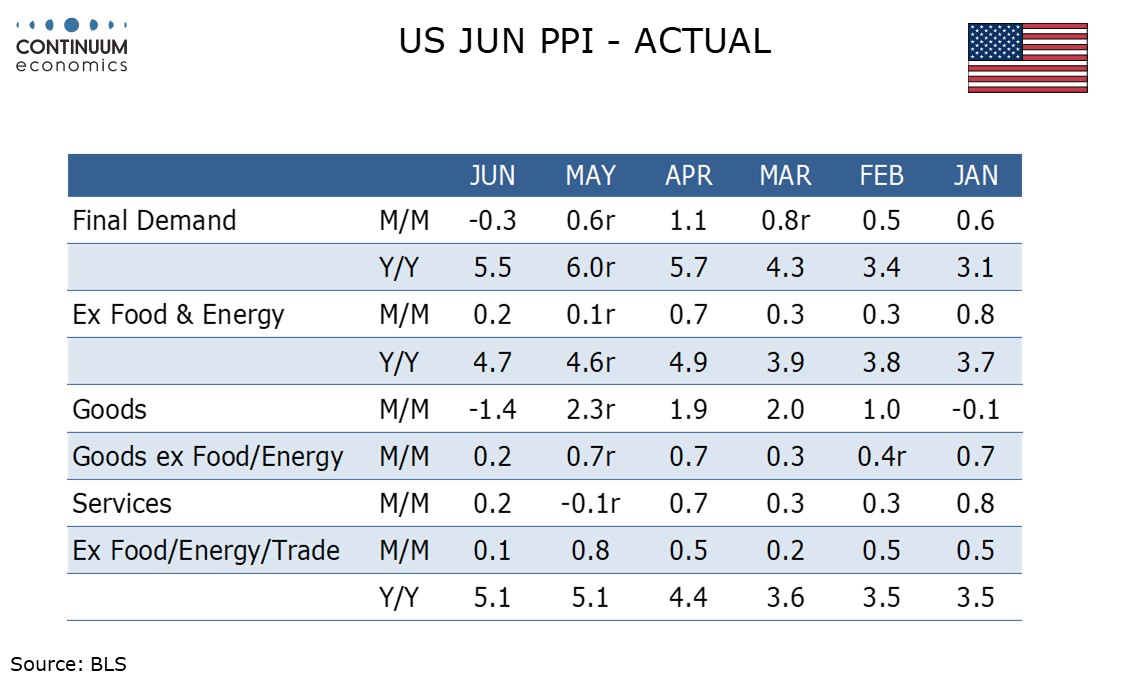

U.S. June PPI - Lower than expected with May revised down, but still firm yr/yr

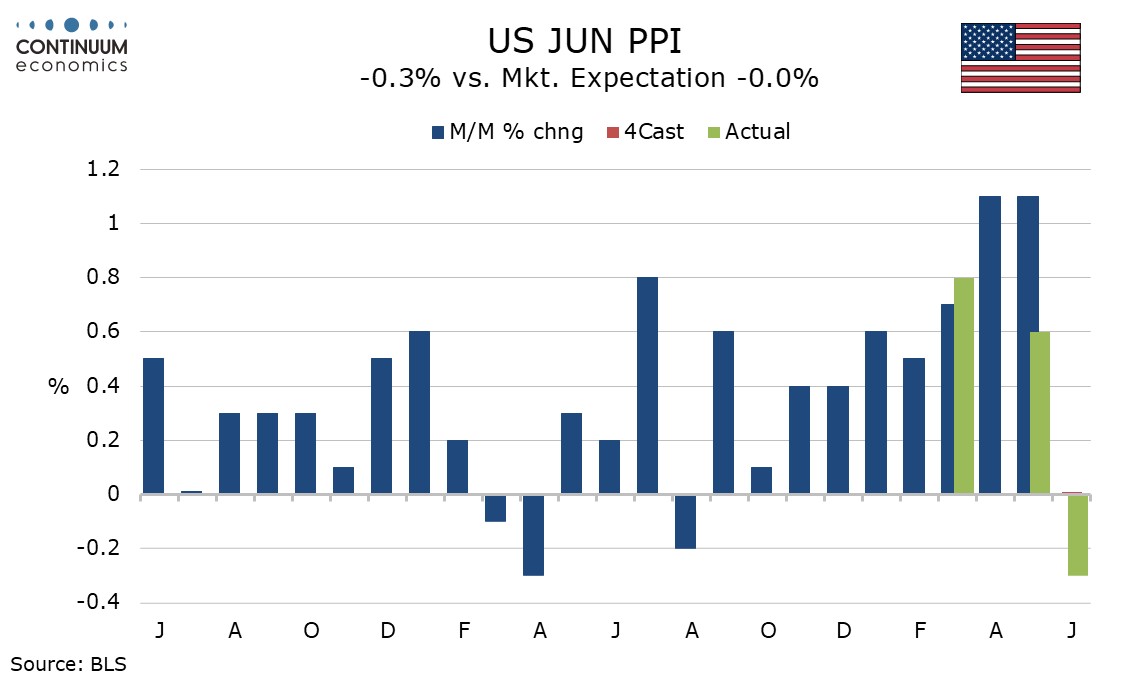

June PPI is on the low side of expectations, -0.3% overall, +0.2% ex food and energy and +0.1% ex food energy and trade. The weakness can be seen as corrective from preceding strength though a downward revision to May adds to the negative surprise.

