FX Weekly Strategy: Asia, Jun 29 - Jul 3

EZ HICP seen peaking, US payrolls solid but flattered

Central bank get-together. Rate hike expectations easing in tandem

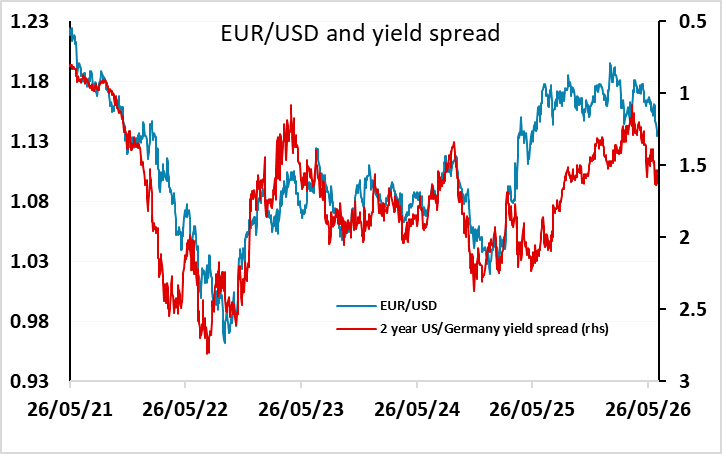

Dollar still firm, but market to finish unwinding overbought conditions

The week ahead has plenty of notable events, spanning Eurozone inflation on one side, to US payrolls on the other, and with central bank speakers all round - the ECB Sintra conference at the start of the week hears from Lagarde and then a panel that includes Warsh and Bailey.

