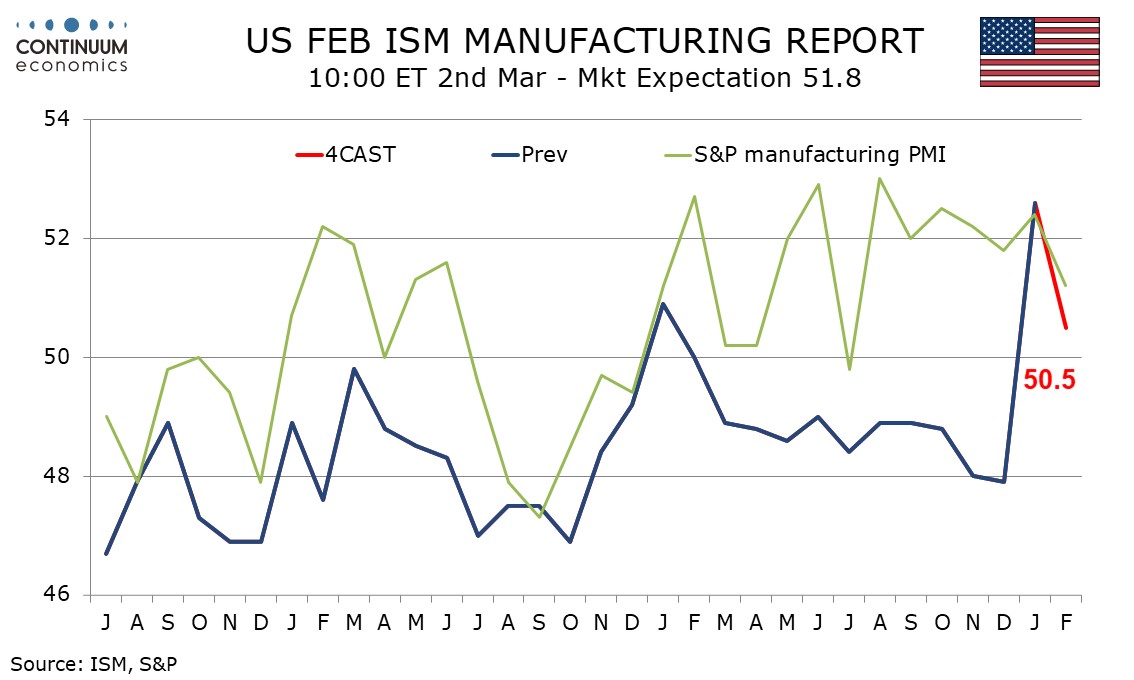

Preview: Due March 2 - U.S. February ISM Manufacturing - Correcting lower but still positive

