This week's five highlights

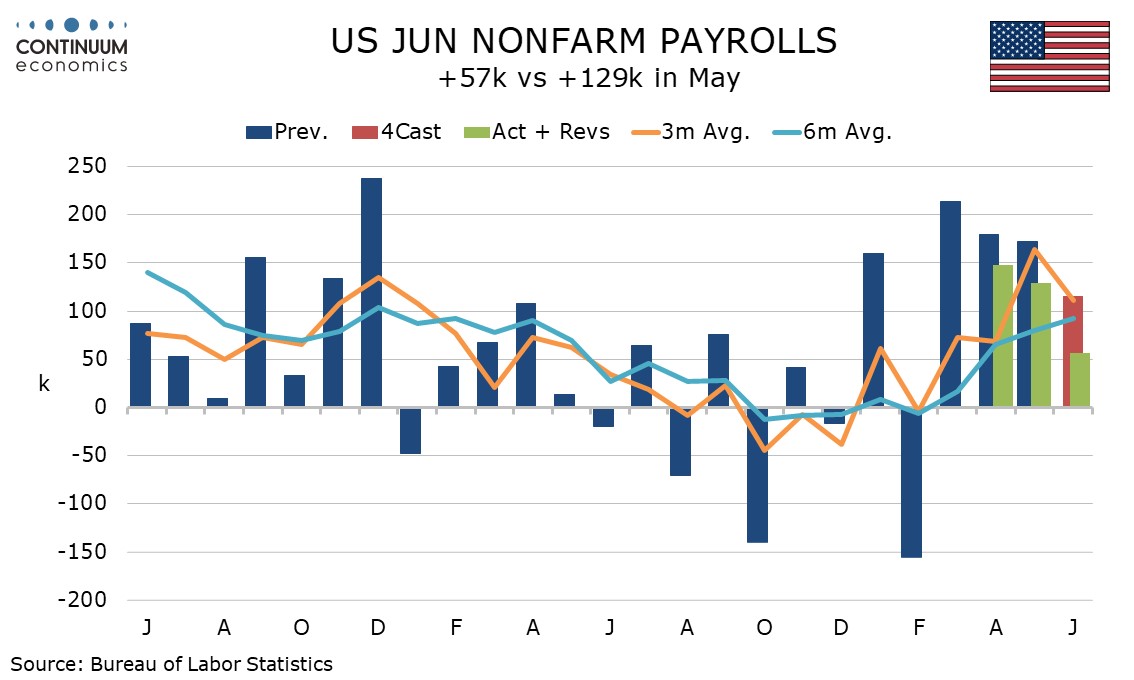

U.S. June NFP Misses