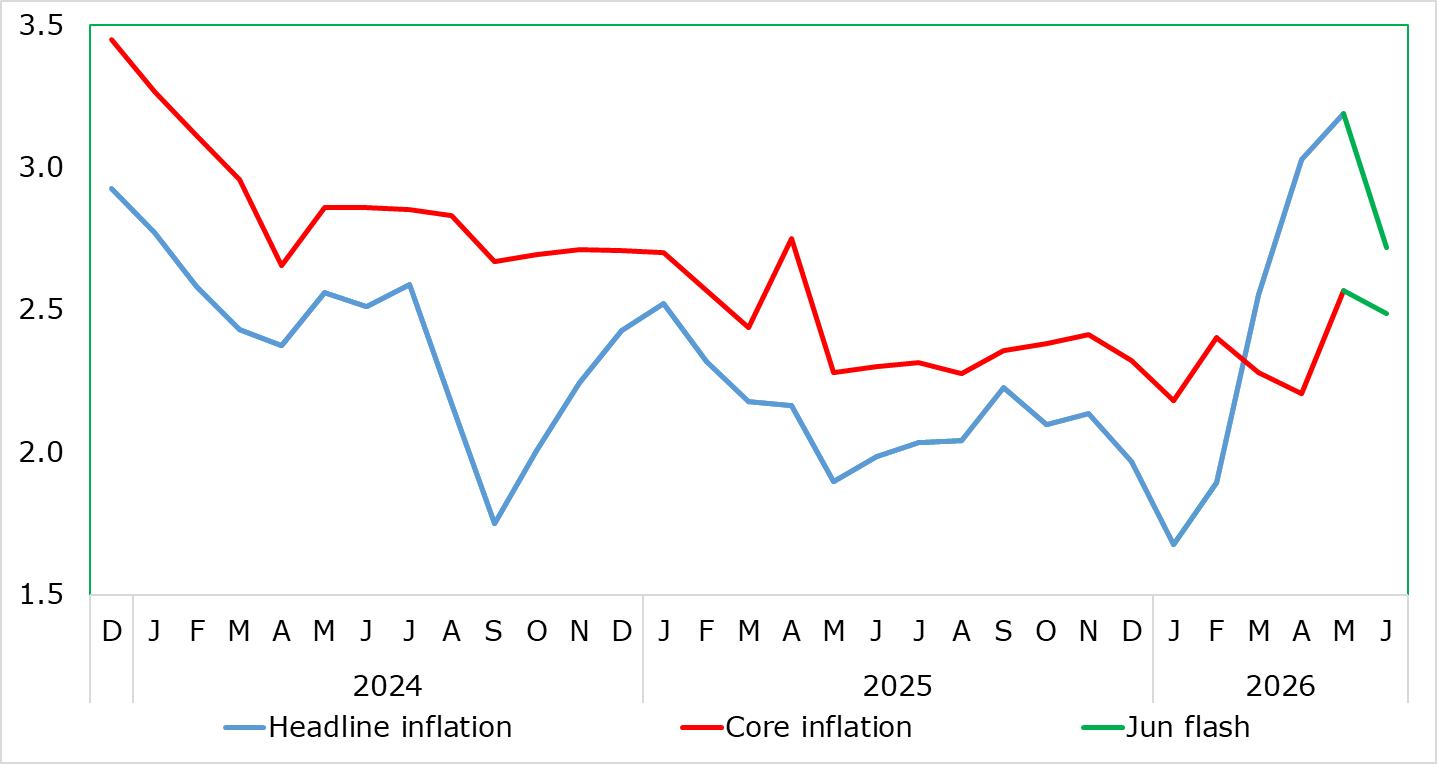

ECB Lagarde has sounded a less hawkish note in recent days, highlighting the lack of second run effects and suggesting no need for ‘forceful action’ as energy prices drop back steeply on the Iran MoU. Market pricing has been leaking but there is still another hike priced in by October and ¾ priced in by Sep, so there may still be some room for erosion if this tone is maintained. We expect to see signs of peaking in this week’s HICP print and that too could help shift the market pricing more hedged even if it is going to be reluctant to entirely give up on the risk of a follow up just yet based on past precedent.

On the Fed side, Warsh makes a point of not giving forward guidance but, deliberate or not, the natural inclination to emphasis price stability and monetary policy responsibility for inflation on first appearance did inflame a marked initial market response. So he does have the opportunity to double down on that early ‘credibility marker’ or row back if he chooses. The discussion on AI might give more indications of his more medium-term stance though given past focus from him on the supply-side and productivity side of the equation.

