Published: 2024-01-08T13:54:02.000Z

Preview: Due January 9 - U.S. November Trade Balance - Deficit to rise with both exports and imports lower

-

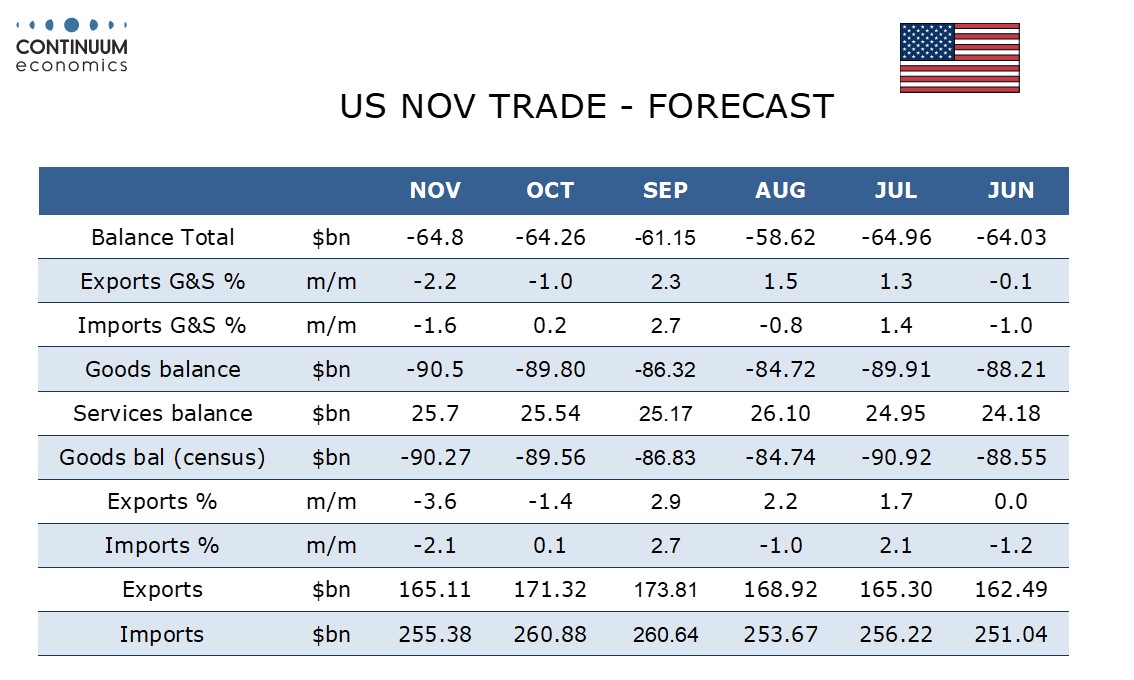

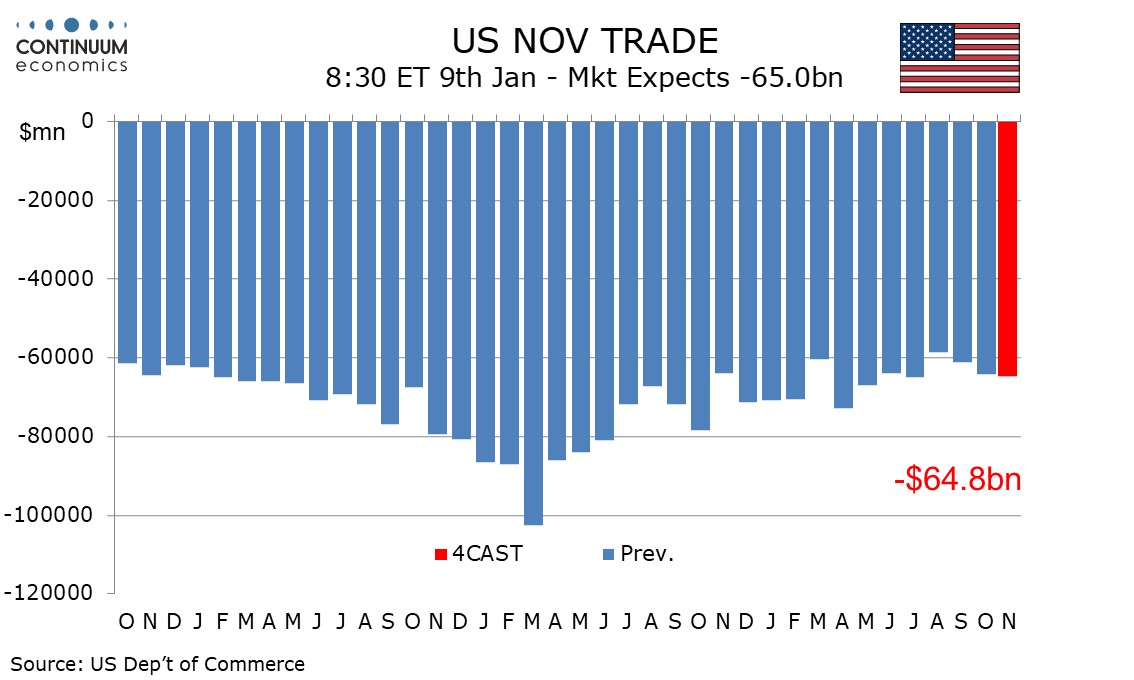

We expect a November trade deficit of $64.8bn, wider than October’s $64.3bn and a third straight deterioration, though over the last year trend has been fairly flat.

We expect a 2.2% decline in exports and a 1.6% decline in imports.

Advance goods data showed exports down by 3.6% and imports down by 2.1%, with the falls in both cases being led by volumes though prices did slip too. For services we expect gains of 0.7% in both exports and imports.