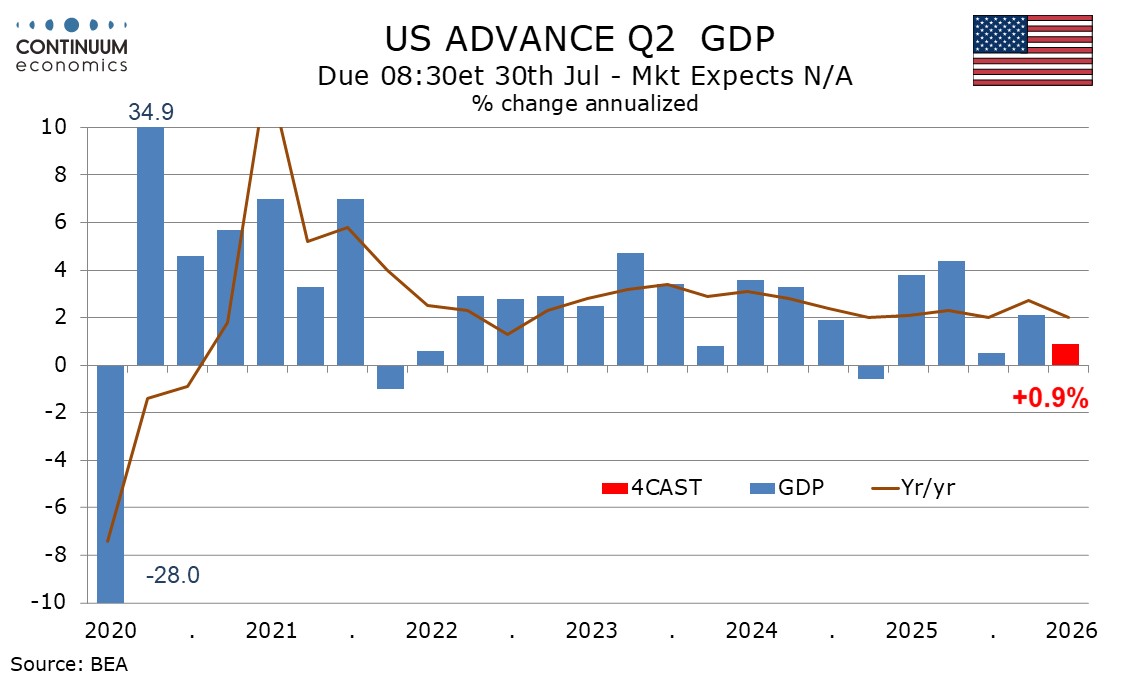

A Strong U.S. Q2 Report Now Looks Unlikely

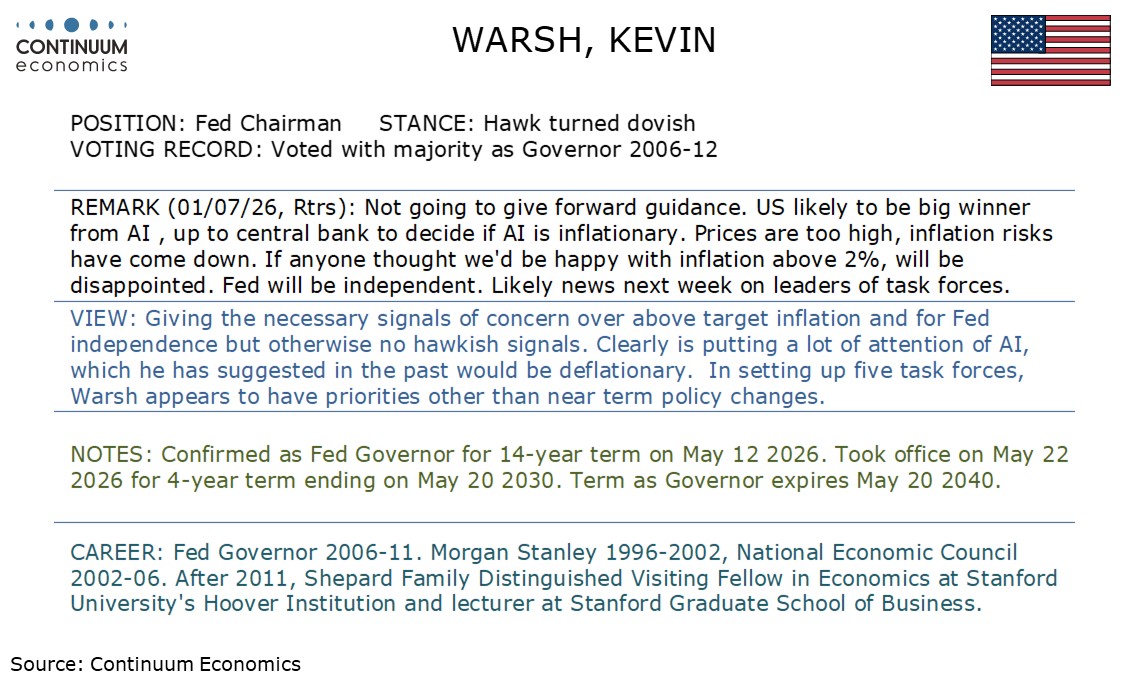

