FX Daily Strategy: Asia, June 3rd

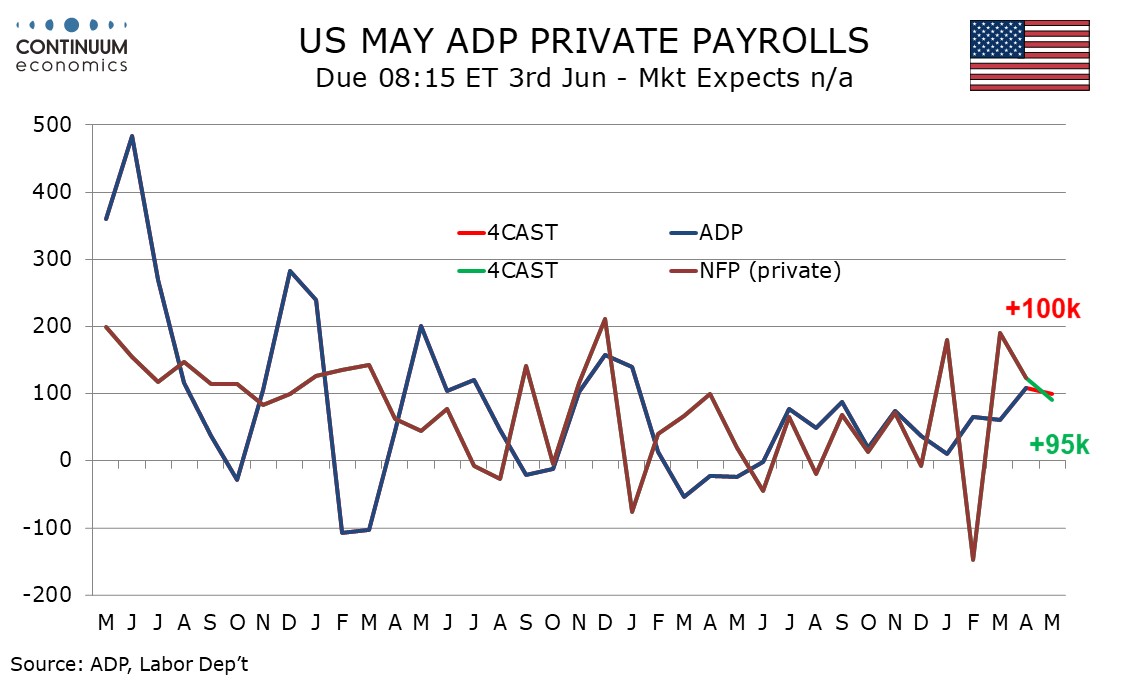

U.S. Weekly ADP data remains firm

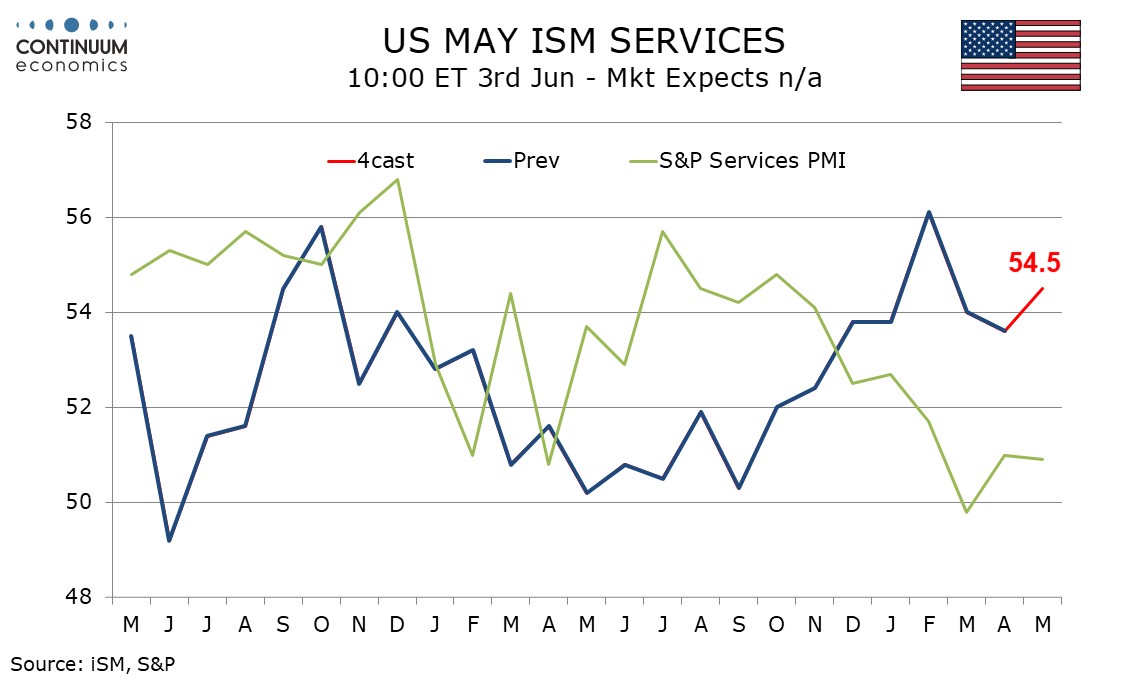

And Seasonal adjustments may provide a lift For ISM Service

DXY Choppy in range

We expect a 100k increase in May’s ADP estimate for private sector employment, which would be similar to April’s 109k, which was the strongest since January 2025. It would not be as strong as a 4-week average of 37.75 in the weekly ADP employment report for the weeks to May 9 implies. The weekly ADP data in early April looked similar to the weekly data in early May. Positive signals from the weekly ADP data are consistent with low initial claims, with the initial claims 4-week average lower in May’s payroll survey week than in April’s, though the weekly data has moved off the lows by the time of the survey week, and the signals from continued claims are not as strong.

We expect some slowing ion the non-farm payroll, to 85k from 115k overall and to 90k from 123k in the private sector. We thus expect a modest outperformance of private sector payrolls from May’s ADP report after a modest underperformance in April. The closure of Sprit Airlines caused 17k redundancies that should be caught by non-farm payrolls but may not be by ADP data.

We expect May’s ISM services index to pick up to 54.5 from 53.6 in April, picking up after two straight declines from February’s 56.1. While rising energy prices are a downside risk for services activity, seasonal adjustments may provide some support in May. We expect outcomes of 56.5 for both business activity and new orders, picking up from 55.9 and 53.5 respectively, both benefiting from easier seasonal adjustments. We expect supply shortages coming from the Middle East conflict to bring a further acceleration in delivery times, to 57.5 from 56.8. Only in employment of the four contributors to the composite do we expect slowing, to 47.5 from 48.0.

USD flows continue to dominates as haven bids/offers from geopolitical uncertainty are in the driver's seat. There hasn't been much progress lately but also little signs of talks breaking down also. It is likely both sides will come to the middle ground with Trump facing domestic pressure and Iran met with steep economic difficulty plus full oil storage facility soon.

Choppy trade has given way to a spike to 99.40, before settling lower as overbought intraday studies unwind, into fresh consolidation around 99.10. Daily readings continue to track lower and broader weekly charts are coming under pressure, highlighting room for fresh losses in the coming sessions. A break below congestion support at 99.00 will open up the 98.75 weekly low of 29 May, with a break beneath here opening up congestion around 98.50. However, any immediate continuation should be limited in consolidation above 98.00, as daily stochastics become oversold. Meanwhile, resistance remains at 99.50 and should continue to cap any immediate tests higher.