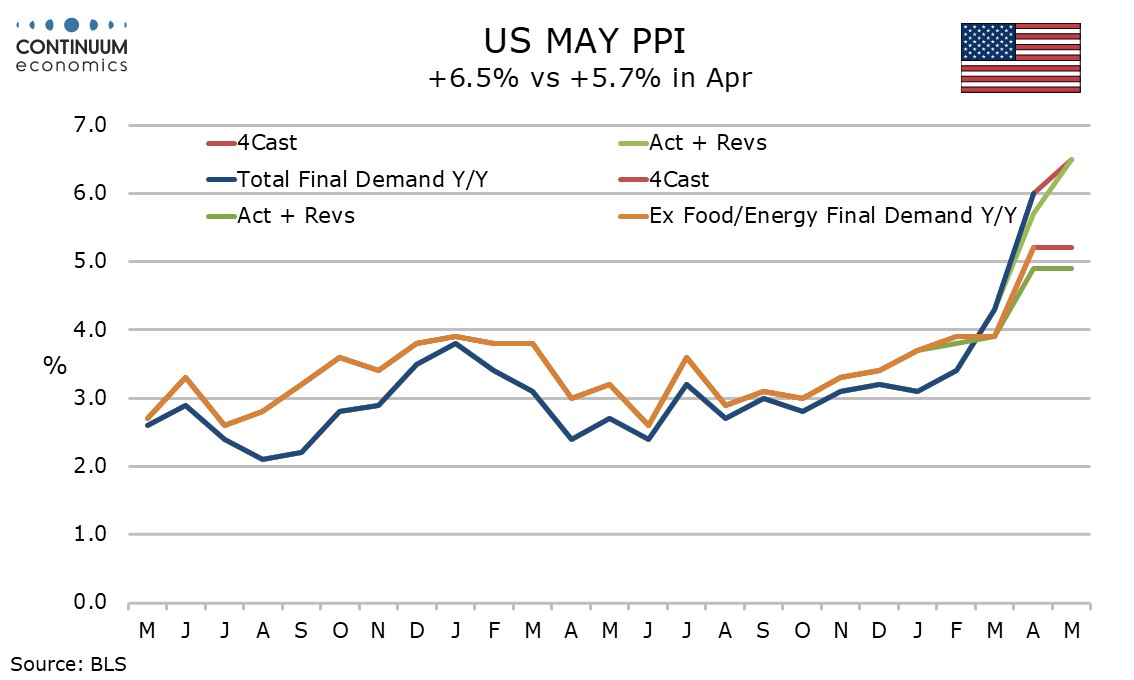

U.S. May PPI - Mostly strong, Initial Claims hinting at slower payroll growth in June

While May’s PPI is mixed, it is on balance a stronger than expected figure with strength overall and ex food, energy and trade outweighing a slightly softer than expected ex food and energy outcome, on a correction lower in trade. Initial claims are hinting June’s payroll will be less strong than May’s.

