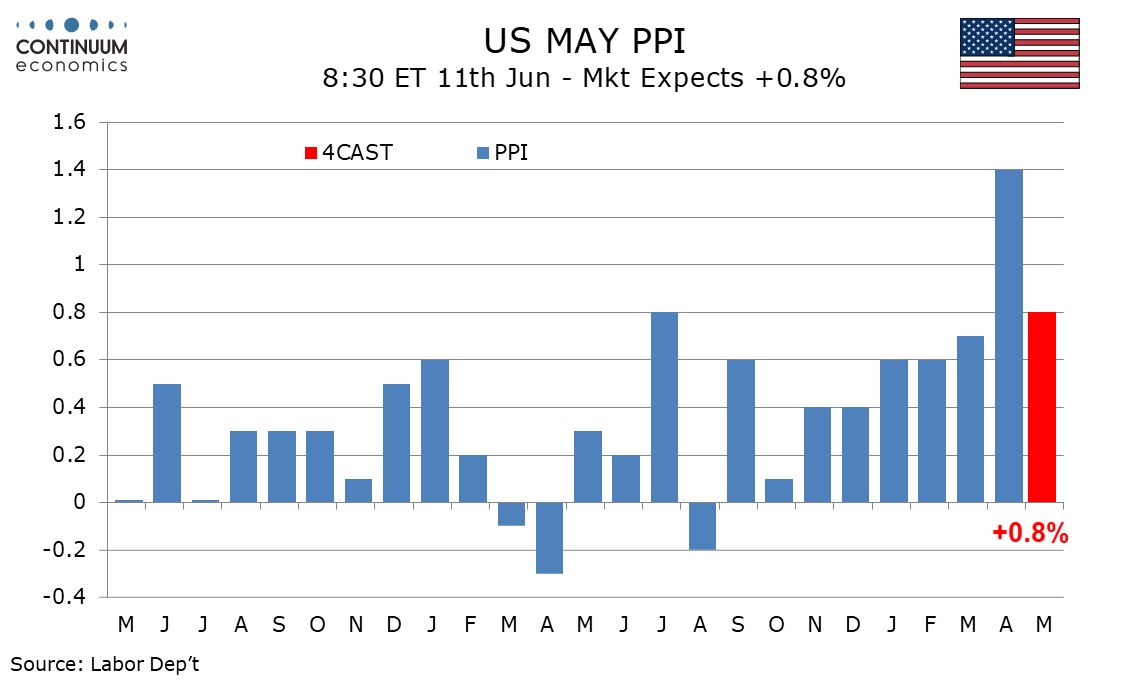

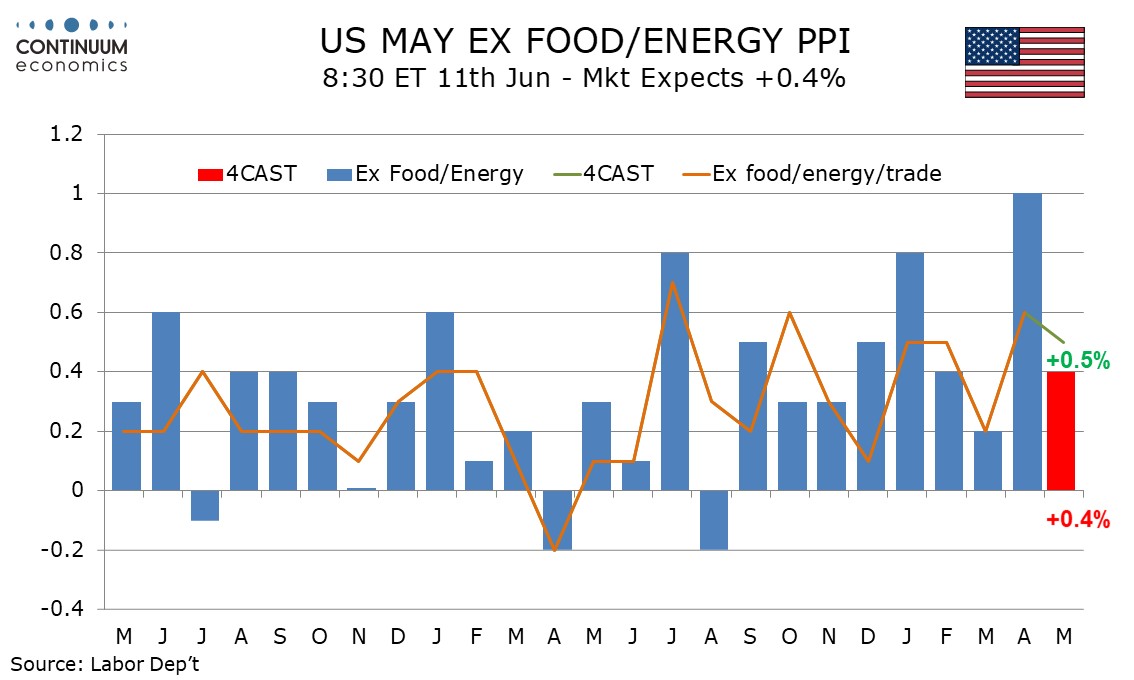

Preview: Due June 11 - U.S. May PPI - Strong if less so than in April

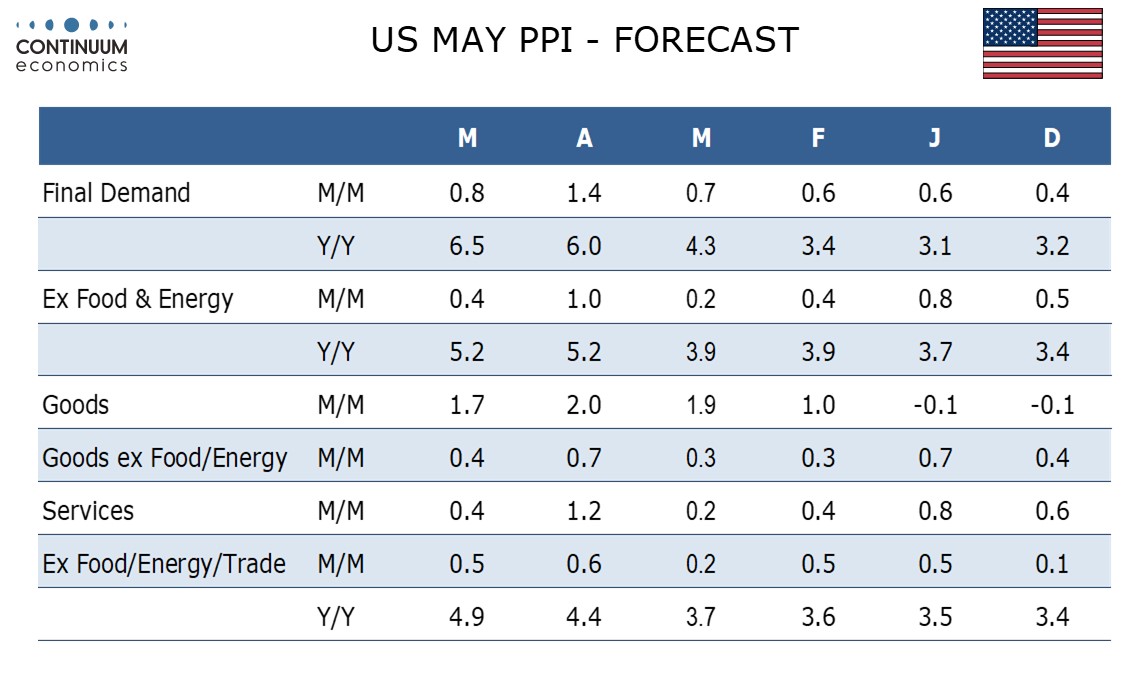

We expect PPI to rise by 0.8% overall in May, strong if slower than April’s 1.4% surge, with a 0.4% rise ex food and energy, significantly slower than a 1.0% increase in April. Ex food, energy and trade however we expect only a modest slowing, to 0.5% in May from 0.6% in April.

We expect a 1.7% rise in goods prices, down from 2.0% in April with energy at 7.5% versus 7.8% in April and food at 0.5% versus 0.2% in April. For goods ex food and energy we expect a 0.4% increase, down from 0.7% in April but stronger than 0.3% gains seen in February and March. With the tariff impact fading and we doubt April’s core strength will be matched on a sustained basis despite the ongoing supply disruptions coming from the Middle East.

We also expect a 0.4% rise in services after a 1.2% April increase. April saw an unusually strong rise in the volatile trade sector of 2.7% which we expect to correct lower by 0.5% in May, leaving PPI ex food, energy and trade slightly stronger at 0.5% than the 0.4% rise ex food and energy. Transportation and warehousing was stronger still at 5.0% in April, probably influenced by the Middle East. We expect a rise of 2.5% in May, still firm if less so. Other services, which make up the majority, rose by only 0.1% in April after a flat March. We expect a 0.2% increase in May.

We see yr/yr growth rising to 6.5% from 6.0% overall, which would be the strongest since December 2022. Ex food and energy we expect the yr/yr pace to remain at April’s 5.2% pace, which was the highest since December 2022. Ex food, energy and trade, we expect a yr/yr pace of 4.9%, up from 4.5% in April and this would be the highest since November 2022.