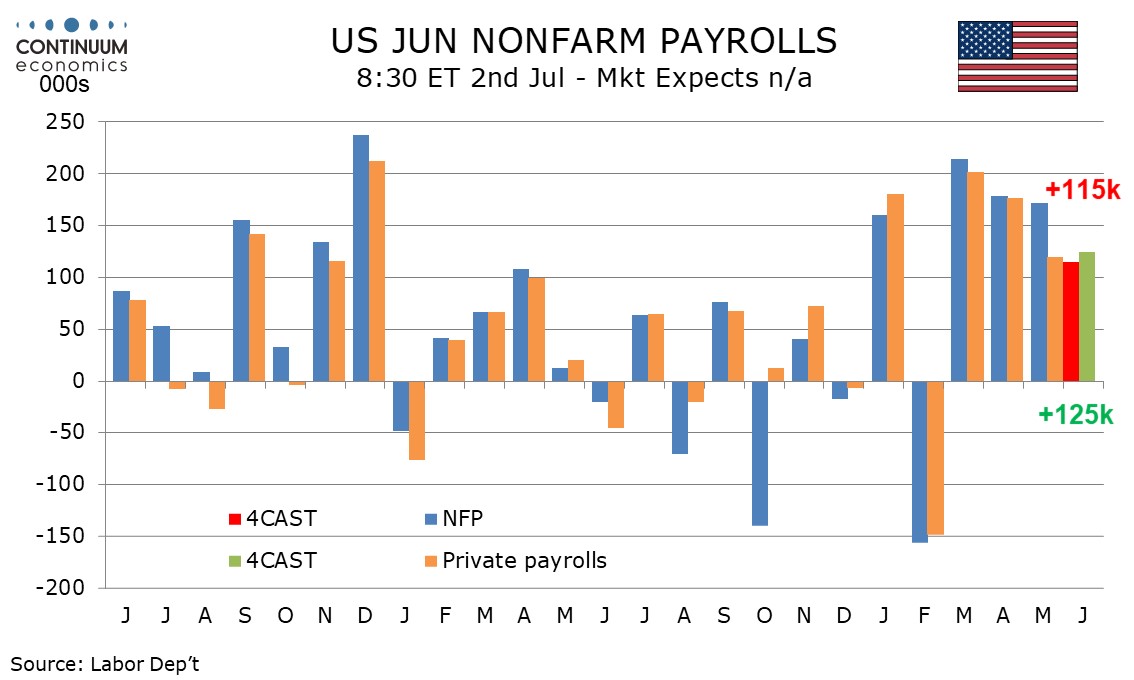

Our call for payrolls is a little ‘middling’ – fairly solid all round, though again likely somewhat flattered by hospitality into the World Cup. A bit like PCE prices last week, the market’s take given recent re-orientation might be that its ‘not strong enough’ to be hawkish / dollar bullish, while at the same time it is expected to be robust enough to actually be pretty agnostic for the current debate.

Any dregs from the hangover from last week will also likely colour the early action as well as the market completes the work off from its overbought dollar action built up over the speedy post FOMC breakout. This does allow then for EUR/USD run on through the 1.1410 break, but supply is expected to build into .50+ and short-term MA trend above, so that selling into rallies is expected to keep the dollar underpinned. Over coming weeks there still seems more scope for some dollar follow through higher before the overall swing higher complete.

It’s worth noting that while US yields have come well off from the post FOMC spike, along with oil and more mixed risk, so have Eurozone. There’s scope for both to continue to do so in parallel, so long as Iran remains benign. Net, that still leaves interest rate spreads down at absolute levels where it allows for the EUR/USD breakdown to run on modestly firmer, once a technical breather has run its course.

In terms of the wider dollar performance, it also worth noting the month and quarter end. Here it is especially notable the extent to which, in theory at least, relative equity performance over the quarter ought to play to strong USD/JPY rebalancing support, though it doesn't always play out like that of course. If it does, the market will naturally remain focused on intervention risks. In fact, the market might end up being 'self policing' here anyway if upside attracts natural profit-taking selling interest from the wider market. There is just a vague sense that the market is viewing the pair as running out of gas and maybe longer-term longs may be more inclined to be reducing positions and booking large profits.