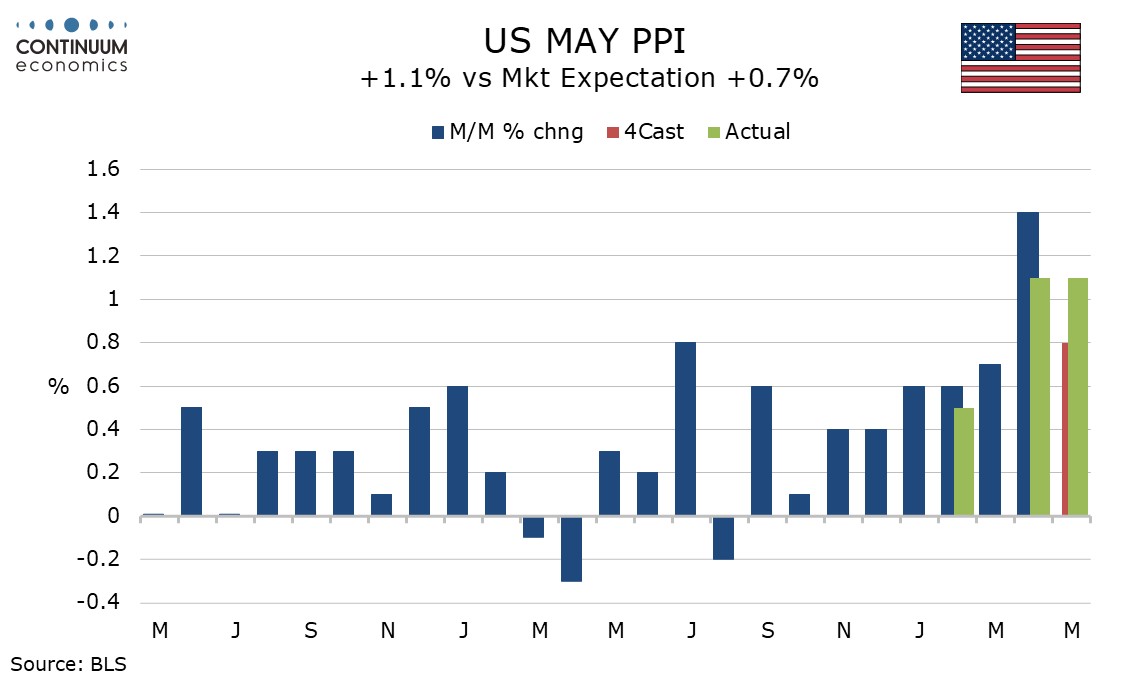

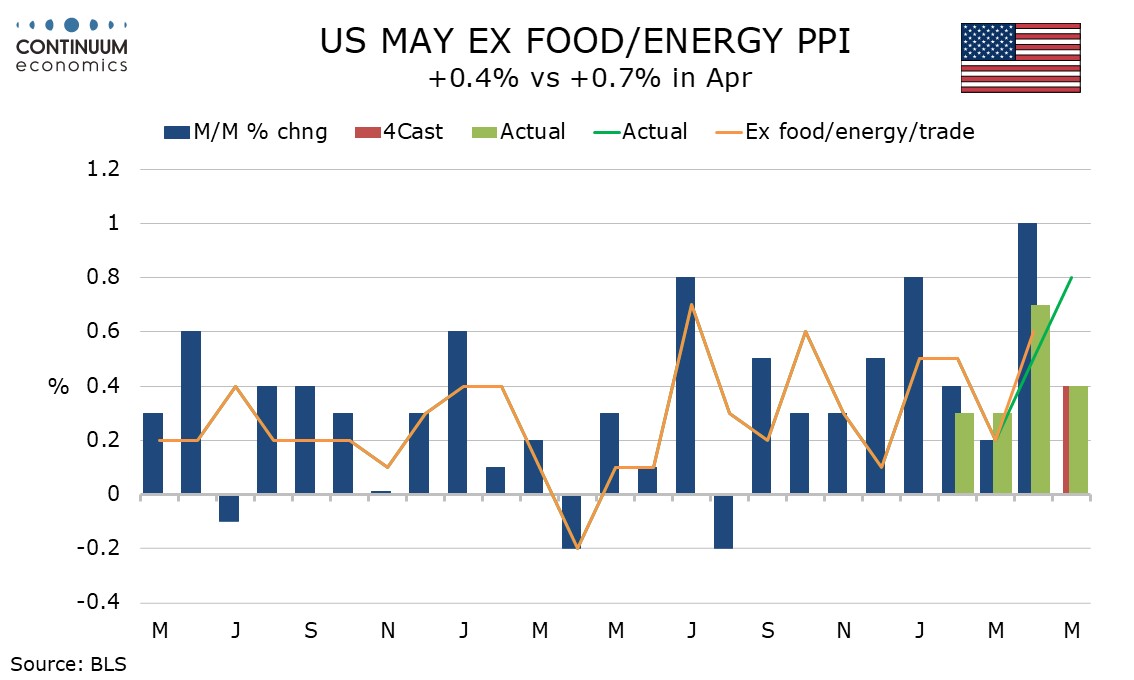

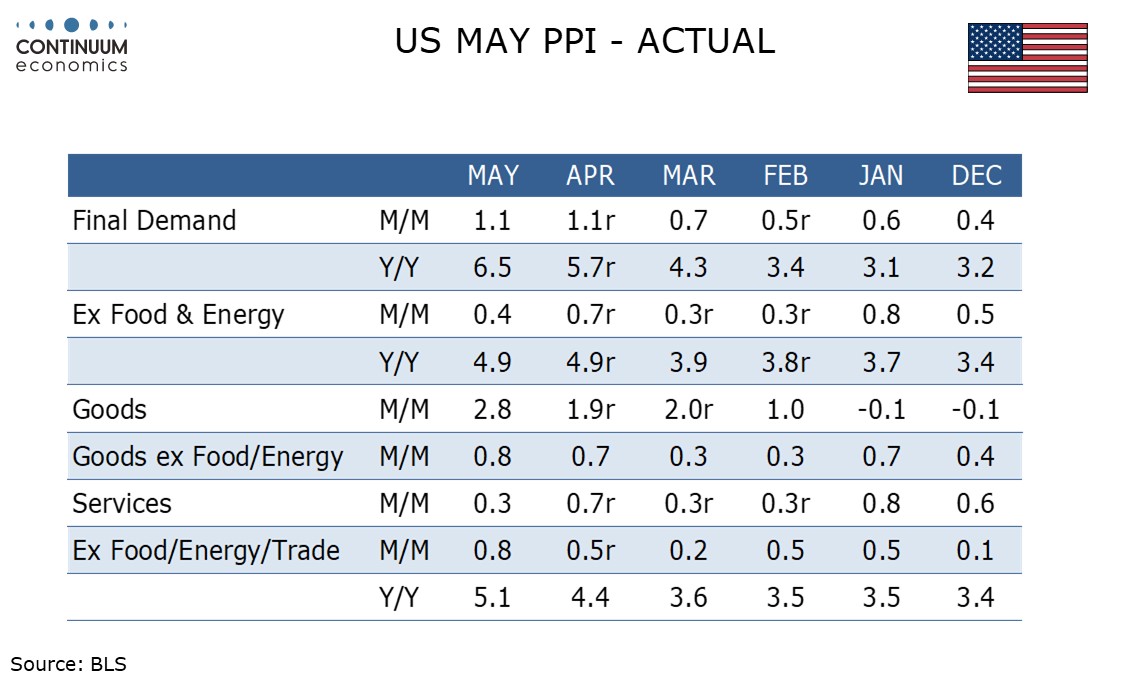

May’s PPI rose by 1.1% for a second straight month, the upside surprise partly offset by a downward revision to April from 1.1%. Ex food and energy was slightly softer than expected at 0.4% with April revised down to 0.7% from 1.0%, but a 0.8% rise ex food, energy and trade, with April revised marginally to 0.5% from 0.6%, implies underlying strength.

Energy surged by 10.7%, surprisingly stronger than 10.4% in March as well as April’s 7.5%. Gasoline led the way with a rise of 23.4%. Food saw a strong but not exceptional month at 0.6%.

