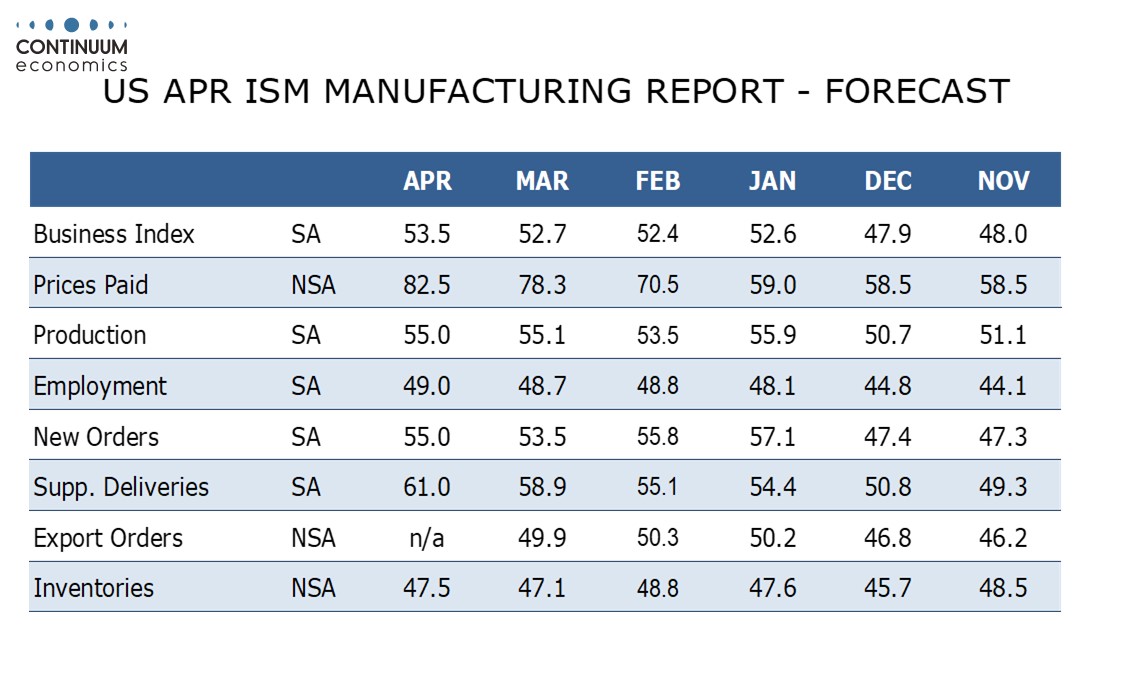

Preview: Due May 1 - U.S. April ISM Manufacturing - Highest composite and prices paid since 2022

