Preview: Due July 1 - U.S. June ISM Manufacturing - Sustaining May's bounce

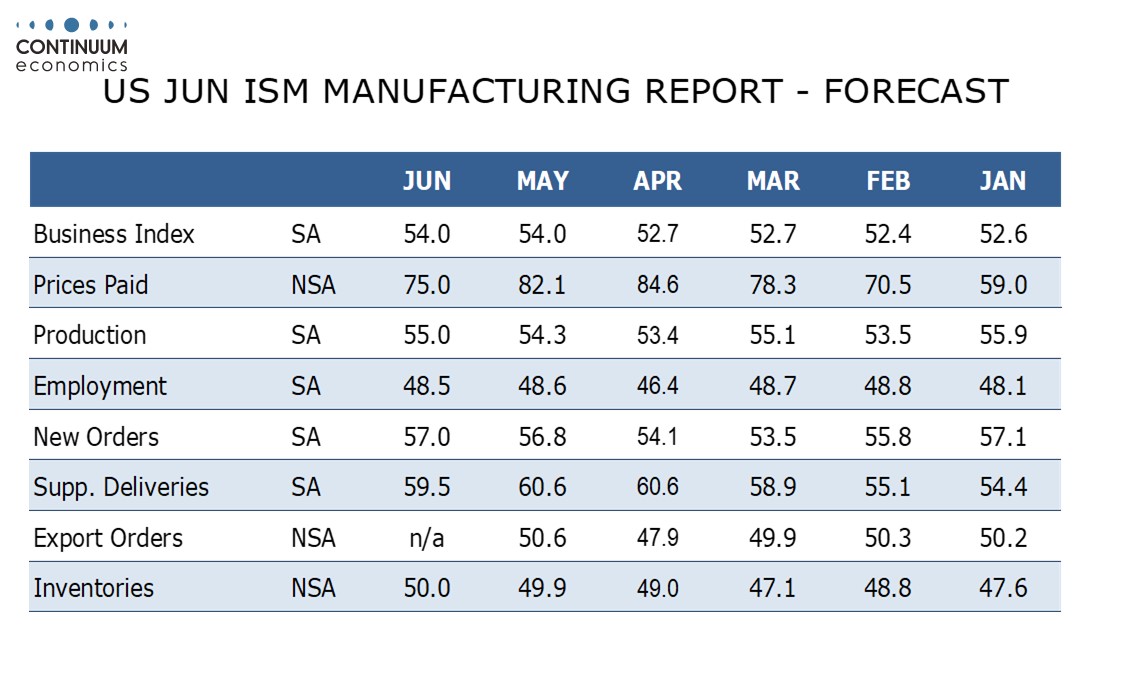

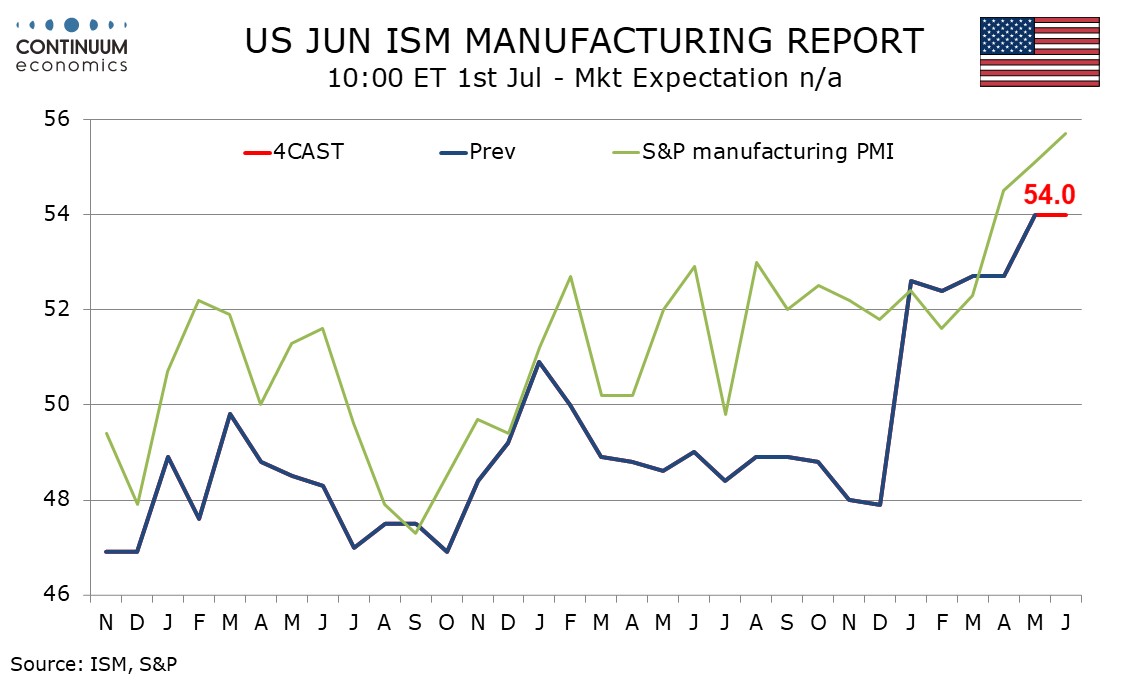

We expect an unchanged June ISM manufacturing index of 54.0, sustaining a May bounce from April’s 52.7 to reach the highest level since May 2022. Strong business investment remains supportive.

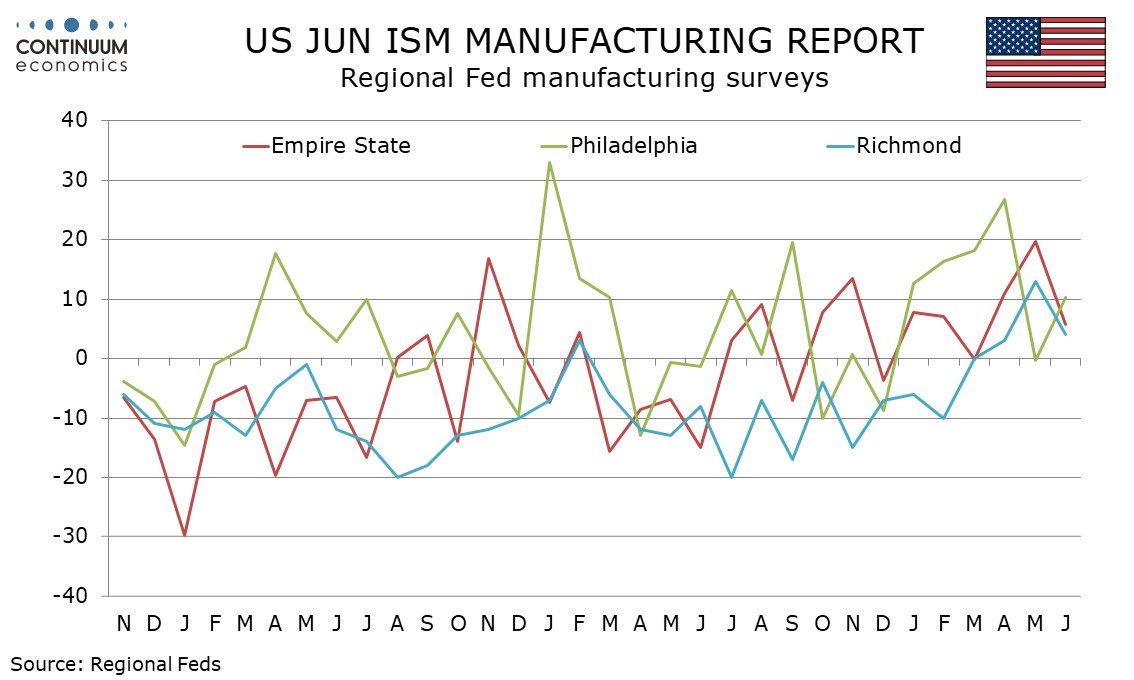

Signals from other surveys are mixed. The S and P manufacturing PMI accelerated still further in June, but the Richmond Fed and Empire State surveys lost momentum while the Philly Fed’s, while improved from a weak May, remained off recent highs.

May ISM details showed new orders particularly impressive at 56.8 and supportive June seasonal adjustments could lift that index further, we expect to 57.0. Strong new orders should help lift production to 55.0 from 54.3. We expect inventories at 50.0 and employment at 48.0 to be almost unchanged from May.

There is however scope for slippage in delivery times as Middle East generated supply disruptions ease, we expect to 59.5 after two straight months at 60.6, to complete the breakdown of the composite. Prices paid do not contribute to the composite, but should also see some slippage, falling to a 4-month low of 75.0 from 82.1, still well above pre-conflict levels that had fallen below 60.0.