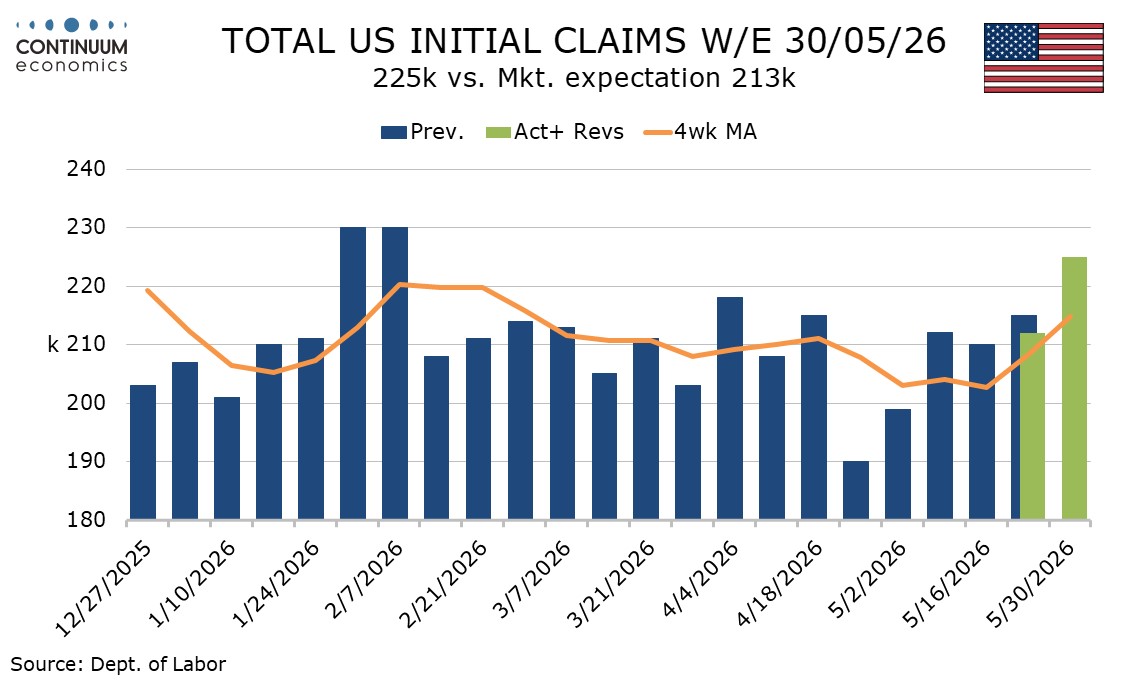

U.S. Initial Claims up in holiday week, Q1 Productivity and Unit Labor Costs both revised down

Initial claims at 225k in the week to May 30 are up from 212k and the highest since February 7, though the data should be treated with some caution given that the week included the Memorial Day holiday, which can cause seasonal adjustment difficulties.

The survey week for May’s non-farm payroll came two weeks ago, and the 4-week average of 202.75k was well below the 211k seen in April’s survey week, though by the survey week the weekly data had returned to trend after two weeks when outcomes below 200k were seen.

