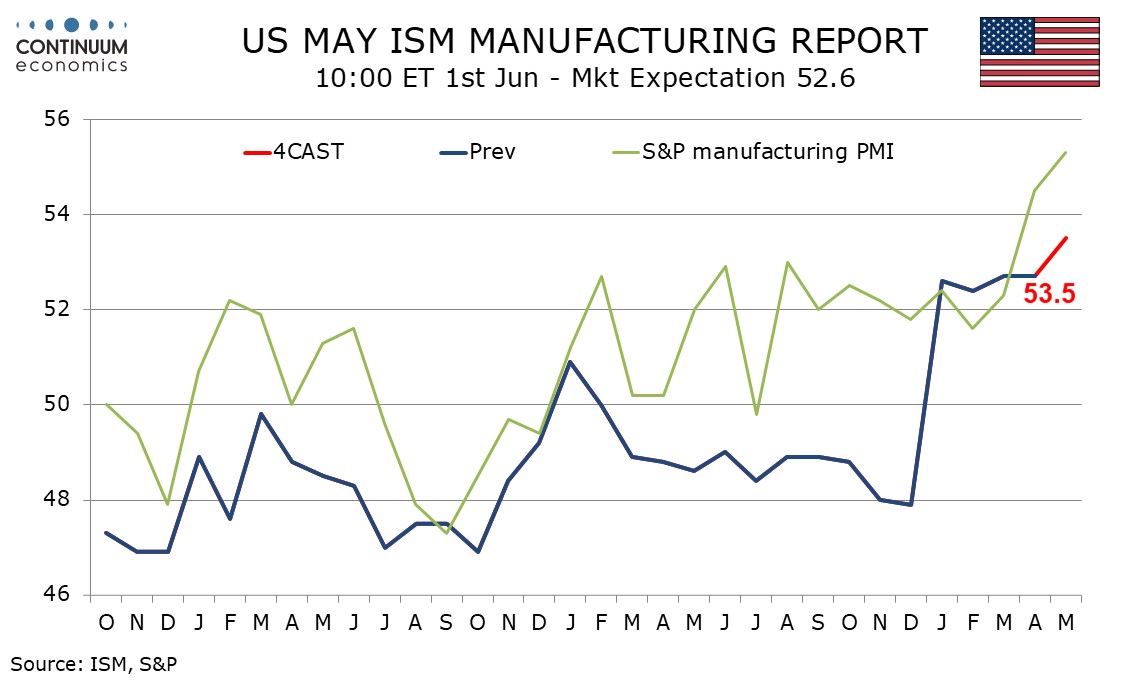

Preview: Due June 1 - U.S. May ISM Manufacturing - A renewed acceleration

We expect a rise in May’s ISM manufacturing index to 53.5 from 52.7, reaching its highest level since June 2022 after four straight similar months, extending the improvement from negative late 2025 readings.