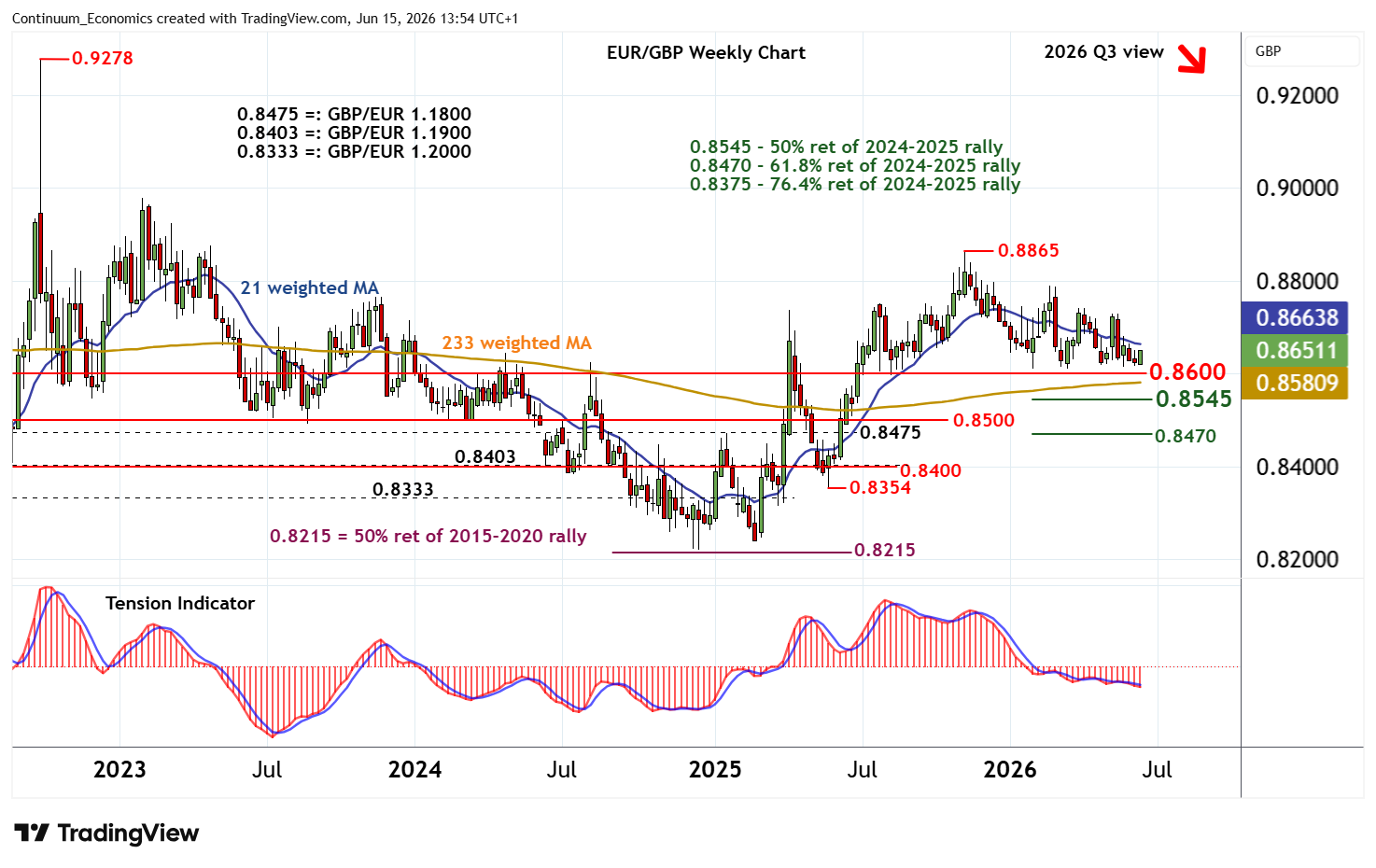

In the UK, politics may have flagged as a market driver, but Burnham’s speech expected this week will still be watched for the signals it gives. Many a UK PM/Chancellor from Brown onwards have been lured by the apparent win-win of an investment growth agenda and Burnham seems equally inclined. How the market buys into that, or not, will be telling. His pick as chancellor is a more obvious market focal point too. EUR/GBP continues to trade out what you might call a treacherous triangle – it has all the apparent qualities of building into an apex that pressures the long time floor and breaks to sterling’s favour (catching the market offside). But everyone has seen enough of these be a coin flip – either a false break that sucks in stops and then returns, or just a drift out of triangle into more range and so upside. Near-term, the more likely scenario for EUR/GBP (perhaps temporary) downside break would actually be euro driven - if the EUR/USD sell off extends and continues to drive faster euro action vs the dollar than cable, given positioning.

Elsewhere, we made the case in the Outlook for the NOK to be in thematic trade correction mode for a while even if it has long-term favourable fundamentals - though as elsewhere there is a case for some of the unwind of last week to be getting a bit stretch technically. Even so, there’s more downside scope ahead after any pause/correction, so long as oil prices don’t spike afresh. EUR/NOK has got to the circa 11.3~ point which is a good reference but can look to 11.4/50 after (break and 50%). USD/NOK likewise continues to run to 10 big figure next.