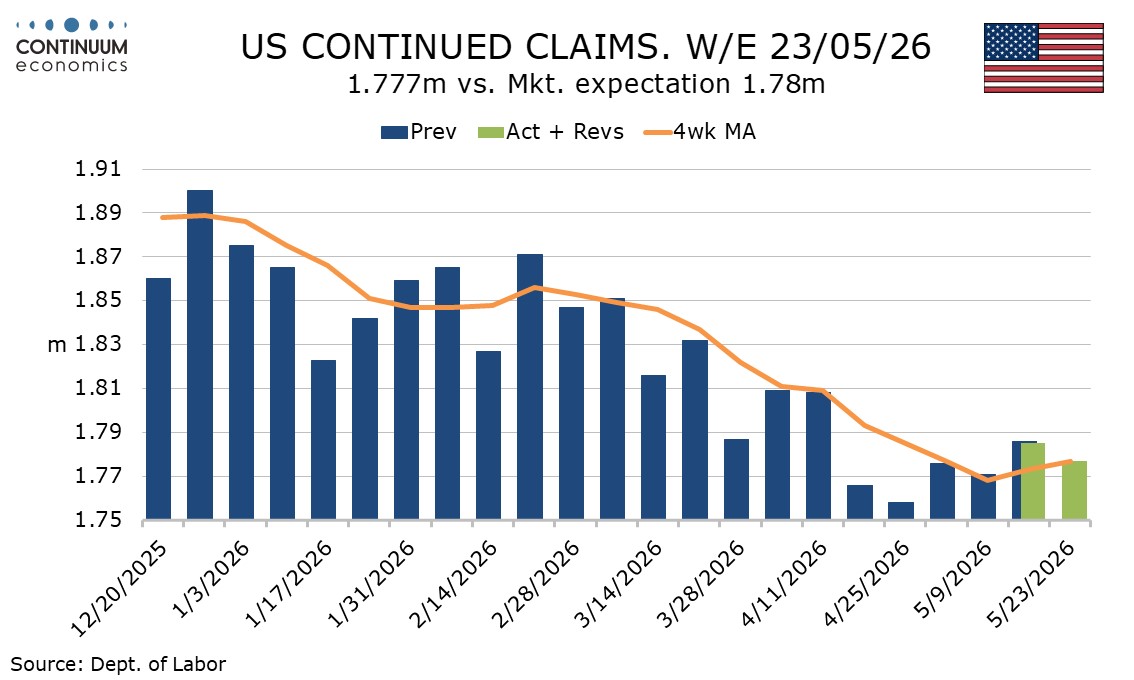

Continued claims cover the week before initial claims and saw a fall of 8k to 1.777m, which is on the 4-week average. Trend here is showing some hints of stabilization after moving lower from February through April.

The signals from initial claims are generally supportive of a healthy May payroll, but there are tentative hints that momentum is starting to slow as we enter June.