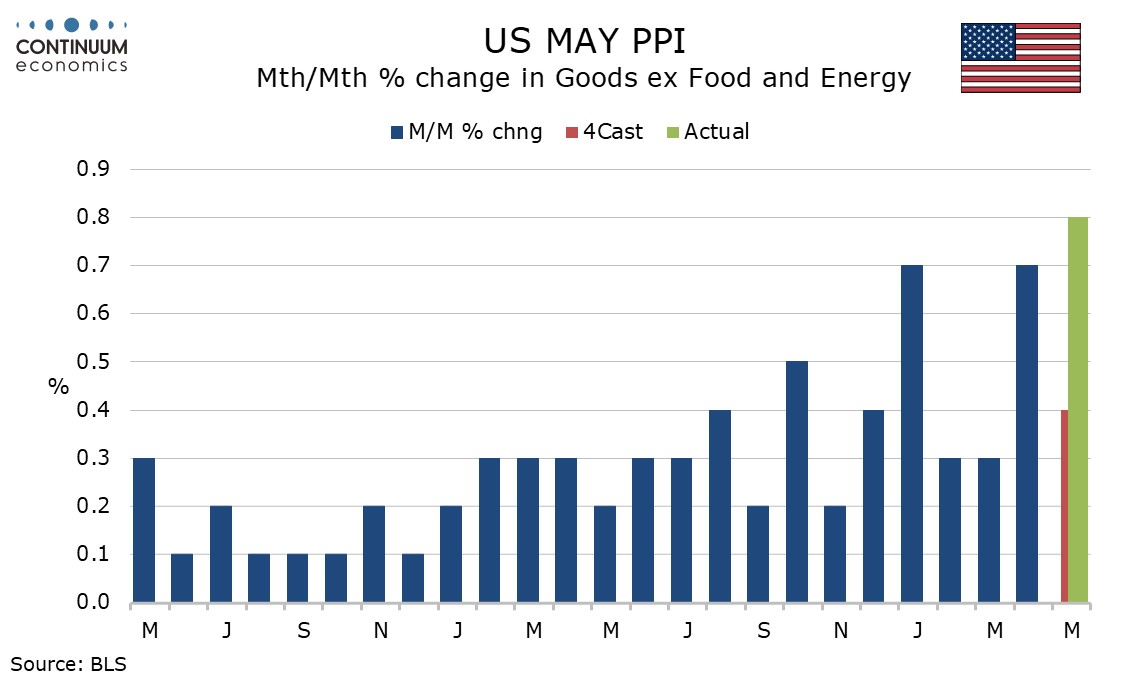

Goods ex food and energy increased by 0.8% after a 0.7% April rise and have shown a marked acceleration in the last two months, disturbing with the tariff impact seen fading, and thus implying some energy pass-on. By far the strongest stand-out was industrial chemicals, surging by 7.6% after a 5.1% increase in April.

Services rose by 0.3% after a 0.7% April rise, restrained by a 1.1% fall in trade after a 1.3% April increase. Transport and warehousing at 2.6% saw a third straight strong gain if less sharp than April’s 3.8% which looks like feed through of energy costs. More disturbing was a 0.7% rise in other services, up from 0.1% in April. Portfolio management at 4.8% and other credit intermediation at 5.4% were stand-outs.

Yr/yr ex food and energy PPI was unchanged at 4.9% but overall PPI accelerated to 6.6% from 5.7% reaching its highest since December 2022 while ex food, energy and trade at 5.1% from 4.4% is the highest since October 2022, showing that the inflation problem goes well beyond energy.

Intermediate data was generally firm too, processed goods up 3.5% and 1.8% ex food and energy, unprocessed goods up 4.9% and 2.6% ex food and energy, and services up by 0.5%.

