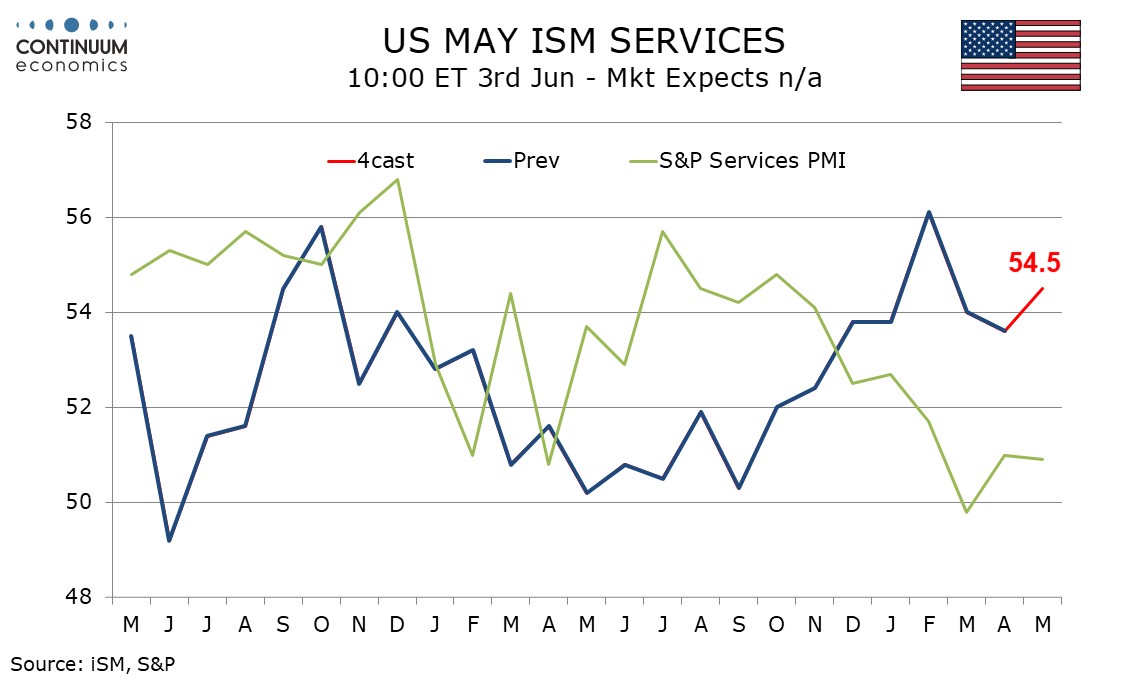

Preview: Due June 3 - U.S. May ISM Services - Seasonal adjustments may provide a lift

We expect May’s ISM services index to pick up to 54.5 from 53.6 in April, picking up after two straight declines from February’s 56.1. While rising energy prices are a downside risk for services activity, seasonal adjustments may provide some support in May.

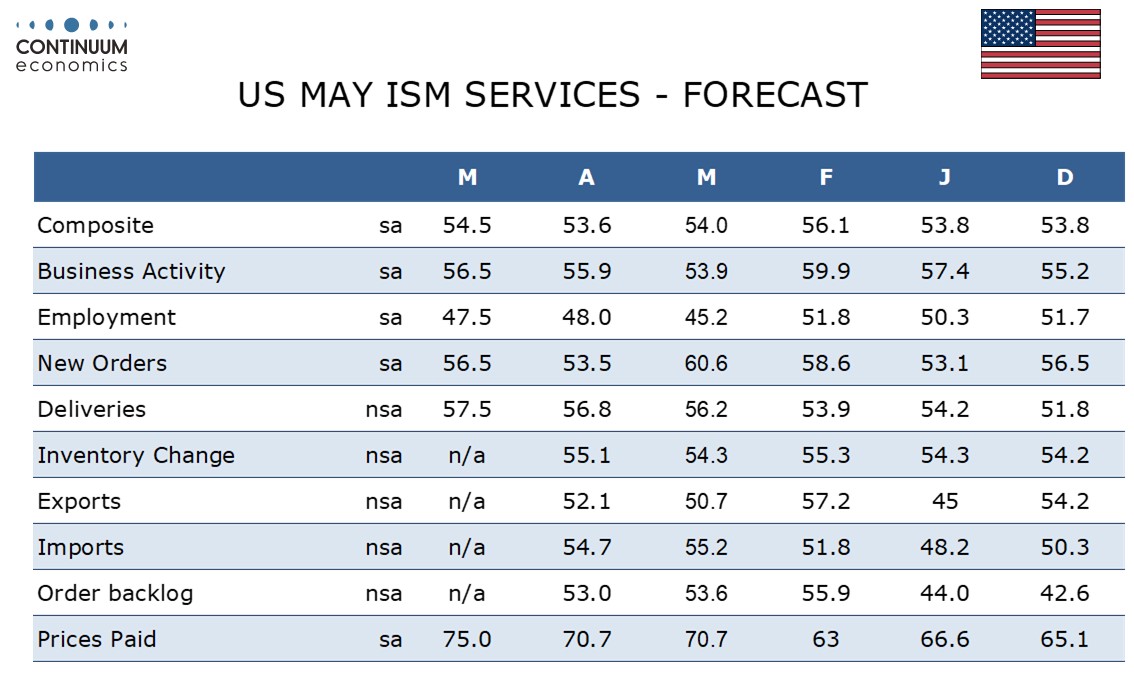

We expect outcomes of 56.5 for both business activity and new orders, picking up from 55.9 and 53.5 respectively, both benefiting from easier seasonal adjustments. We expect supply shortages coming from the Middle East conflict to bring a further acceleration in delivery times, to 57.5 from 56.8. Only in employment of the four contributors to the composite do we expect slowing, to 47.5 from 48.0.

Prices paid do not contribute to the composite and here we see a rise to 75.0 after April saw a pause, remaining at March’s level of 70.7. This will be the highest reading since June 2022.

Our forecast is a little stronger than what is implied by others service sector surveys. The Richmond Fed’s was stronger, but S and P’s and Dallas Fed’s little changed and still subdued. The Empire State index was less negative, but the Philly Fed’s increasingly so.