Europe Summary and Highlights 1 Jul

EZ HICP confirmed lower than mkt expectations, EUR/USD slips off 1.14

Focus turning to ongoing payrolls build up

European morning session

EZ June HICP comes in at 2.8%y/y from 3.2%y/y, well below the original consensus of 3.0%, if less surprising after weak national figures yesterday. Ex energy was down to 2.2%, while services was down to 3.2% from 3.5%.

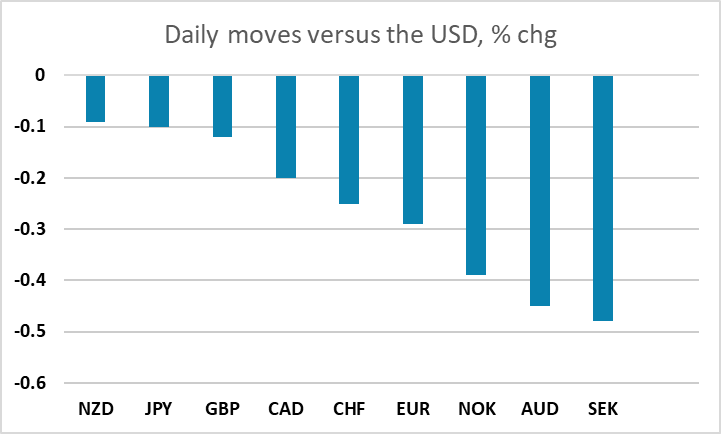

EUR/USD eases off from 1.14~ to 1.1385. Dollar generally remains well supported even as it unwinds the overbought conditions of the last few weeks. Next major focus remains payrolls, with ADP and ISM continuing the build up to that in the US session.

Final EZ manufacturing PMI revised marginally to 51.4 from 51.3. UK revised to 52.5 from 53.1 and is still being artificially boosted in the breakdown by supply issues.

Metals generally on the soft side, AUD/USD finding it hard to sustain any attempted lift back above 0.69.

Asia Session

Another day another high for USD/JPY as the pair marches towards the next figure at 163. We haven't heard much from the Japanese side but such rally has assumed a rapid pace, potentially triggering an intervention if there is more follow through in the week. USD/JPY is trading 0.16% higher at 162.78 with JGB yields higher across the curve.

The broader market is undecided with Middle East concern resurfaced. The U.S. seems to be applying maximum pressure tactics again while Iran continues to play hardball. While it is beneficial for both side to reach a final agreement, no market participants would like to be caught wrongfooted. Major equity indexes are performing individually. AUD/USD is trading 0.39% lower at 0.6892 as precious metal stay depressed. NZD/USD is trading 0.03% lower while USD/CAD rises 0.12% with Brent and WTI performing individually. Else, EUR/USD is down 0.11% and GBP/USD is down 0.15%.