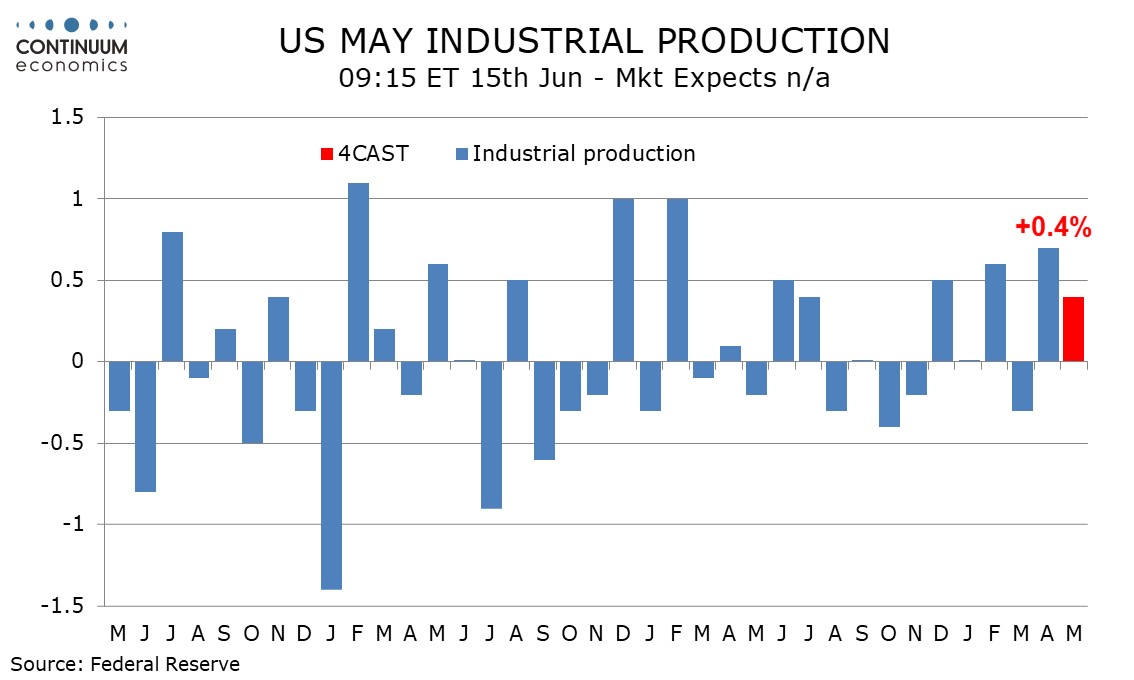

Preview: Due June 15 - U.S. May Industrial Production - Improvement in trend to continue