Note that the USMCA deadline falls this week too. While this is hardly news and the market is already expecting this passes without signature, it does present the opportunity for headline risk and so one to watch for CAD. USD/CAD has been similar to elsehwere in that it has seen the dollar acceleration but then overbought pullback from 1.42~ test.

Data and events for the week ahead

USA

The data highlight in the US will be June’s non-farm payroll, due on Thursday due to Friday seeing the Independence Day holiday. We expect a rise of 115k, 125k in the private sector, with temporary hiring for the World Cup likely to weigh against a loss of underlying momentum. We expect unemployment to be unchanged at 4.3% and an in line with trend 0.3% increase in average hourly earnings. Other labor market indicators come from May’s JOLTS report on job openings on Tuesday, Wednesday’s ADP report of private sector employment, for which we also expect a rise of 125k, and weekly jobless claims on Thursday.

Tuesday sees June consumer confidence as well as April house price data from S and P Case-Shiller and FHFA. Wednesday sees May construction spending and June’s ISM manufacturing index, which we expect to be unchanged at 54.0. May factory orders are due on Thursday. Fed’s Warsh will speak on Wednesday and will be closely listened to.

Canada

Canada releases April GDP on Tuesday. We expect a 0.3% increase, slightly below a 0.4% estimate made with March data. June’s S and P manufacturing PMI is due in Thursday.

UK

Coming before final PMI data (Wed & Fri), there are final Q1 GDP numbers where no revision is envisaged (Mon). Published alongside, will be current account data, the gap likely to widen slightly beyond 2.5% of GDP. Otherwise, the BoE dominates the week with Monday’s money/credit data likely to show more signs of a softer housing market, thereby chiming with anecdotal evidence. Such signs may get short shrift from MPC hawk Mann who speaks (Thu) but may mention in updated BoE Credit Condition Survey data (Thu) or via the latest Decision Maker’s Panel (Fri).

Eurozone

Data wise, there are final manufacturing and services PMI numbers (Wed/Fri). Otherwise, the week is dominated by Monday’s actual money and credit figures, where some credit weakness is emerging, these coming almost alongside Thursday’s labor market data which still suggest abundant workforce supply. Monday also sees key survey data for the European Commission, likely to chime with PMIs in signalling on-going economic fragility.

But the main event will be the June HICP flash (Wed), partly flagged by German HICP numbers (Tue). These data may have a material impact on ECB thinking, especially as they arrive toward the end of the ECB monetary annual gathering in Sintra (Mon-Wed). Indeed, the numbers may suggest the headline rate peaked at 3.2% in May and not the 3.4% rate implicit for June in the ECB quarterly projections released earlier this month. In fact, we see the headline down to as low as 2.7% pulled down not just by hefty energy price falls but also a seasonal aberration in travel prices that pushed up services inflation in May. This could involve small dip in the core too. House price data arrive on Thursday.

Rest of Western Europe

There are few key events in Sweden. In Switzerland, Tuesday sees the latest KOF survey update and Thursday sees what may be near-unchanged headline June CPI numbers, such an outcome chiming with the SNB latest projection. The SNB also releases its latest Financial Stability Report. Norway on Friday releases the latest credit numbers, alongside updated Unemployment figures.

JP

Kickstarting the week with Retail sales. It would be great to see a positive outcome as consumption has been lagging behind real wage gains. Followed by labor data on Tuesday and other tier two data throughout the week. Both shouldn’t be JPY moving.

AU

RBA Governor Bullock will be speaking on late Sunday yet unlikely to provide new cues for rate move, given the current inflation dynamics. So as the meeting minutes on Tuesday. Trade balance on Thursday will likely be more important for changes in energy import.

NZ

Only consumer confidence on Friday may catch an eye.