Europe Summary and Highlights 28 May

Overnight blips faded, oil stays towards the lows so long as talks not declared derailed

Volatility continues to compress

European morning session

The European morning largely consolidated and slightly faded the overnight action. Oil currently proving very capped towards the May lows.

The market is tending to fade any blips on fresh skirmishes for now - at least so long as there’s no indication that talks have stopped proceeding. Oil overnight gains halved to around $1.5, and nearer yesterday’s lows than highs.

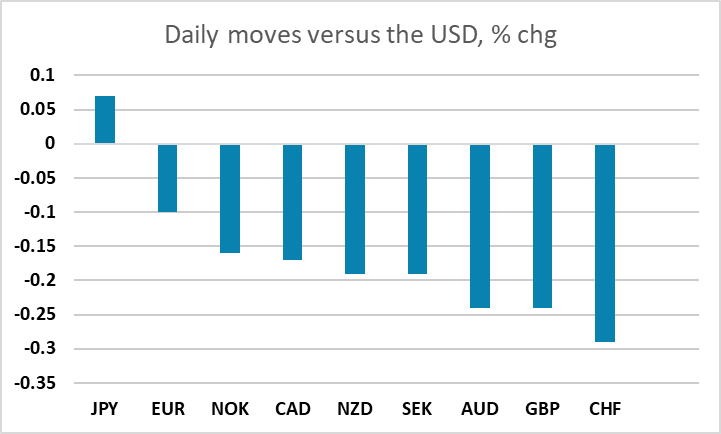

FX action very dull accordingly, the dollar only modestly in the plus still. Recent realised action and lack of decisive drivers tending to see volatility further collapse.

Cable a touch softer but largely looking a case of further range action on EUR/GBP, as it has been lifting back off the well-established band floor in recent sessions again.

In terms of data, not a huge amount of interest. Italian May consumer confidence above expectations at 93.4 from 90.8 (mkt 90.1). Norway mainland GDP +0.2%q/q in Q1 vs mkt 0.3%.

Asia Session

The risk sentiment turned sour on Thursday as more explosions are heard near Bandar Abbas, Strait of Hormuz. U.S. said such action is defensive while Iran accused an American tanker tried to pass. Such incident is giving market participants second thoughts on whether a deal is near. U.S. major equity indexes and most regional equities are lower. AUD/USD is trading 0.5% lower at 0.7106 as precious metal also treads lower. NZD/USD is also 0.54% lower while USD/CAD rises 0.16% with both Brent and WTI higher.

The haven bids for USD are revived on more bombings in the Middle East. The ceasefire is officially done with both sides exchanging fire. It is hard to tell whether background negotiations are still going and both sides are just showing their leverage. USD/JPY is trading 0.05% higher at 159.58. Else, EUR/USD is down 0.3% and GBP/USD is down 0.36%.