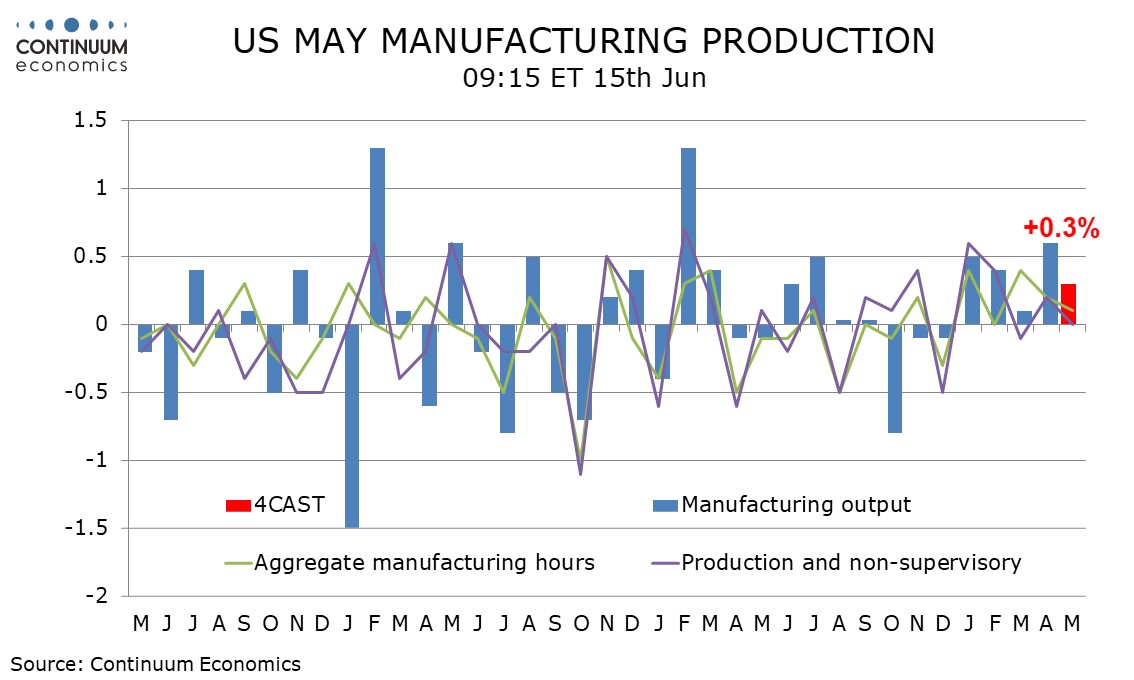

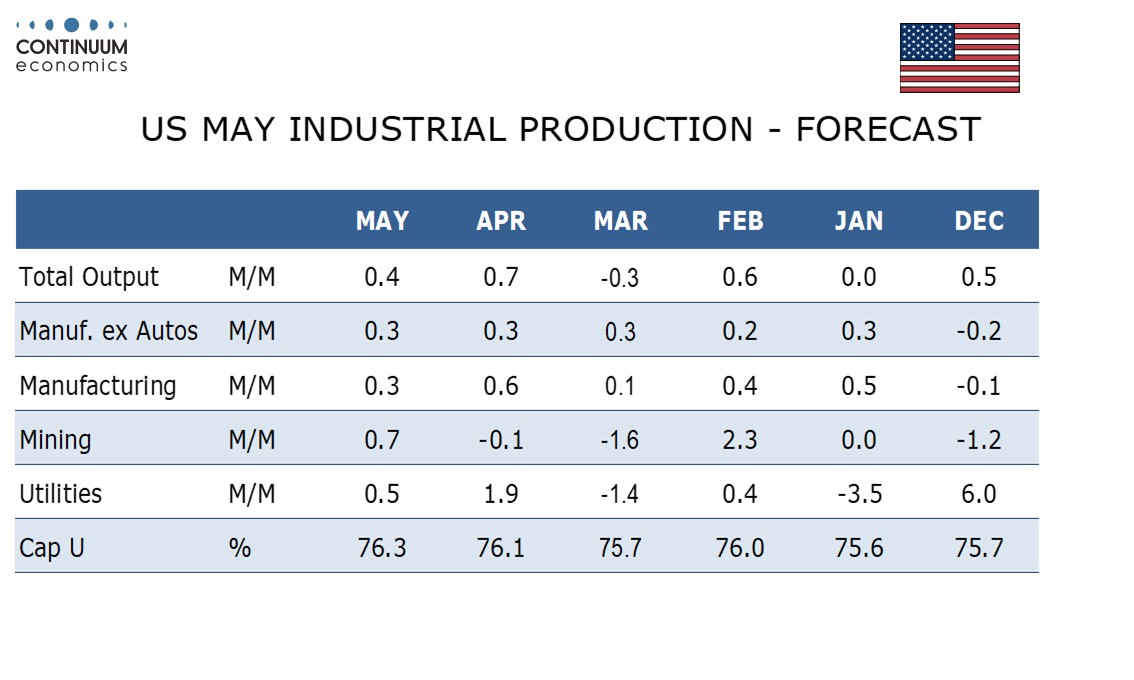

We expect a 0.4% increase in April industrial production with a 0.3% increase in manufacturing, the latter seeing a fifth straight gain to confirm a positive trend.

Manufacturing signals have generally been picking up with the ISM manufacturing survey increasingly positive in May, the spread of AI supportive. May’s non-farm payroll showed aggregate hours worked in manufacturing only marginally improved, but with productivity gains should allow a rise in output.

We expect a neutral contribution from autos after an April bounce corrected a March decline. We expect a third straight 0.3% increase in manufacturing ex autos, and the fourth such rise in five months, the exception being a similar 0.2% increase in February.

Weekly electrical output data suggests a modest rise in utilities while non-farm payrolls show an increase in aggregate hours worked in mining, possibly supported by higher oil prices, implying a rise in output, even if uncertainty over how long they will persist keeps the oil industry cautious over expanding output. This will lift overall industrial production slightly above manufacturing.

We expect capacity utilization to increase to 76.3% from 76.1% with manufacturing at 75.9% from 75.8%. These would be the highest since February 2025 and August 2025 respectively, further illustrating a recent improvement in trend.