Europe Summary and Highlights 14 Jul

FX still currently neutralised, in parts, as oil rises and hike odds broadly lifted

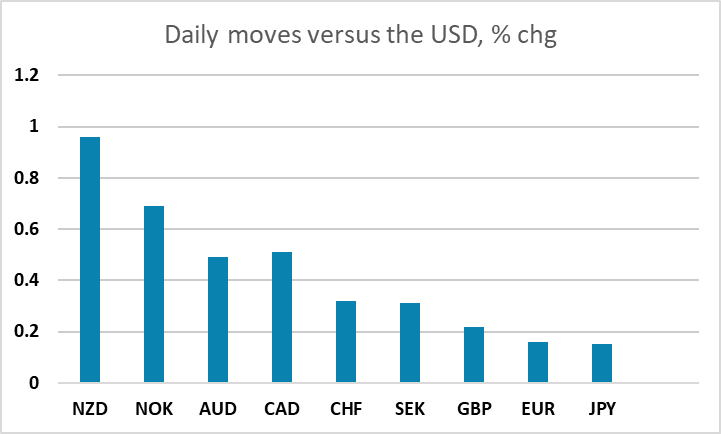

Kiwi remains the stand out, short squeezing further ; NOK and CAD gain some oil support

Focus turns to US CPI, given extra emphasis by Fed Waller comments

European morning session

As the market increasingly resigns itself to the risks that abnormal Strait scenarios become messier and more entrenched after recent comments and events, oil has marked higher, Brent making it to the $86s, up another $3. There is also increasing focus on much greater pressure on refined.

In FX, this is still largely proving self-neutralising to a degree, in places, with EUR/USD still sat around 1.14, where more options sit again into US CPI. Both ECB and Fed have moved back to pricing in 2 hikes by turn of the year. The market is also already somewhat long dollar against most pairs.

NZD has been the main independent mover for a few sessions now. The short squeeze extends further with NZD/USD up around 1% now on the day, following the overnight comments that added further fuel.

Otherwise, the likes of NOK and CAD are seeing a degree of support from the oil lift.

Asia Session

RBNZ chief economist Conway reaffirmed last week 25bp hike to 2.5% and said the bank will respond further if Middle East linked inflation pressures prove persistent. While it is a similar rhetoric from the meeting summary, the reinforcement is keeping Kiwi bidders hopeful of more hike to come in the next meeting. NZD/USD is trading 0.71% higher at 0.5791. AUD/USD is also trading 0.21% higher while USD/CAD slips 0.18% with oil up almost two dollar/b.

The U.S.-Iran escalation persists and seems to see little easy solution soon. The initial optimism from continued negotiation fades quickly with more U.S. military operation. Major equity indexes are performing individually. USD/JPY is trading 0.08% lower at 162.30. Else, EUR/USD is down 0.11% and GBP/USD is down 0.14%.