Overall May PPI now increased by 0.6% rather than 1.1% while ex food and energy has been revised down to a 0.1% increase from 0.4%. May’s ex food, energy and trade gain however is unrevised at 0.8%, and the 0.1% June ex food, energy and trade gain needs to be seen alongside that.

Energy fell by 6.4% after a rise of 8.4% in May, with gasoline down by 12.0% after a 20.9% rise in May, that was a third straight strong gain. Food also fell, by 0.6% after a 0.5% May increase, with grains falling by 12.0% after a 10.2% May increase.

Goods less food and energy rose by 0.2% after two straight gains of 0.7%. Services rose by 0.2% after a 0.1% a May decline but May’s weakness was fully due to a 2.3% decline in the volatile trade sector which rose by 0.4% in June. Transport and warehousing fell by 0.1%%, its first fall in 12 months, after three straight strong gains, as war-related supply issues faded, while other services rose by 0.1% after a 0.7% May increase that was led by some financial services.

Yr/yr PPI at 5.5% is still firm if down from 6.0% in May. Yr/yr PPI ex food, energy and trade at 5.1% matches May’s pace while the ex food and energy pace picked up to 4.7% from 4.6%.

Intermediate goods data was soft at -1.2% for processed goods and -4.1% for unprocessed goods, with respective ex food and energy rates of +0.6% and -1.2%. Intermediate services saw a modest 0.3% increase.

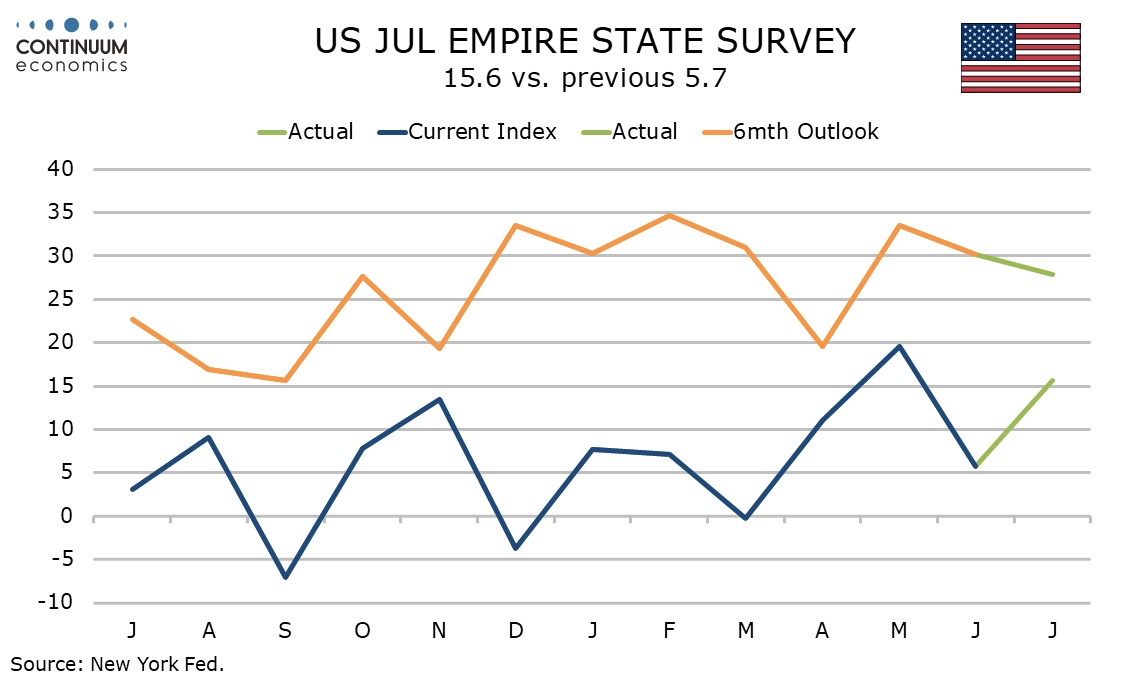

July’s Empire State manufacturing survey saw renewed strength with an index of 15.6 from 5.7 but six month expectations fell to 27.9 from 30.1. Price indices both received and paid, one month and six month, fell to 3-month lows, with six month expectations for prices paid at a 4-month low.