Preview: Due July 20 - Canada June CPI - Energy to correct lower but BoC core rates seen mostly stable

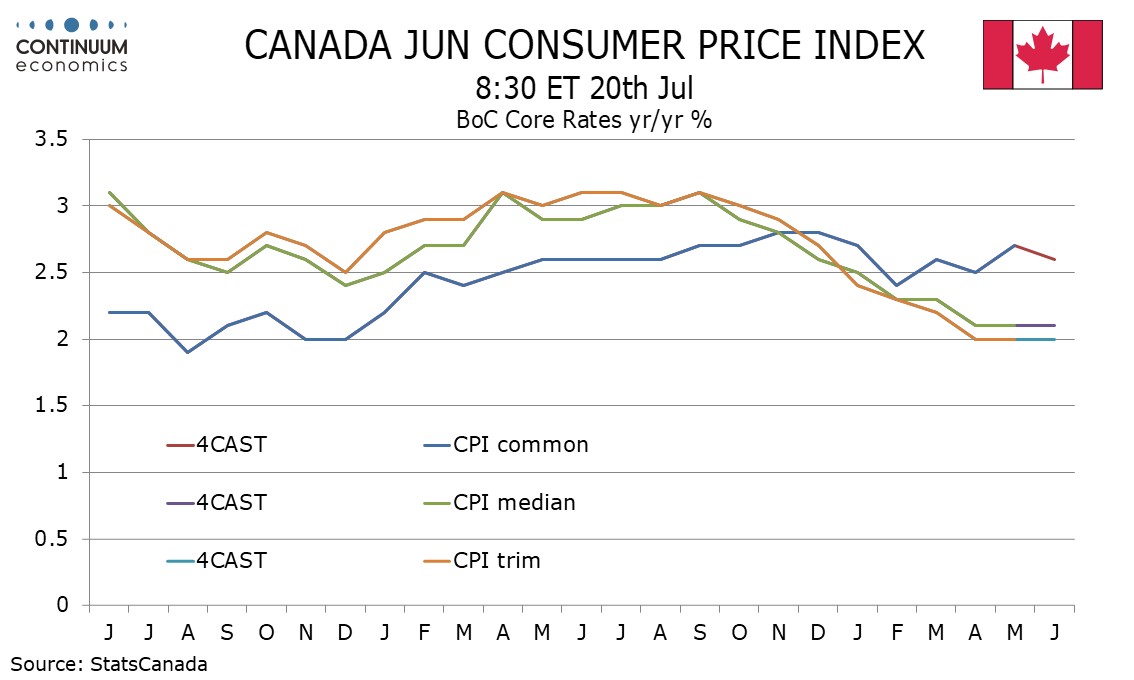

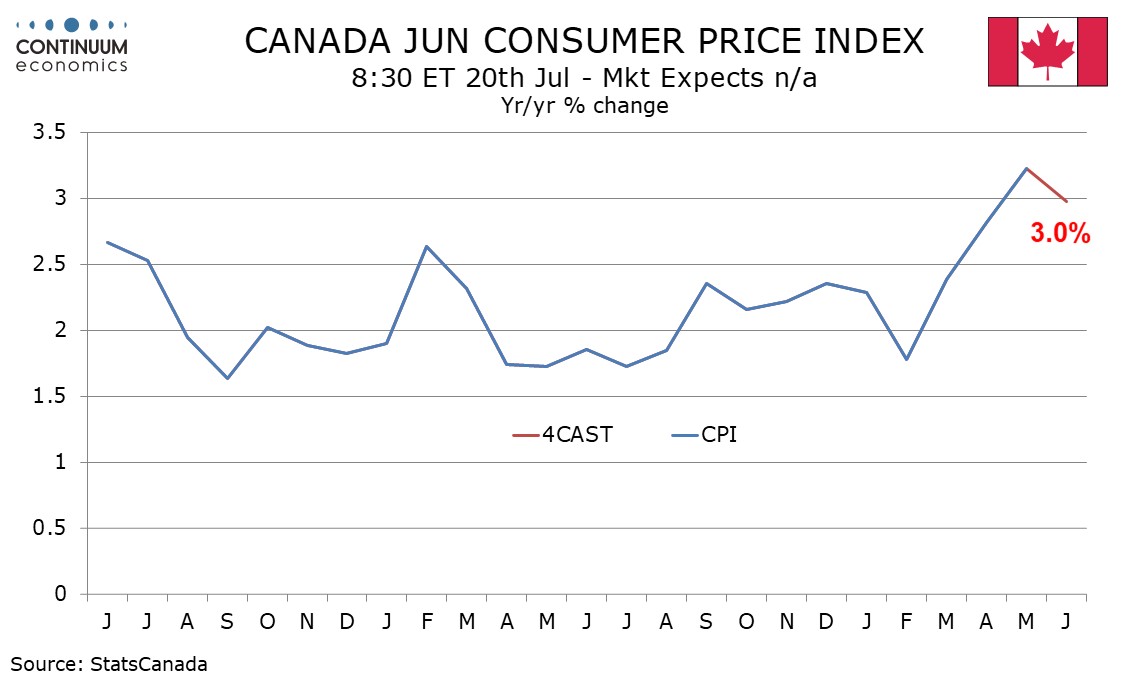

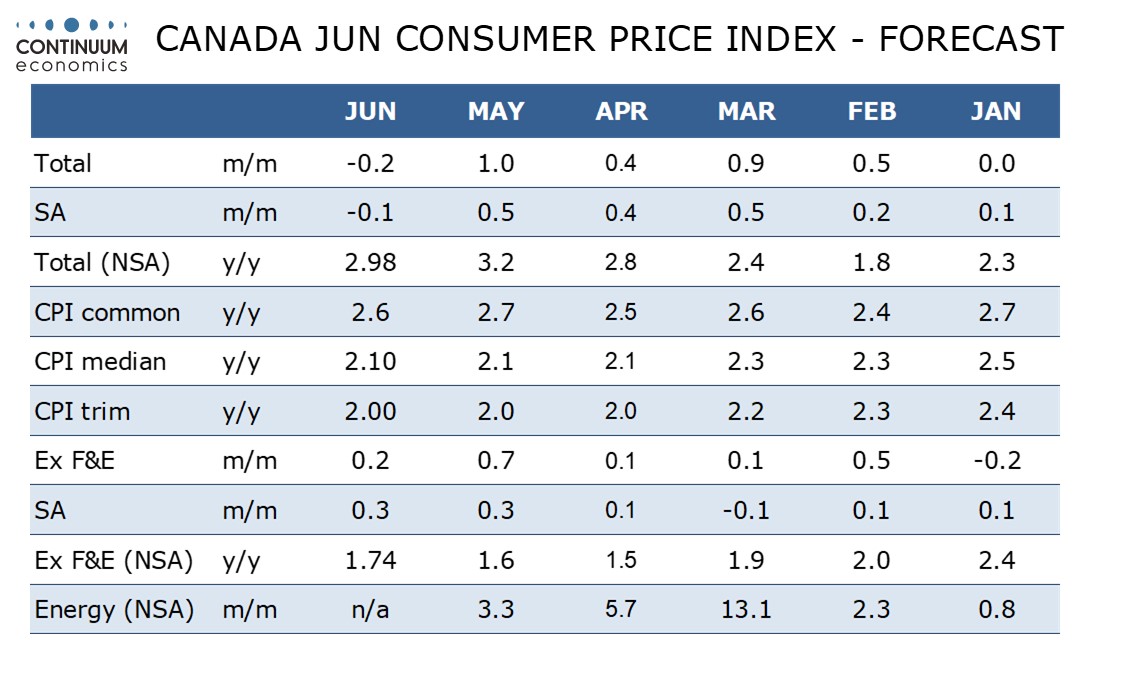

We expect June Canadian CPI to correct lower to 3.0% yr/yr from May’s 3.2% which was the highest since December 2023, with a slowing to 2.98% from 3.23% before rounding. The Bank of Canada’s core rates however are likely to remain mostly stable with CPI-Median at 2.1% and CPI-Trim at 2.0%, both for a third straight month.

On the month we expect CPI to fall by 0.2% overall with a 0.2% increase ex food and energy before seasonal adjustment, with seasonally adjusted data showing a 0.1% decline overall with a 0.3% increase ex food and energy. Gasoline prices have shown a significant correction from three straight months of sharp increases. Ex food and energy we expect a second straight rise of 0.3% after four straight months at 0.1% or less. Before rounding, we expect the ex food and energy increase to be only marginally above 0.25% before rounding, as was also the case in May.

With the economy returning to growth in Q2 the May bounce from the soft start of the year has scope to extend further, with the World Cup likely to provide modest support to prices in the Toronto and Vancouver areas. May’s seasonally adjusted data showed prices subdued outside monthly gains of over 1.0% in transport and recreation, education and reading, with air fares, traveller accommodation and travel tours all showing strong gains as well as gasoline. June’s gain may be broader based, but travel-related costs are unlikely to correct lower as soon as June even with the fall in energy prices, particularly given the continued influence of the World Cup.

We expect yr/yr growth ex food and energy to rise to 1.7% from 1.6%, extending a bounce from April’s 1.5% which was the lowest since March 2021. This is not one of the Bank of Canada’s core rates. For the BoC’s core rates we expect CPI-Common to slip to 2.6%, correcting a rise to 2.7% in May from 2.5% in April. However, we expect the more closely watched CPI-Median at 2.1% and CPI-Trim at 2.0% to match their April and May outcomes, with the gains remaining very close to 2.1% and 2.0% respectively even before rounding.