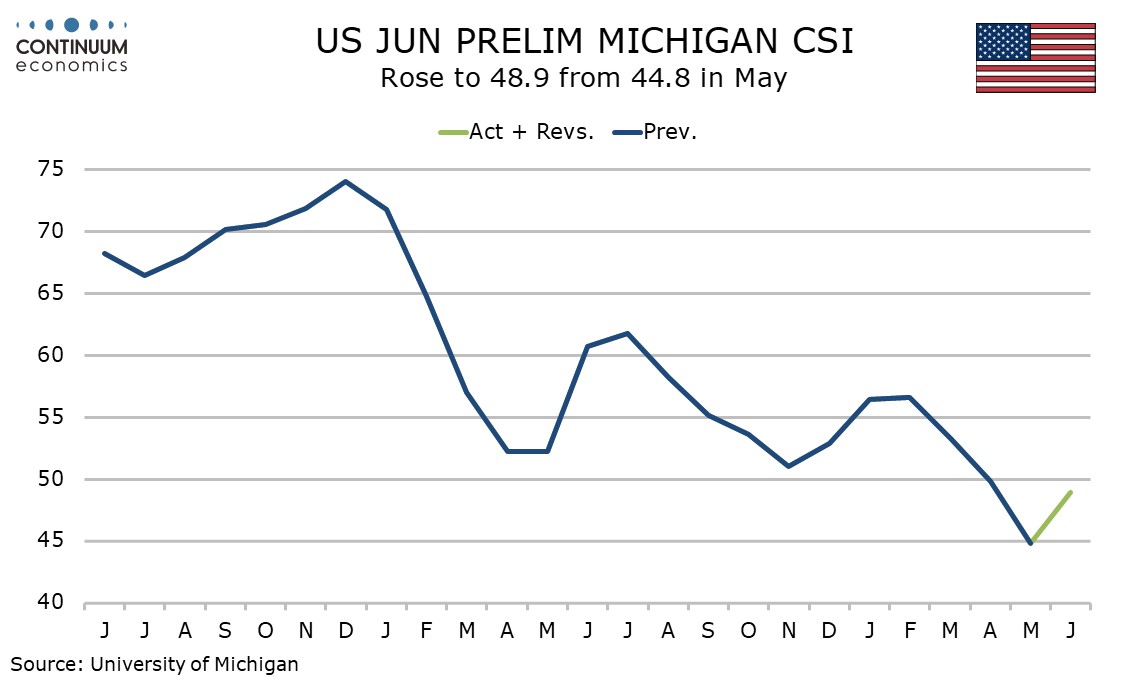

U.S. Preliminary June Michigan CSI - Rebounds from a very weak May final as inflation expectations correct lower

