Europe Summary and Highlights 29 Jun

Slow morning, consolidation with minor dollar drift

European morning session

A slow morning, the dollar still a little dragged by the hangover of overbought conditions but still held by recent capping. Options this week and wait for major events like payrolls may also tend to reinforce the stall. EUR/USD for instance around the 1.14 figure.

EZ M3 3.2% from 2.7% vs market 2.7%. Loans to household 3.1% from 3%, non-financials 4% from 3.4%. Spain HICP unchanged at 3.6%y/y vs market 3.4%. EZ economic sentiment 95.0 from 93.7 vs 94.3 expected.

UK BoE consumer credit 1.66bn vs market 1.8bn, mortgage lending 2.89bn vs market 4.55bn, and approvals 56.2k vs market 62.9k.

Equities a little firmer, Nasdaq future +1%, while oil is calm, up around $0.6-0.8

Asia Session

The brief crossfire in Middle East has limited impact for the global market on Monday. Minor gaps are closed for major currency pair. USD/JPY is hovering at recent high while short end yields underperform longer end. USD/JPY is currently trading 0.06% higher at 161.79.

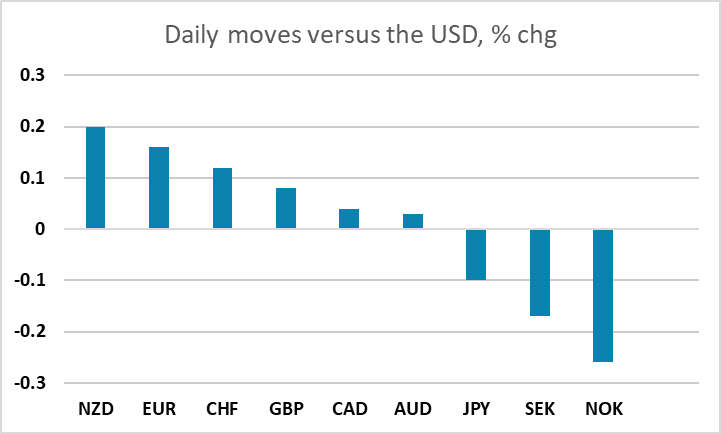

Major equities are performing individually on Monday even Middle East tension eases. U.S. equities are leading the pack while Japanese equities lag. It is clear that market participants are cautiously optimistic about the Middle East situation. AUD/USD is trading 0.04% lower as precious metal are also falling. NZD/USD is trading 0.17% higher while USD/CAD slips 0.05% with both Brent and WTI filling gap. Else, EUR/USD and GBP/USD are up 0.08%.