Europe Summary and Highlights 5 Jun

Range action holds, tired risk mkt tone shrugged of in morning session

Focus turns to US payrolls

European morning session

Trapped in familiar ranges ahead of US payrolls on a quiet morning.

If anything, slight bias in recent sessions for Europe to be seeing glass half full and US more half empty when it comes to Iran backdrop, and the USD lean.

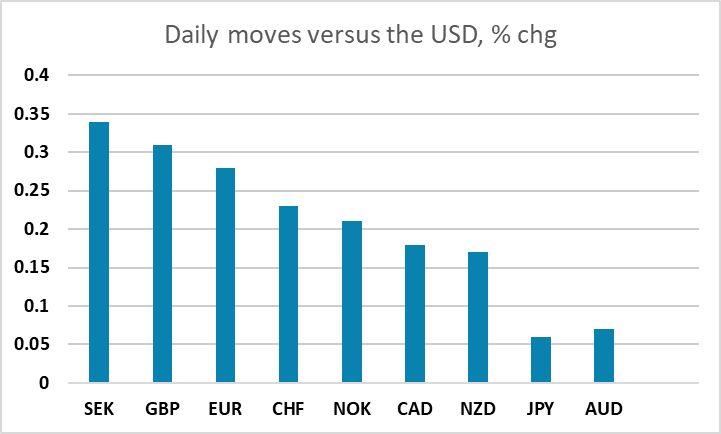

Crude holding flat to -1% over session. USD/JPY sat off 160, EUR/USD lifted slightly into mid 1.16-1.1650 zone. Higher beta pairing holding up despite the fact that tech markets have been showing some tiredness the last few sessions (Kospi -5.5%, Nasdaq future -1%, metals -1%-2%).

EZ Q1 GDP revised to -0.2%q/q from 0.1%, 0.3%y/y from 0.8% - downward distorted by sharp Irish GDP drop (GNP firmer), though breakdown is still soft all the same.

Italy retail sales flat m/m, 1.6%y/y unadj

UK Halifax house prices -0.1%m/m, 0.5%y/y.

Asia Session

As USD/JPY flirts with the 160 level, we heard Japan FM Katayama suggesting readiness to respond to FX. It of course did little to reverse the trajectory of USD/JPY, barely keeping the pair under the figure. Fundamentally, we do see wage gains exceeding expectation at 3.5% y/y and could contribute to stronger inflation in a medium run. If such persist, the rate expectation could change from the currently 1% terminal rate we are seeing to as high as 2% but only time will tell. USD/JPY is trading 0.06% lower at 159.92.

It is reported that Oman's Mina al Fahal crude terminal on the Gulf of Oman has been forced to suspense oil loading from drone attacks. Such is the first time, Oman, a relatively neutral country, being dragged into the conflict. Major equity indexes are reacting negatively to the news. AUD/USD is trading 0.08% lower at 0.7128. NZD/USD is trading unchanged while USD/CAD slips 0.04%. Both Brent and WTI are slightly higher. Else, EUR/USD is up 0.04% and GBP/USD is up 0.03%.