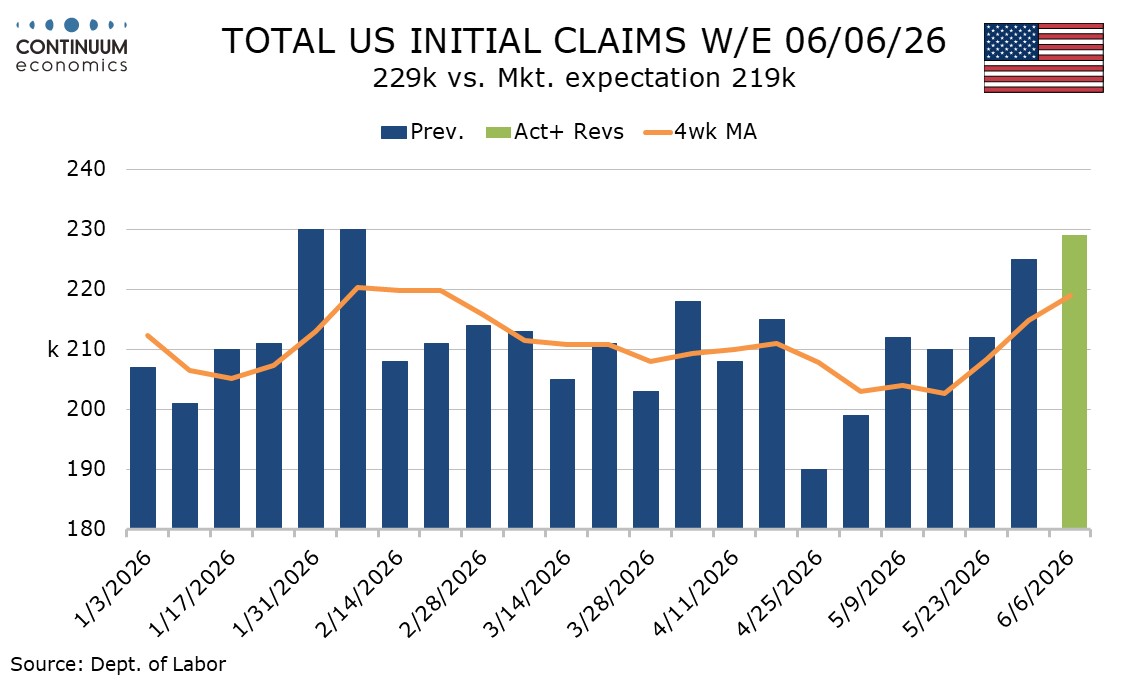

Weekly initial claims at 229k from 225k are the highest since December 6 and suggest that an acceleration last week cannot be blamed solely on the Memorial Day holiday that took place in the week. The survey week for June’s non-farm payroll comes next week. The labor market may be losing some of the healthy momentum seen from February through May.

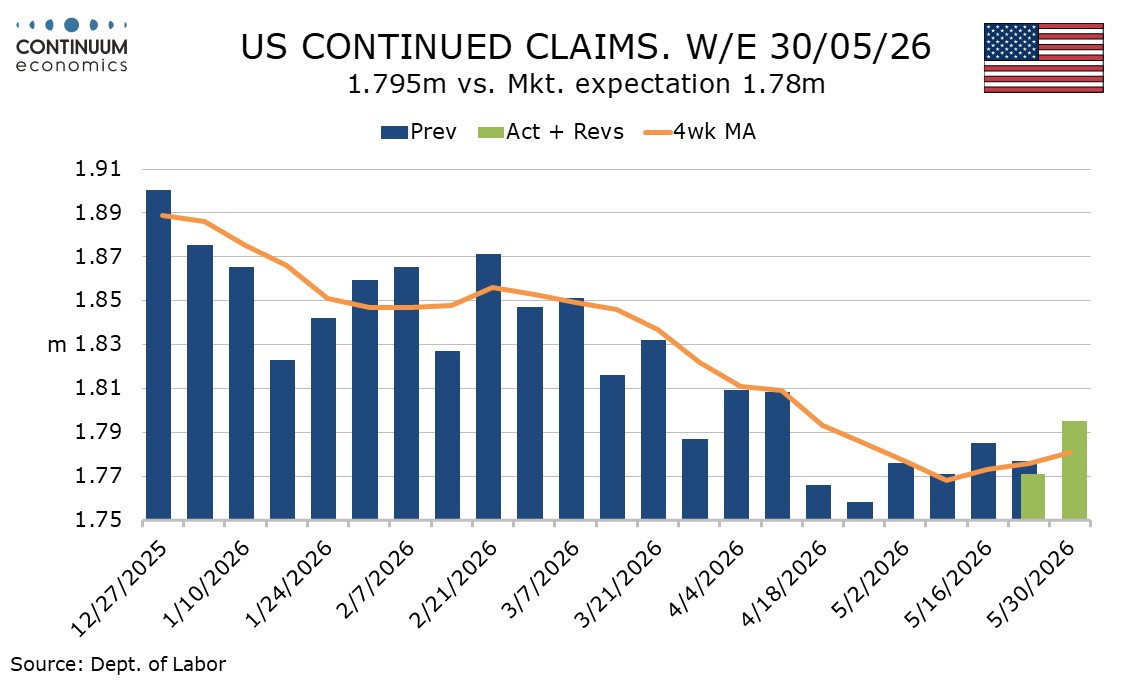

Continued claims cover the week before initial claims. Here a 24k increase was seen to 1.795m, the highest since a relatively recent April 11, so not a worrying sign. However a declining trend from February through early May appears to have found a base, and that implies some loss of payroll momentum.