Europe Summary and Highlights 29 May

Oil sits around the lows waiting on news

EZ data mixed. German State CPI below expectations, bolsters bunds

BoE's Bailey signals no hurry on rates

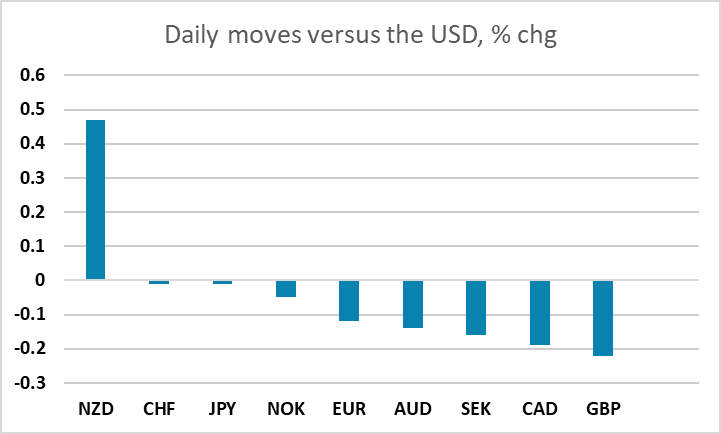

AUD/NZD still where the most life is

European morning session

Markets marking time to see if the final hurdles are cleared regarding a MoU, oil sitting at the lows (front months - ¾% to -1%). Dollar pairs largely contained, EUR/USD so far respecting the circa 1.1650ish highs and more generally sitting in the 1.16-1.165 or so range and expiry zone that has been dominating for a couple of weeks.

Kiwi remains the standout performer of the day and week, AUD/NZD - ½ % on the day and back as low as 1.1985, and NZD/USD trending back towards the range highs near 0.6~.

GBP drifting off, though mainly as EUR/GBP continues its recent chart driven range bounce action. BoE's Bailey though does come across relatively dovish with comments that suggest no hurry to raise rates: higher inflation expectations not coming through in wage settlements, allowing inflation to temporarily run above target appropriate (albeit tolerance would weaken if second round effects emerge).

Eurozone data a little mixed but overall comes in bond supportive mainly thanks to the lower than expected German state CPI, generally pointing to a deceleration of around 0.3pp on the year for the national figure later.

France Q1 GDP also revised down to -0.1% in Q1 from flat. France prelim HICPI 2.8% from 2.5%, highest since Feb24, but below mkt 2.9%.

On the flip side, Italian HICP 0.4% m/m 3.3% y/y vs 3.2% mkt and highest since Sep 2023

German unemployment also comes in better than expected at -12k vs mkt +10k with the rate down to 6.3% from 6.4%. Italy unemployment also lower than expected at 5.1% vs mkt 5.3%.

Asia Session

Tokyo May headline CPI came in at 1.4% y/y, with ex-fresh food at 1.3% and ex fresh food & energy at 1.6%. It clearly shows the inflationary pressure being artifically cushioned by extension of energy stimulus. Yet, it cannot be ignored that household consumption is also weaker despite real wage positive. USD/JPY is trading 0.04% higher at 159.29.

The risk sentiment is still undecided as Trump hasn't signed the ceasefire deal yet. It looks like background negotiations are still going through wordings of a nuclear deal while in the front we heard more bombings. U.S. major equity indexes are more cautious than regional counterpart while precious metals are performing individually. AUD/USD is trading 0.03% higher at 0.7165. NZD/USD is trading 0.39% higher on Governor Breman's hawkish rhetoric following the RBNZ's hold earlier in the week. Else, USD/CAD is up 0.03%, EUR/USD is down 0.08% and GBP/USD is down 0.04%.