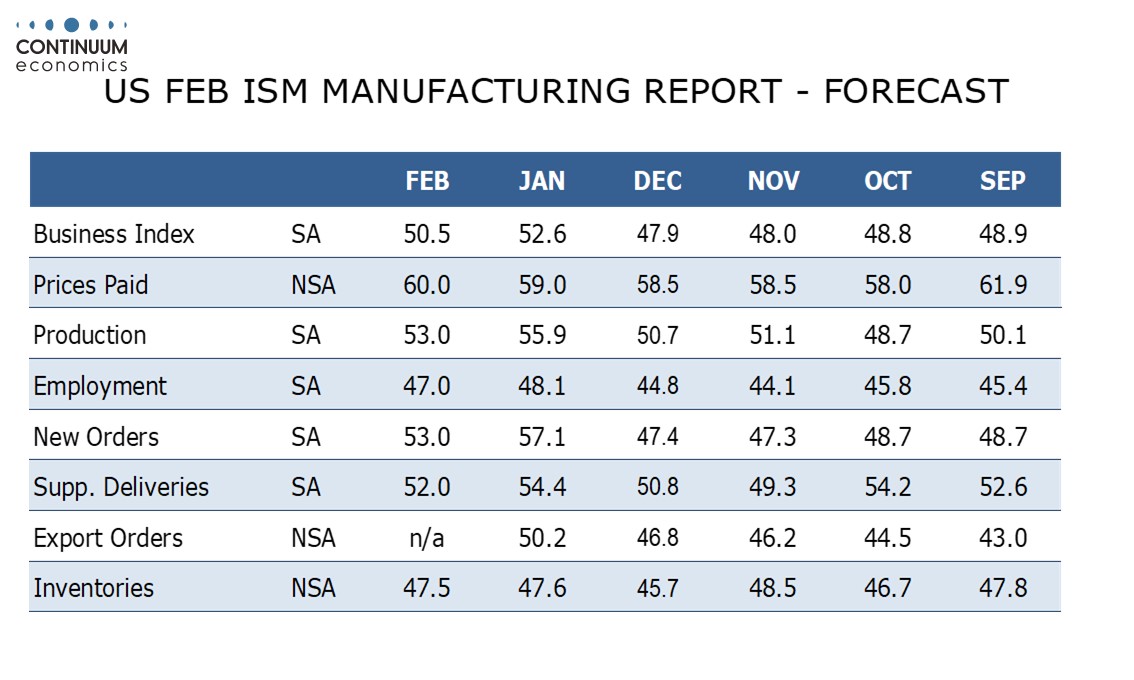

We expect February’s ISM manufacturing index to correct lower to 50.5 from January’s sharply improved 52.6, though this would still deliver a second straight positive reading to follow ten straight negatives.

Durable goods orders trend has been picking up and January manufacturing output was improved, backing the message of January’s ISM manufacturing index. However, ISM manufacturing seasonal adjustments are less supportive in February than January.

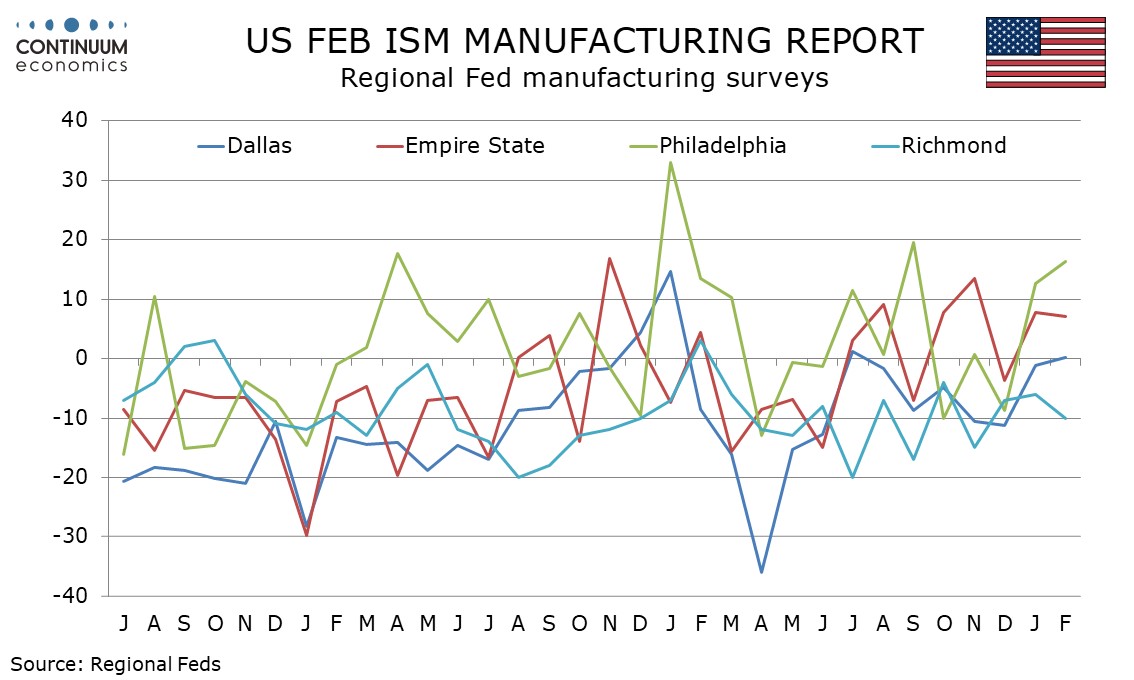

Other February manufacturing surveys have been mixed with the S and P’s survey slipping. The Philly and Dallas Fed surveys were improved, the former quite impressively, but the Empire State and Richmond Fed surveys slipped, with the latter increasingly negative.

We expect ISM detail to show a significant correction lower in new orders with production, employment and delivery times all also slipping from improved January readings. We expect little change in inventories, completing the breakdown of the composite.

Prices paid do not contribute to the composite and here we see an increase to 60.0 from 59.0, led by energy prices.