FX Daily Strategy: Asia, Jul 7

Dollar steadies, risk steadies, summer slowdown may be here

USD/JPY recoups - recovery time seems proportionate to scale of the drop

Thin calendar, Minutes and RBNZ still the later highlights

Just a slight sense of the market entering the summer doldrums. At the moment at least, this seems to be favouring another victory for low volatility - and an attempt to reignite some low volume melt up - rather than any belated ‘sell in May’ type summer action. That can change of course, but if trouble is brewing, it seems like we are waiting more for the autumn storm season this year than a summer exodus.

The market also seems to have absorbed the payrolls disappoint and come back round to the reality discussed in the weekly: still trend US outperformance and the remaining dollar interest rate spreads still being support for the dollar at present. Price action on EUR/USD therefore currently looking like capped sideways action. 1.14 the pivot in a 1.145-1.135 very short-term zone.

USD/JPY’s recovery has been alarmingly swift, as far as MoF are concerned at least, though this does seem a case of the less hard they fall the quicker they bounce. With the US holiday out the way, the market seems to have snuck back out again. There’s something a bit Gann square like about the recoveries seen so far in recent months on both MoF intervention and self-generated smaller scare drops. If the recent parallels hold, then the setbacks we saw last week may take until mid-month to fully unwind after making back most of it – in other words, a period, if proportionately shorter one, of consolidation back in the recent top.

In terms of the calendar, Tuesday is a fairly thin one - Japan has household spending data, Germany industrial production, and UK Halifax house prices.

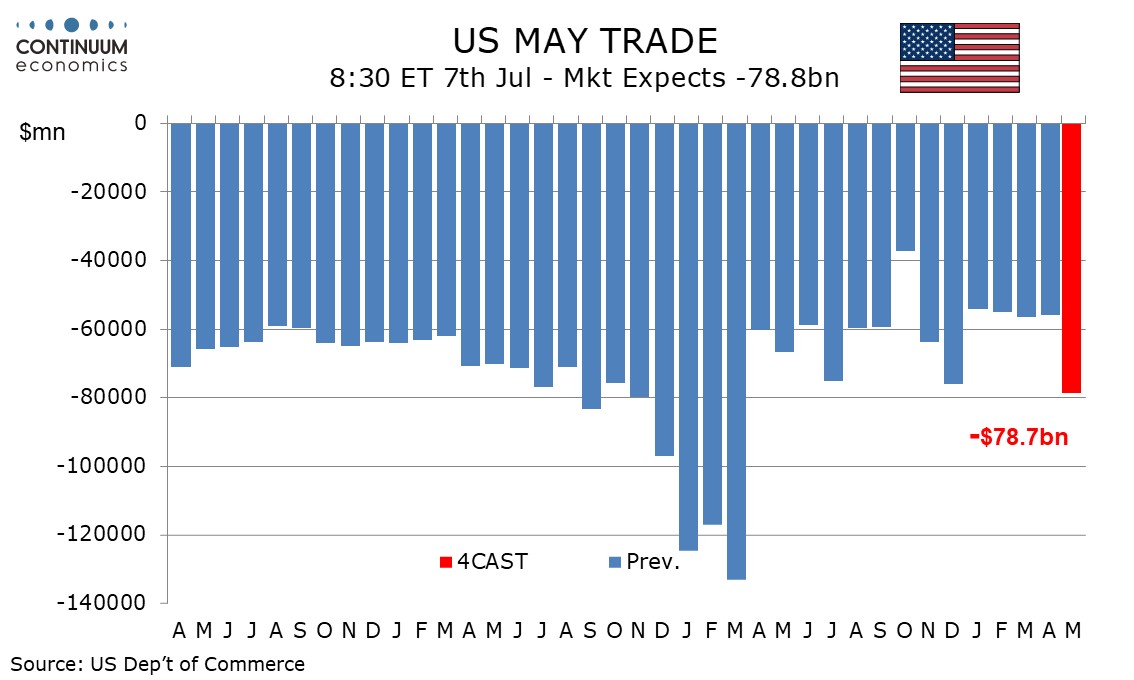

In the US, we expect a May trade deficit of $78.7bn, up from $55.9bn in April and the widest deficit since a pre-tariff record of $133.0bn in March 2025. We expect a 3.4% decline in exports after four straight gains and a 3.1% increase in imports, which would be a fourth straight gain.

Canada also sees May’s trade balance and June’s Ivey manufacturing PMI.

Focus for the week remains the Fed and ECB Minutes and the RBNZ. The latter has invited some NZD profit-taking / squaring into the event, having had a decent run up last week. From here it comes down to how much of the rates curve the Bank decides to validate. A tightening-path hike and the recovery back into range will likely be recouped. No change would be a hit given the market is fairly heavily skewed towards a move, if with 20% tail risk of unchanged.