Europe Summary and Highlights 2 Jun

Subdued morning, some calm after Mon's concerns, but still uncertainties

Crude sits just off $90, mid range for last few days

European morning session

Subdued European morning, some calm after Monday’s Iran concerns, but the dollar not backing off much further at this point. Crude sits back just off $90 now, off Monday’s near $95 highs but still off the mid $80 lows of last week.

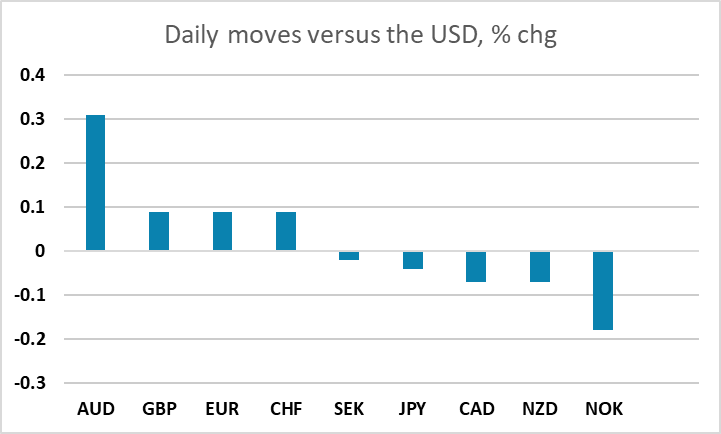

EUR/USD back to sitting off 1.1650~ area, USD/JPY still poised under 160 (159.70s), higher beta pares a bit circumspect (SEK and NZD back to nearer flat on the day now).

Iran's Mehr News says Iran still reviewing, has not yet responded to the US' latest proposed final agreement.

EZ May HICP at 3.2% from 3.0%, in line with market. Ex food, energy, alcohol, tobacco 2.5% from 2.2% (mkt 2.4%).

UK April consumer credit £1.86bn vs mkt £1.7bn, mortgage approvals 65.9k (mkt 62k), M4 +0.2%m/m.

European Parliament committee voted to remove EU import duties on many U.S. goods, moving to comply with US trade deal. Legislation still needs to be approved by full EU assembly.

Asia Session

While RBA's Harper sound hawkish, it is hard to see RBA to hike the fourth time in a row when monthly CPI has begin moderating. On the other hand ,we have Trump telling ABC that a deal is near, again. Market participants doe not seem to react to such cry of the wolf anymore. U.S. major equity indexes are in the red while regional equities performing individually. AUD/USD is trading 0.04% higher at 0.7164. NZD/USD is trading 0.05% while USD/CAD rises 0.02% on lower oil.

It is reported that the White House is trimming tariffs on farm and industrial gear to 15%. That looks like Trump tried to keep the inflationary pressure lower from the prolonged Iran conflict. USD/JPY is gathering steam beneath 160 to trade 0.04% higher at 159.72. Else, EUR/USD is up 0.06% and GBP/USD is up 0.08%.