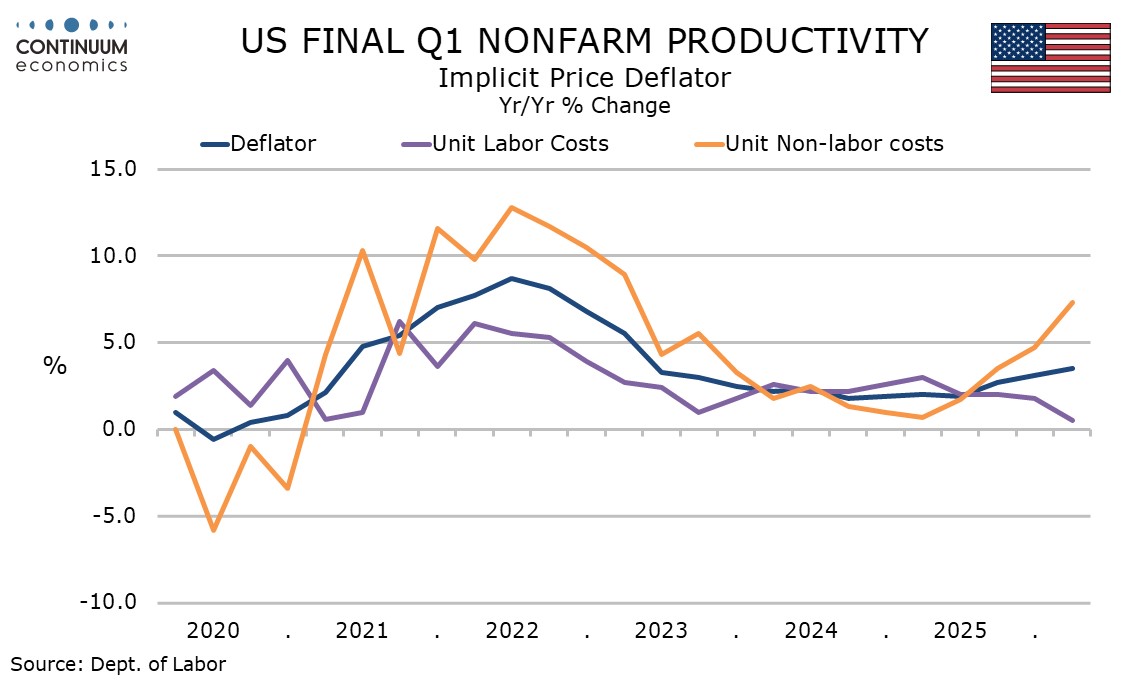

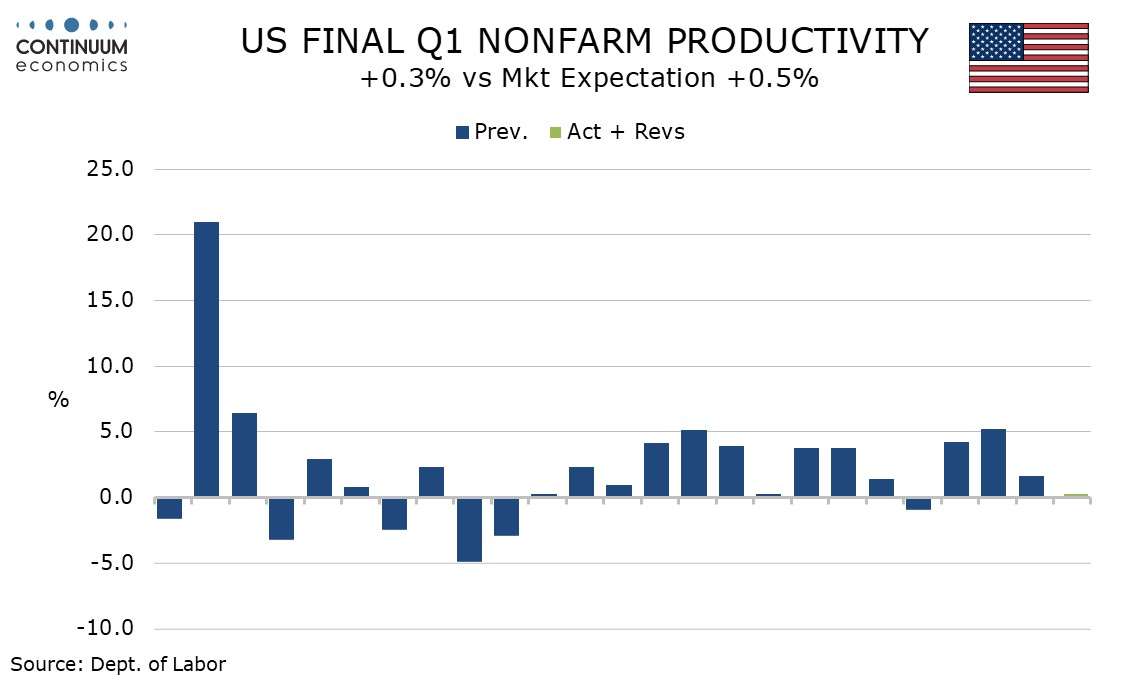

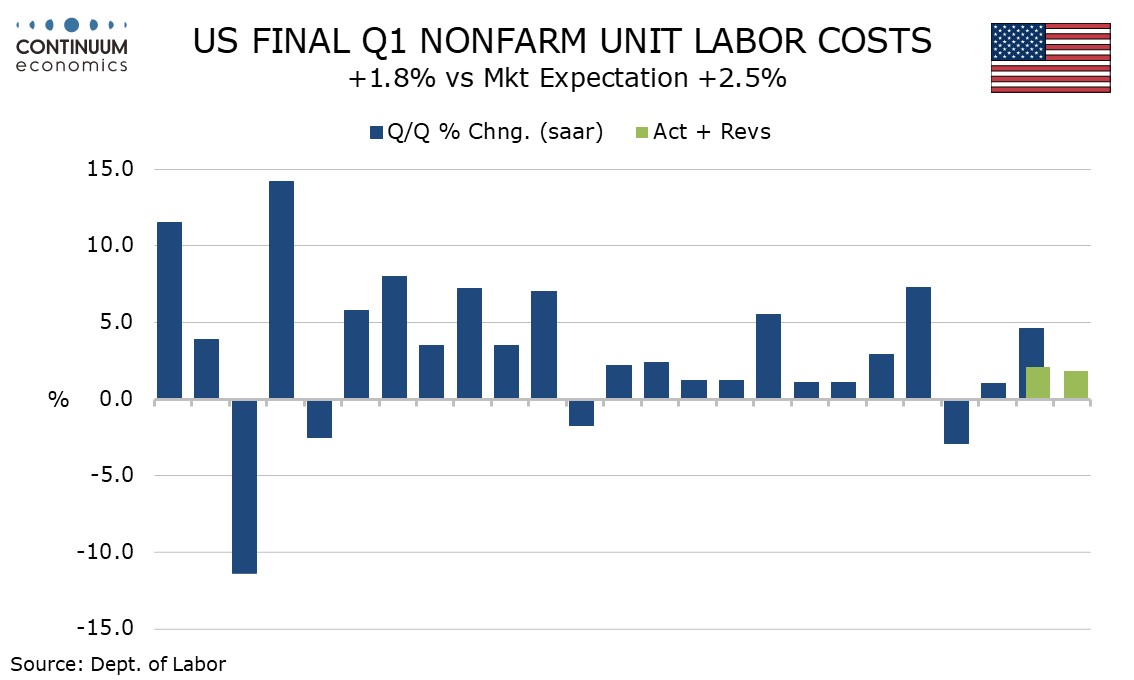

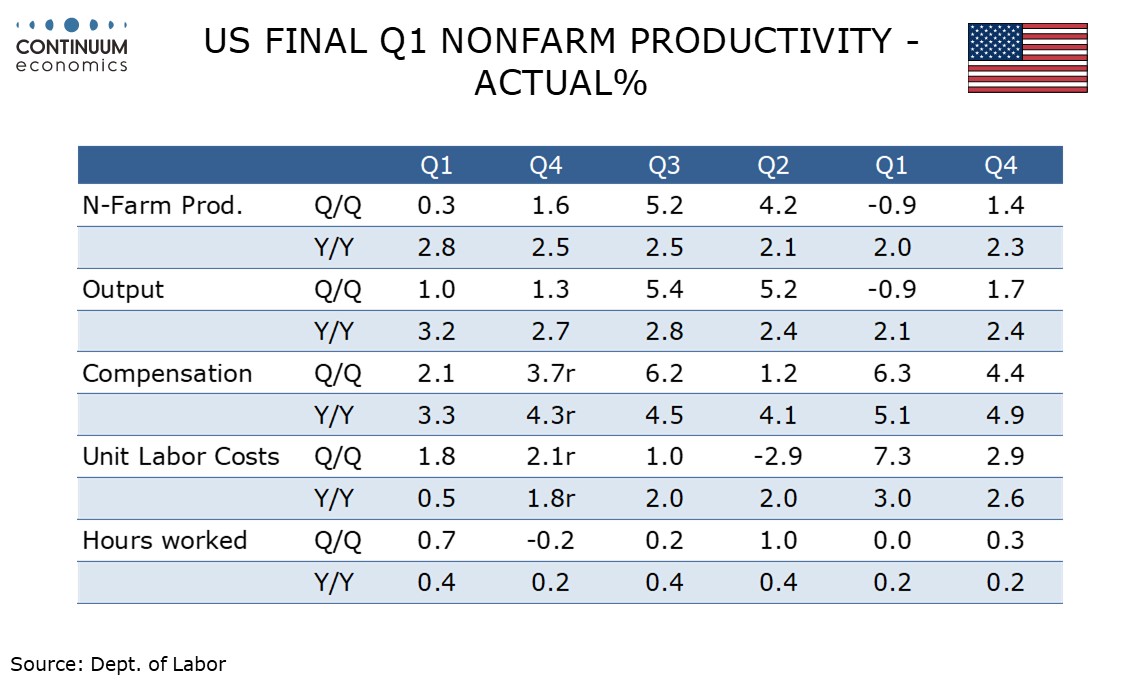

Q1 productivity was revised down to 0.3% from 0.8% with non-farm business output revised down to 1.0% from 1.5% in line with the details of a negative revision to GDP while aggregate hours were unrevised at 0.7%. Despite the subdued Q1, yr/yr productivity is healthy at 2.8%.

Normally a downward revision to productivity means an upward revision to unit labor costs but this time unit labor costs were revised down to 1.8% from 2.3% with compensation revised down to 2.1% from 3.1%. Personal income did see a negative revision in the GDP detail, both for Q4 and Q1.

Non-labor costs were revised up to 8.9% from 8.0% so the revision to the implicit deflator was marginal, to 5.0% from 4.9%. This deflator is up 3.5% yr/yr, the highest since Q1 2023, despite unit labor costs being up only 0.5% yr/yr, a sign of an economy facing inflationary pressure that is not wage-generated.