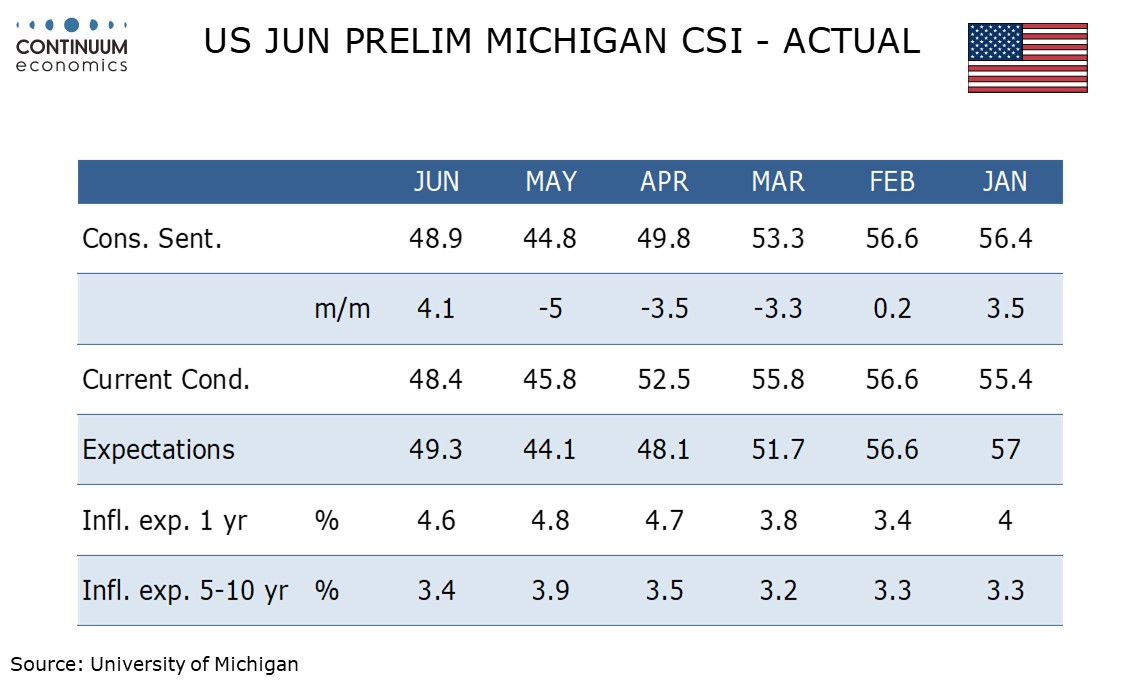

The preliminary June Michigan CSI at 48.9 has seen a surprising bounce from May’s final and record low of 44.8 but is not far off May’s preliminary of 48.2. Gasoline prices remain high but have slipped from May’s highs though the dip in May’s final now looks overstated.

Detail shows current conditions at 48.4 versus 45.8 in May’s final and 47.8 in May’s preliminary. Strength in the labor market may be supportive but there are hints in initial claims that this is fading in June.

Six month expectations at 49.3 are up from 44.1 in May’s final and 48.5 in May’s preliminary. Equity strength may be supportive though there have been some wobbles in early June.

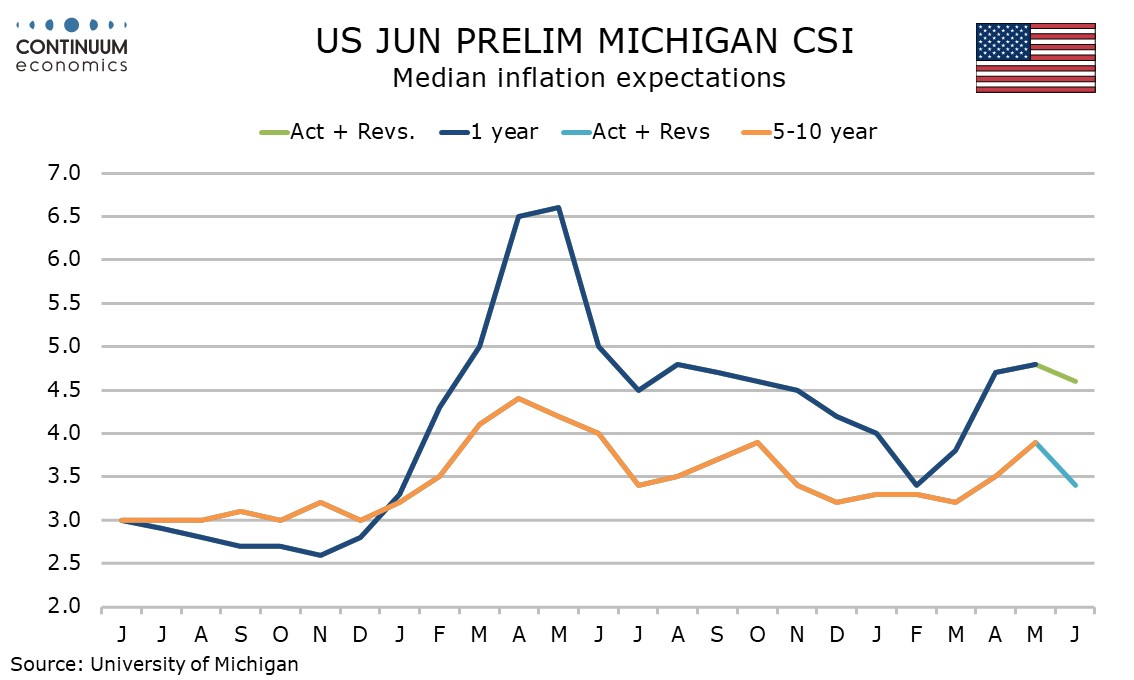

Inflation expectations are lower, with the 1-year view now at 4.6%, down from May’s final of 4.9% but still above May’s preliminary of 4.5%. This is best explained by short term moves in gasoline.

The 5-10 year view however saw a larger dip, to 3.4% from 3.9%, though this is unchanged from may’s preliminary of 3.4%. April also saw a preliminary of 3.4% with a modest upward revision to 3.9% in the final. The strength of May’s final now looks erratic, and that will be a relief to the Fed. Still, few have any real idea of how the situation in the Middle East will be resolved.