Europe Summary and Highlights 24 Jun

Dollar stretches, remains firm, if now taking a breather around some levels

IFO data broadly as expected

European morning session

No data of impact over the morning. German IFO data overall as expected at 85.6 from 84.9, with current 87 from 86.1 (mkt 86.3) and expectations 84.1 from 83.8 (mkt 85.1).

EUR/USD has made it to 1.1350, round figure and just a few ticks through the 38.2% retracement, taking a breather there.

Mixed equity action - Kospi bounce, Nikkei sill down overnight, Nasdaq future around + ½ . Micron earnings are due later today as one watch point.

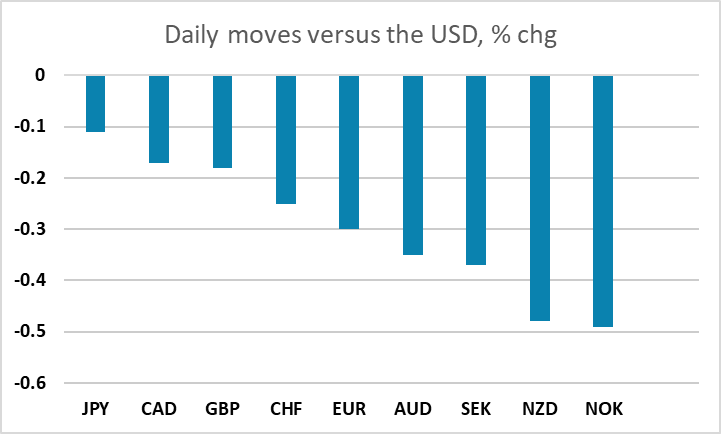

Dollar generally pressing and stretching at the highs across the board, especially NOK and antipodeans - net up around ¼ to ½ % across the majors on the day. USD/JPY still lagging/capping, sitting just off the highs.

Asia Session

Asia Session

Risk stays choppy with traffic began to flow in the Strait of Hormuz. The market is clearly waiting for the next cue with the initial euphoria in Middle East peace and Spacex IPO fades. Major equity indexes are performing individually. The May monthly headline CPI continues to moderate at 4% y/y. However, trimmed mean CPI, favored by RBA, beats estimate at 3.6% y/y. AUD/USD is trading 0.06% lower at 0.6912 on soft precious metal. NZD/USD is trading 0.22% lower while USD/CAD rises 0.04%. Both brent and WTI is lower for the session.

USD/JPY is consolidating at recent high around mid 161. The June BoJ summary of opinions confirmed that majority of board members are indeed hawkish. But contrary to market thinking, we believe the political obstacle will be too big for a hike every few months and see only another hike after 2027 spring wage negotiation. USD/JPY is almost unchanged at 161.58. Else, EUR/USD is down 0.11% and GBP/USD is down 0.06%.