U.S. May ISM Manufacturing - Supported by AI, inflationary pressures pause

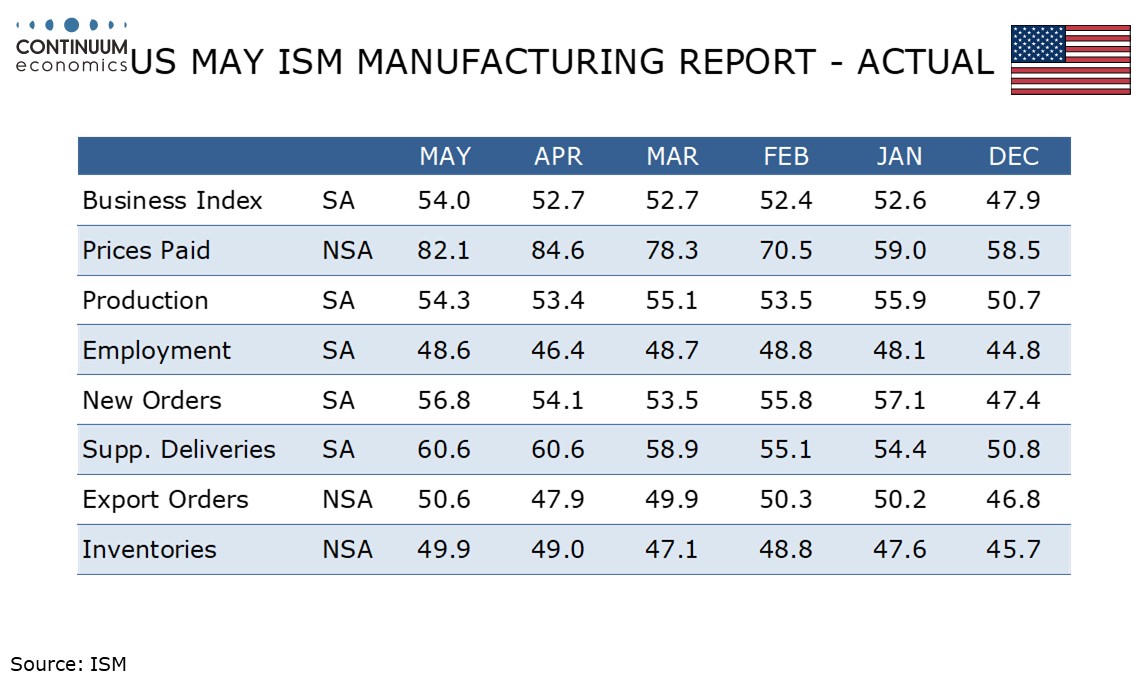

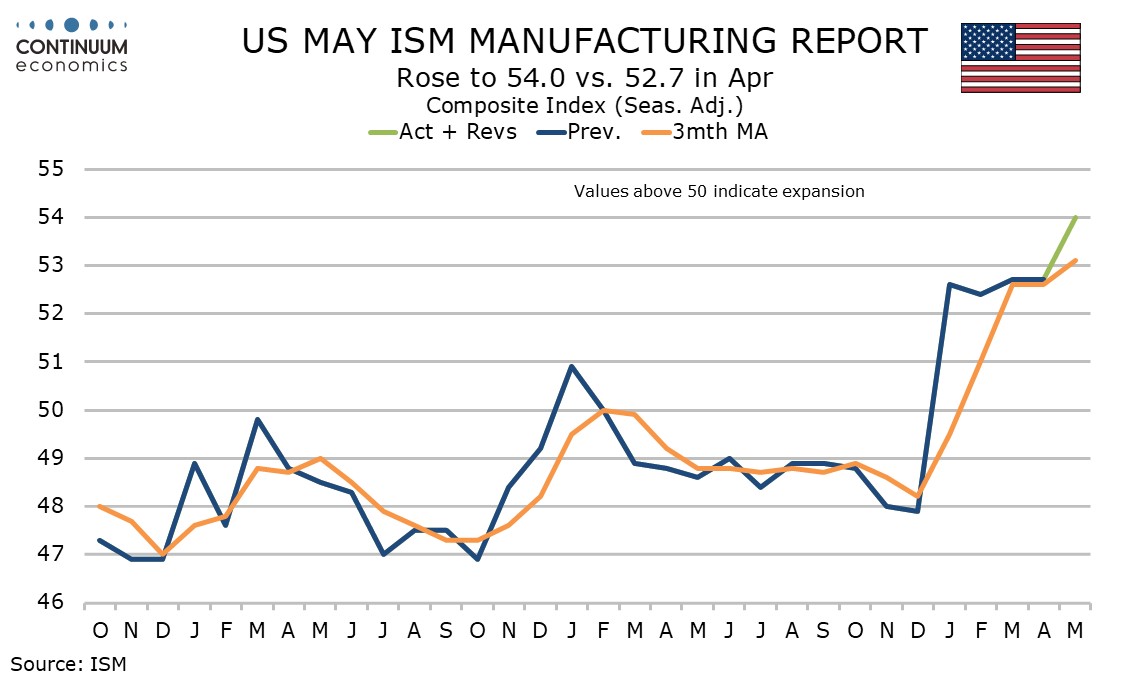

May’s ISM manufacturing index at 54.0 is stronger than expected, up from 52.7 in April and the highest since May 2022. This is consistent with several other manufacturing surveys, notably the S and P national survey, and suggests the manufacturing sector is gaining momentum, most likely fueled by AI.