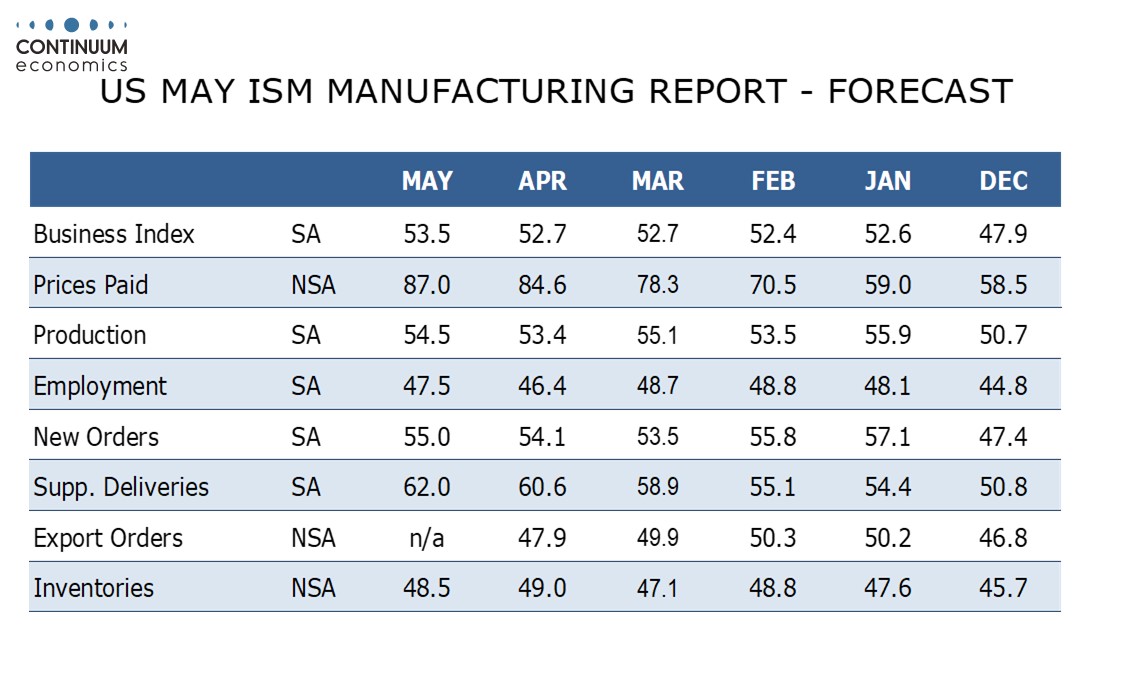

We expect improvements in four of the five components that make up the composite, with new orders and production assisted by seasonal adjustments. These two indices, as well as employment, will however remain short of recent highs, with employment still below neutral.

Delivery times have picked up as the Middle East conflict creates supply problems, and we expect a sixth straight acceleration to 62.0 from 60.8 in April. Prices paid do not continue to the composite, but we expect a further acceleration here too, if less sharp than in recent months, to 87.0 from 84.6. This would be the highest level since Mar 22, seen after Russia’s invasion of Ukraine.

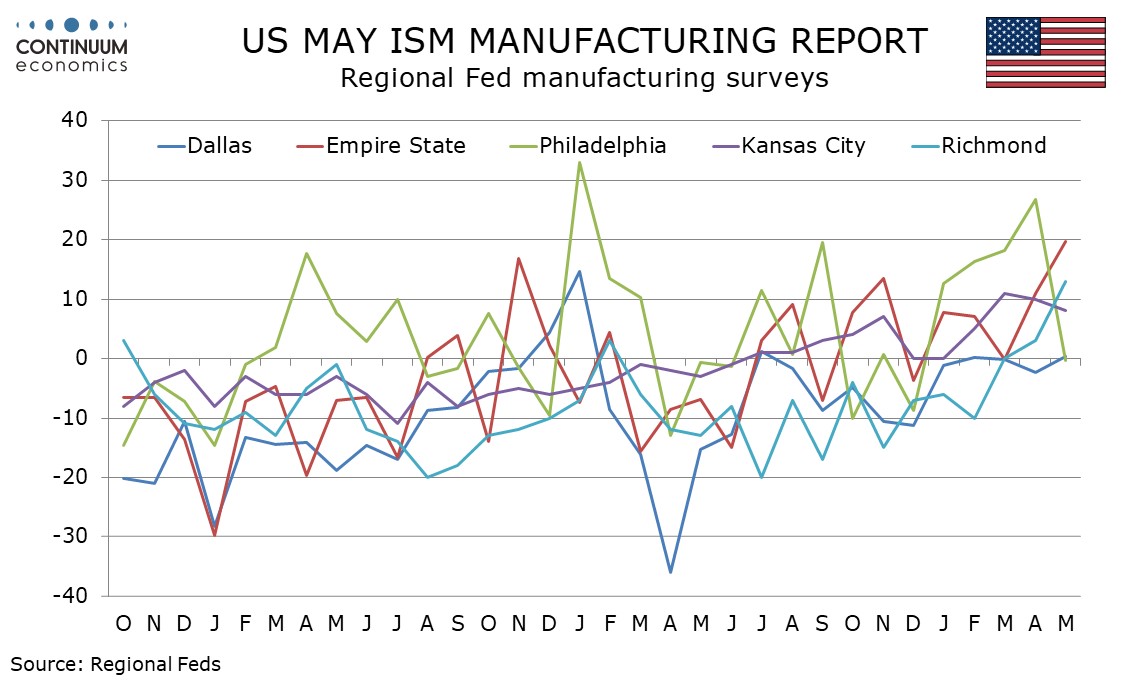

Acceleration in the ISM manufacturing index would be consistent with positive signals from the S and P manufacturing PMI. Regional Fed signals are mixed, with the Empire State and Richmond Fed indices stronger, Dallas and Kansas City Fed indices only moderately changed but the Philly Fed index dipping marginally below neutral after a very strong April.