Europe Summary and Highlights 22 Jun

UK PM Starmer resigns, but no impact as fully expected

Iran talks progress steadies risk and oil

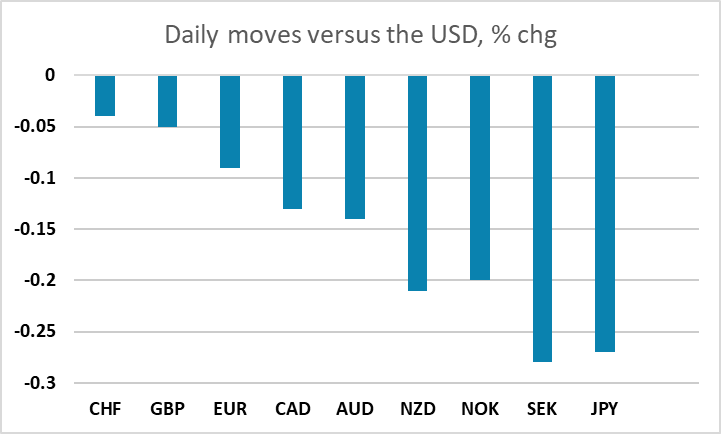

Dollar holds a firm tone

European morning session

UK PM Starmer confirms that he will resign, with nominations for the leadership opening on July 9th. Sterling unmoved as the outcome - and Burnham’s succession - already viewed as a given.

Otherwise, a relatively subdued European morning, holding on to the intraday risk improvement seen over the course of the Asia session after progress made on Iran talks in Switzerland, following the tense weekend - Nikkei and Kospi finishing firmer, Nasdaq now also into the plus at 0.1%, and Brent reversing to be off -$1.5

Dollar remains firm, holding on to the minor net gains, and remaining a solid footing out of the recent upside break. USD/JPY still pressuring into the highs, still testing intervention threats amid the dollar-led action.

Asia Session

There is a breakthrough in Switzerland as Iran agreed to the Hormuz maritime security mechanism. It is a welcoming surprise after the week end ebbs and flows. U.S. major equities rebounded from opening low, so as precious metal. AUD/USD is trading 0.09% lower at 0.7007 after filling the gap lower. NZD/USD is trading 0.18% lower while USD/CAD rises 0.22% with both Brent and WTI reversing early gap up to trade more than a dollar/b lower.

The improvement in risk sentiment does not seem to be driving any USD offers, instead the ongoing uncertainty are driving USD bids. The push and pull will paint a difficult picture for any sustained rally in risk asset. USD/JPY is aiming to revisit June high at 161.64, 0.25% higher for the session after opening lower. Else, EUR/USD is down 0.05% and GBP/USD is down 0.13%.