Preview: Due May 28 - U.S. April New Home Sales - Trend has little direction

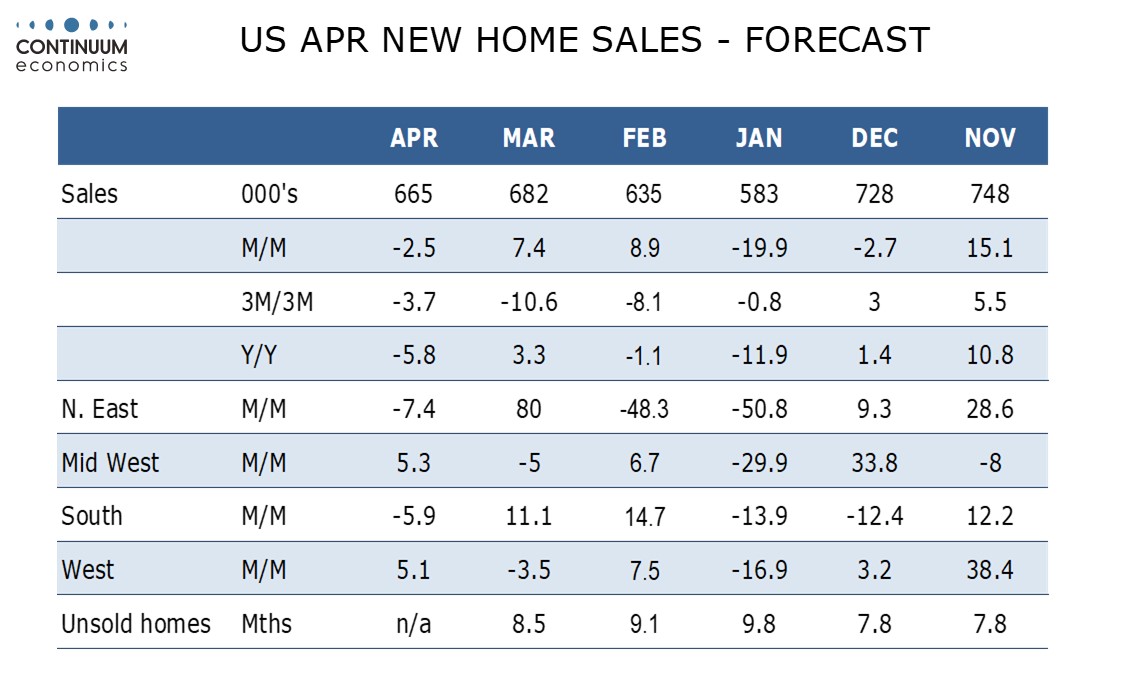

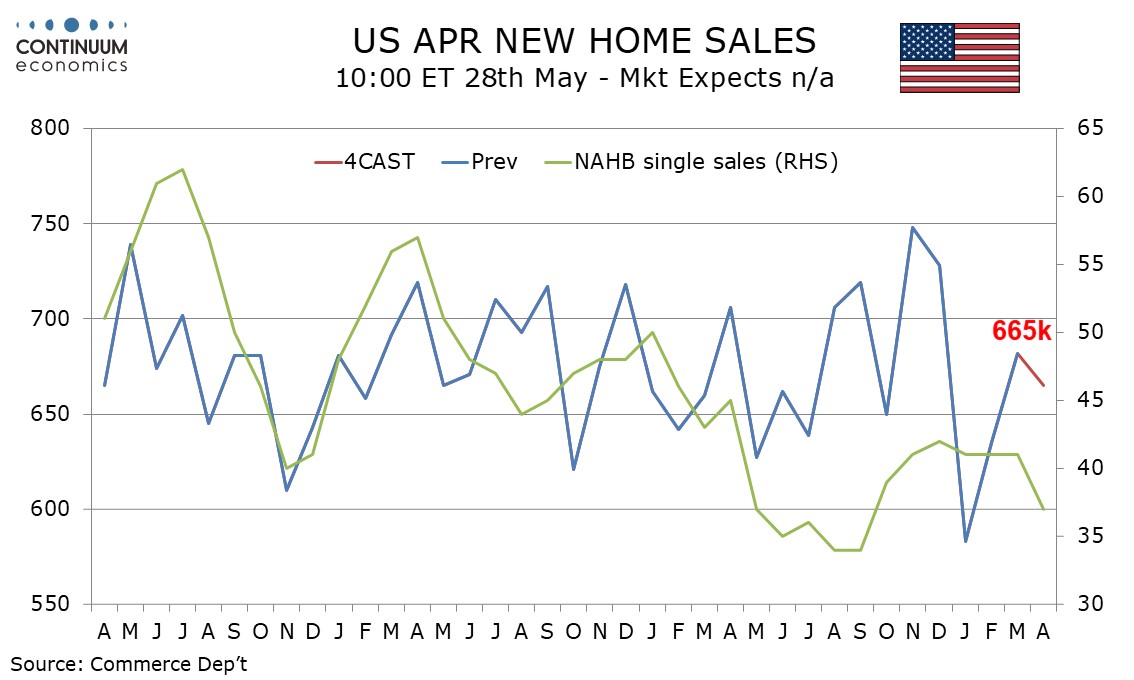

We expect an April new home sales total of 665k, which would be a decline of 2.5% in March’s 7.4% increase to 682k sees no revisions. Over the last three years, movements outside a 650-700k range have trended to be brief though November 2025 hit a high of 748k and January 2026 a low of 583k.

Housing sector indicators generally have little clear trend. April pending home sales saw a third straight increase from a record low in January hinting at upside new home sales risk but the NAHB homebuilders’ index was weaker in April before a bounce in May. The MBA’s house purchase index was fairly stable in April while existing home sales saw a modest rise that failed to fully erase a March decline. Generally the picture is fairly stable, which means resilience to rising mortgage rates as Fed easing expectations fade.

We expect sales to rise in the Midwest and West but to slip in the Northeast and South, all reversing direction from March. The South is the largest region. We expect prices to correct higher on the month, the median by 2.0% and the average by 1.0% after respective declines of 5.3% and 3.4% in March. This would see median prices less negative on a yr/yr basis at -4.5% from -6.2% and the yr/yr average price stable at -1.2%.