New orders at 56.8 from 54.1 were particularly impressive, though production was also increasingly positive at 54.3 from 53.4.

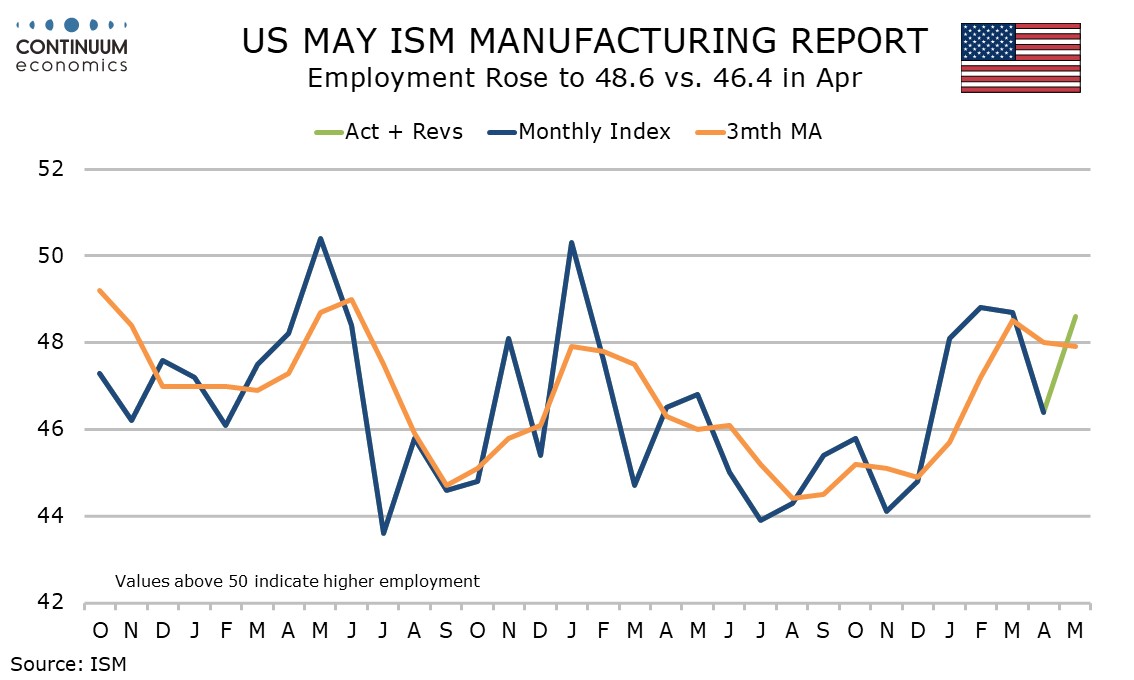

Inventories at 49.9 from 49.0 and employment at 48.6 from 46.4 were significantly less negative but employment did not quite reverse an April dip from March’s 48.7.

The one component of the composite not to increase was unchanged deliveries times at 60.6, though this sustains a significant recent acceleration from near neutral levels in late 2025 as the Middle East situation disrupts supply chains.