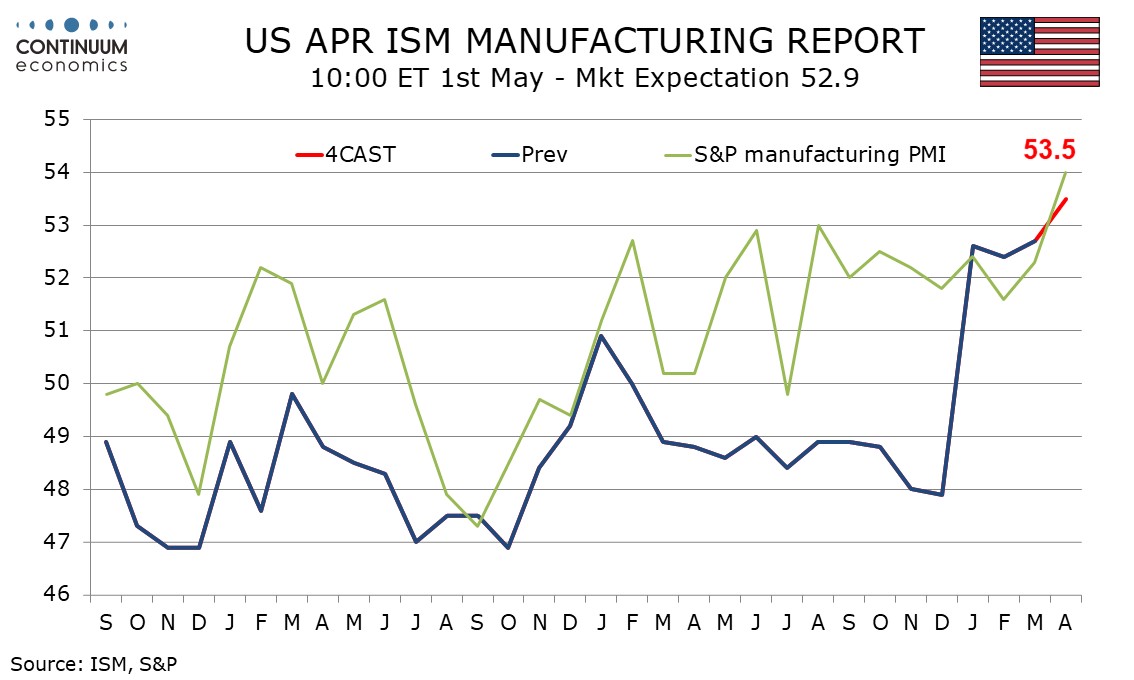

Despite risks coming from the Middle East, we expect April’s ISM manufacturing index to increase to 53.5 from 52.7, delivering a fourth straight clearly positive reading and the highest level since June 2022.

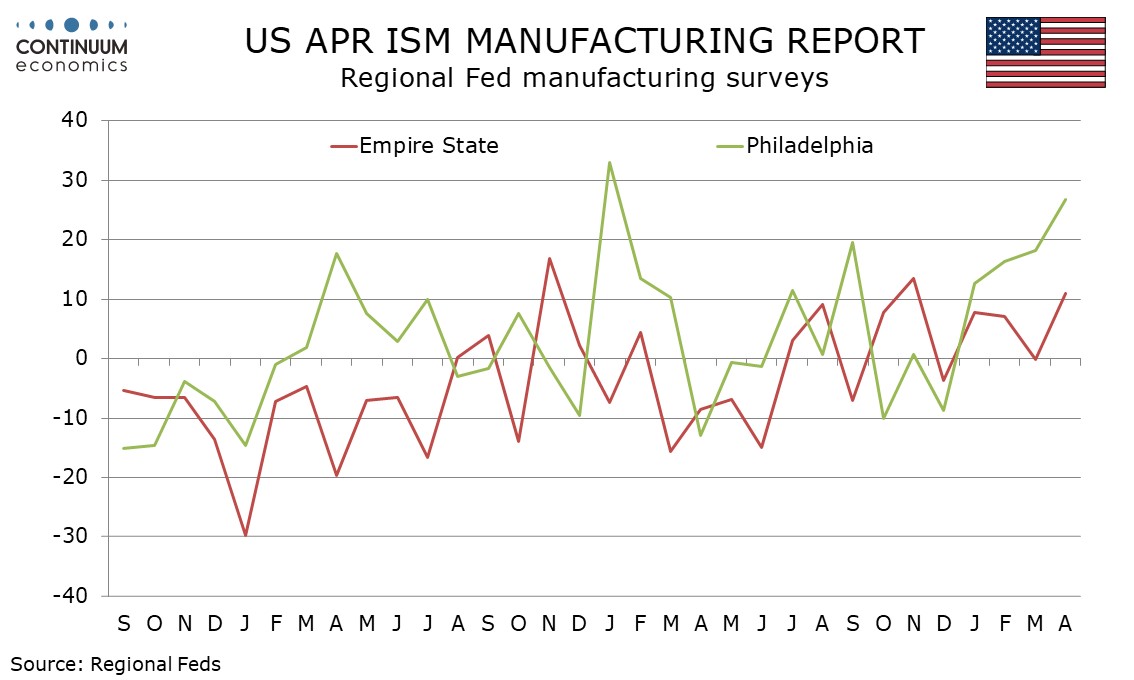

Signaling a stronger reading are improved data from the S and P manufacturing index, Philly Fed and Empire State surveys.

These surveys suggest a bounce in new orders after two straight slowings, we expect to 55.0 from 53.5. We expect production to be little changed at 55.0 from 55.1 and only marginal increases in employment and inventories, to still negative levels. Delivery times may be inflated by war-related supply shortages and we expect a rise to 61.0 from 58.9, completing the breakdown of the composite.

Prices paid do not contribute to the composite but are also likely to be lifted by the situation in the Middle East, we expect to 82.5 from 78.3. This would be the highest level since April 2022.