EUR/USD flows: Fed challenges suggest dollar outlook to remain complicated

Fed Warsh to be sworn in to a testing environment

Grand concept to run into current realities

While the focus is naturally on Japan’s policy trilemma as it juggles FX, policy rate and long end rates, it’s far from the only central bank to have strategic challenges.

Fed’s Warsh will be sworn in this week to an environment very different to the one where he set out his big concept – a big concept that the broader Fed was already showing little inclination of following, given its policy direction seen since the end of last year amid the realities of market instability.

The big concept, when viewed in combination with the mooted Treasury ideas, revolved around a major pivot involving balance sheet reduction in combination with lower short end rates, a lower dollar, financial deregulation (creating demand for collateral and a growth tailwind) and continuing to move issuance short (with a side helping of crypto policy to bolster Stablecoin demand).

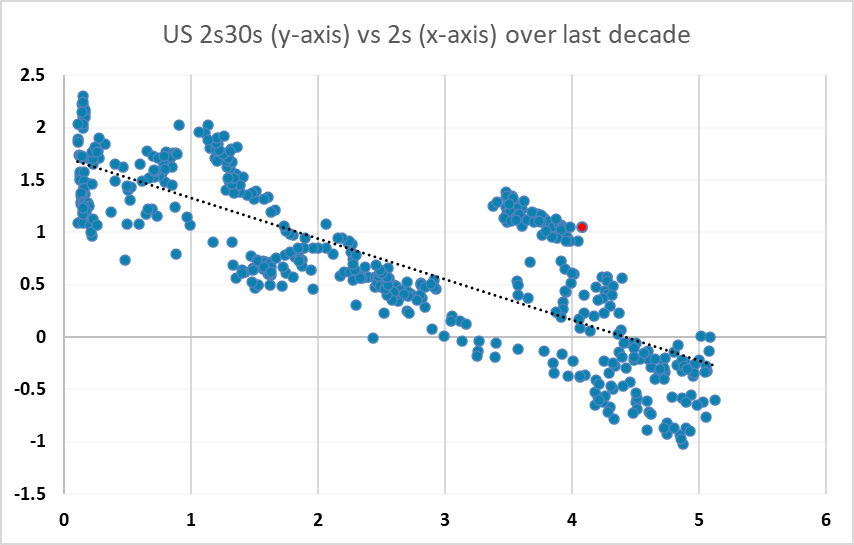

The reality is rather more challenging. Rising risk, term, policy, and demand uncertainty premia have seen the curve shift notably steeper than recent years, in relative terms. While the curve has flattened somewhat since the short end has reacted to the Iran impact, it hasn’t done so to the extent normally seen - by last decades standard, the curve would be much closer to flat already.

If you were super bullish you would see that as reflecting resilient growth, higher productivity and sustained capital build backing a (favourable) rise in real rates. If you are at all less bullish, you see that as reflecting increased bond premia, and policy risk reflecting reduced confidence in the Fed put and balance sheet cushion, and global shifts that are reducing structural long end demand.

The upshot is an environment where a great policy experiment is not only hard to force through the Fed board but one where economic and bond market realities are too challenging, not least unless the current Iran supply crisis rapidly resolves. Bonds are already unstable and would lose their anchor on any suggestion of balance sheet shift from quantitative management back to tightening while easing would risk amplifying the relative loss of long-end control.

The implications of course are highly complex and nuanced and sit within the broader geopolitical story. But, for all the damage to USD status in recent times, it does present a counterpoint to an uncomplicated medium-term dollar negative scenario if the US indeed is caught between unstable equilibriums of tighter policy than assumed or desired, and rapid breakdowns in money market and market stability.