.2% drop in the volatile multiples sector, which we expect to correct higher by 52.5% in June, though June’s level of 450k would still be down from April’s 493k, if up from 295k in May. For single starts we expect a marginal 0.2% decline to follow a 1.9% drop in May.

On the chart, DXY is leaning lower in consolidation following rejection from the 101.30 congestion. Below the 101.00 level threatens pullback to strong support at the 100.64/100.50 area. Daily and weekly studies have turned lower from overbought areas and suggest scope for break here to extend the late-June losses towards the 100.20, 38.2% Fibonacci retracement, then the 100.00 level. Meanwhile, resistance is lowered to the 101.00/30 congestion area which should cap corrective bounce and sustain losses from the 101.80, June current year high.

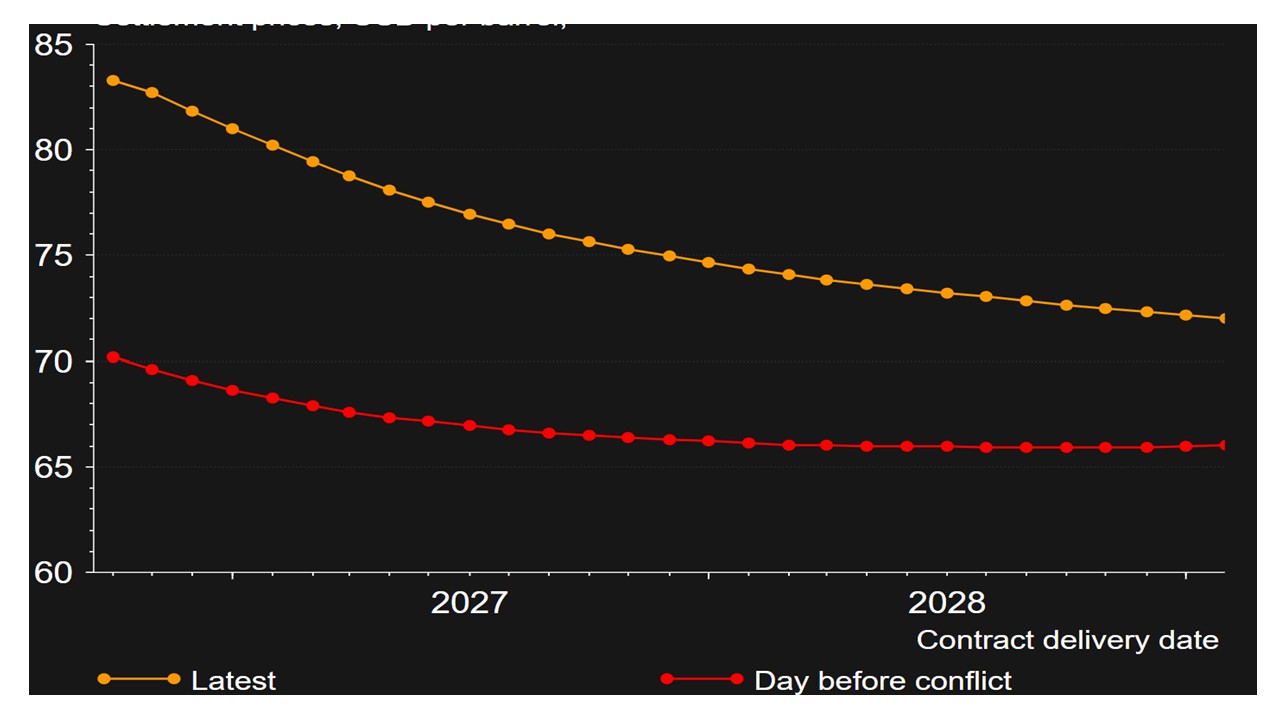

Figure: Brent Futures Curve Start of Conflict versus July 14 (USD)

Our baseline remains that the MOU will hold and that the Strait of Hormuz will reopen. Iran can be pressured economically by the U.S. naval blockade being re-established. Additionally, President Trump loves to escalate to de-escalate to get a deal, while the Republicans are under pressure before the mid-term elections for the Iran war worsening cost of living problems – gasoline could be heading back above USD4, with the latest bounce in oil prices. It is also noticeable so far that Iran attacks in the region have been focused on U.S. military bases and have not extended to hitting energy infrastructure. This is a 60% probability scenario, with WTI forecast at USD80 by end 2026.

Our alternative scenario is that the Strait continues to close intermittently and WTI by end 2026 at USD85. Iran leadership appears split over the MOU with the U.S., with hardliners wanting to ensure that a southern route around Oman is not established and this was the cause of the recent escalation. Additionally, the fog of war could mean a military escalation. In the 1987-88 tanker wars, Iran hit a U.S. warship and prompted the U.S. to escalate by hitting Iran including oil fields.