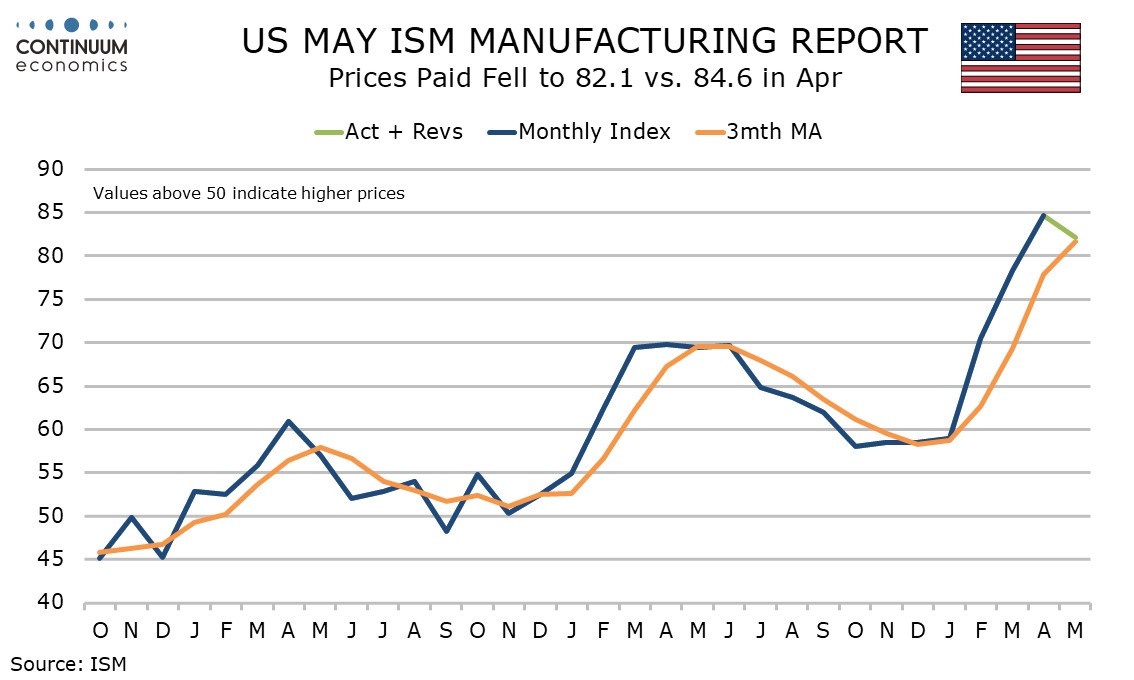

Prices paid do not contribute to the composite and remain very strong at 82.1, though this is a correction from April’s 84.6 which was the highest since April 2022.

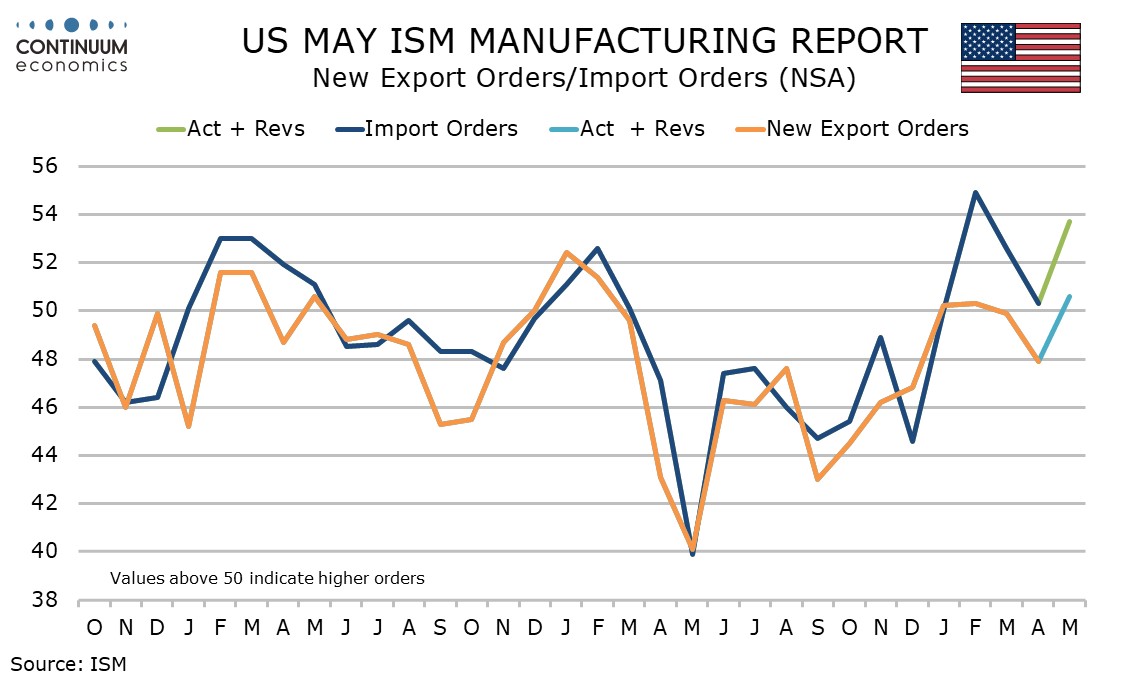

Exports and imports indices also do not contribute to the composite but both are showing resilience to the global situation, exports at 50.6 from 47.9 and imports at 53.7 from 50.3. The exports reading is the highest since February 2025, before the tariffs were implemented.