This Week's Fed Speaker

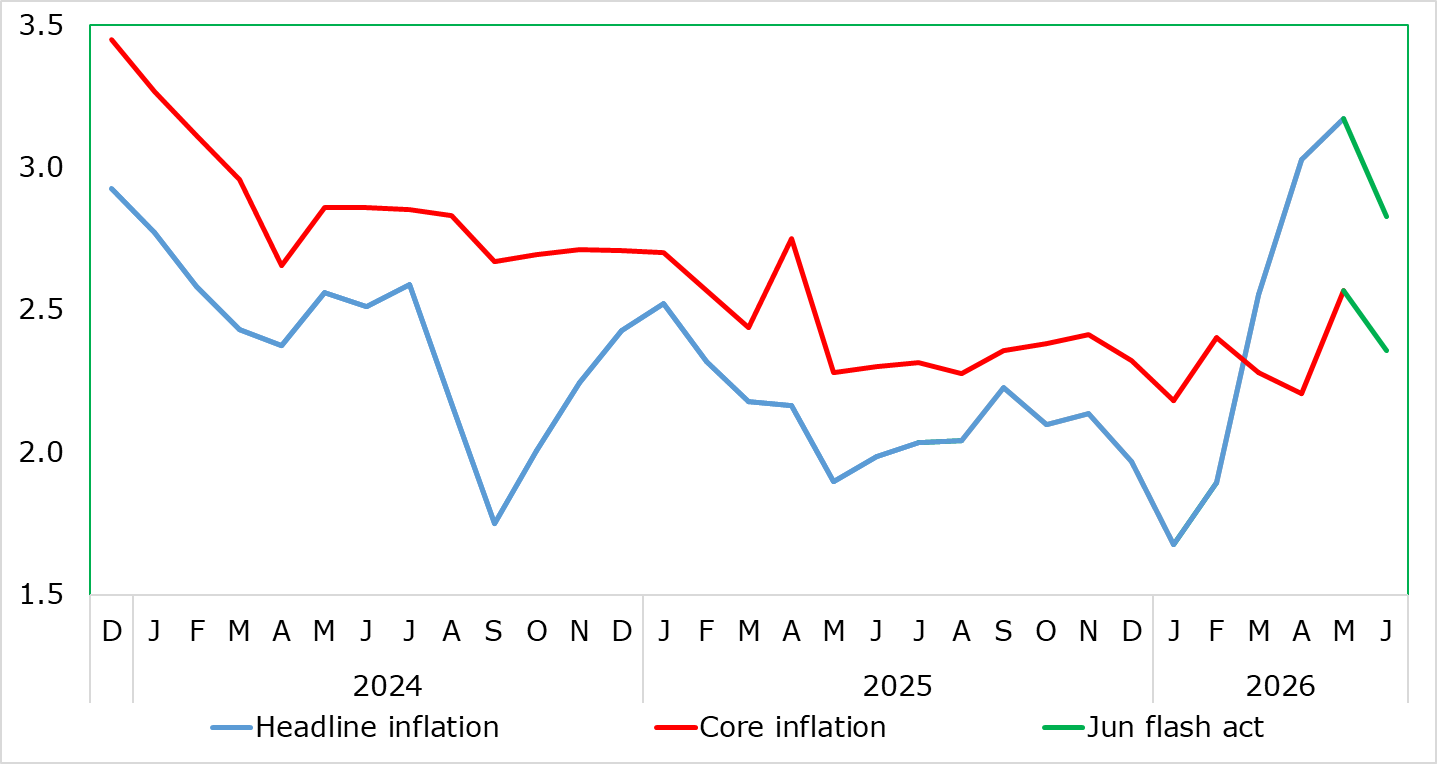

EZ HICP Absence Second-Round Effects Continues

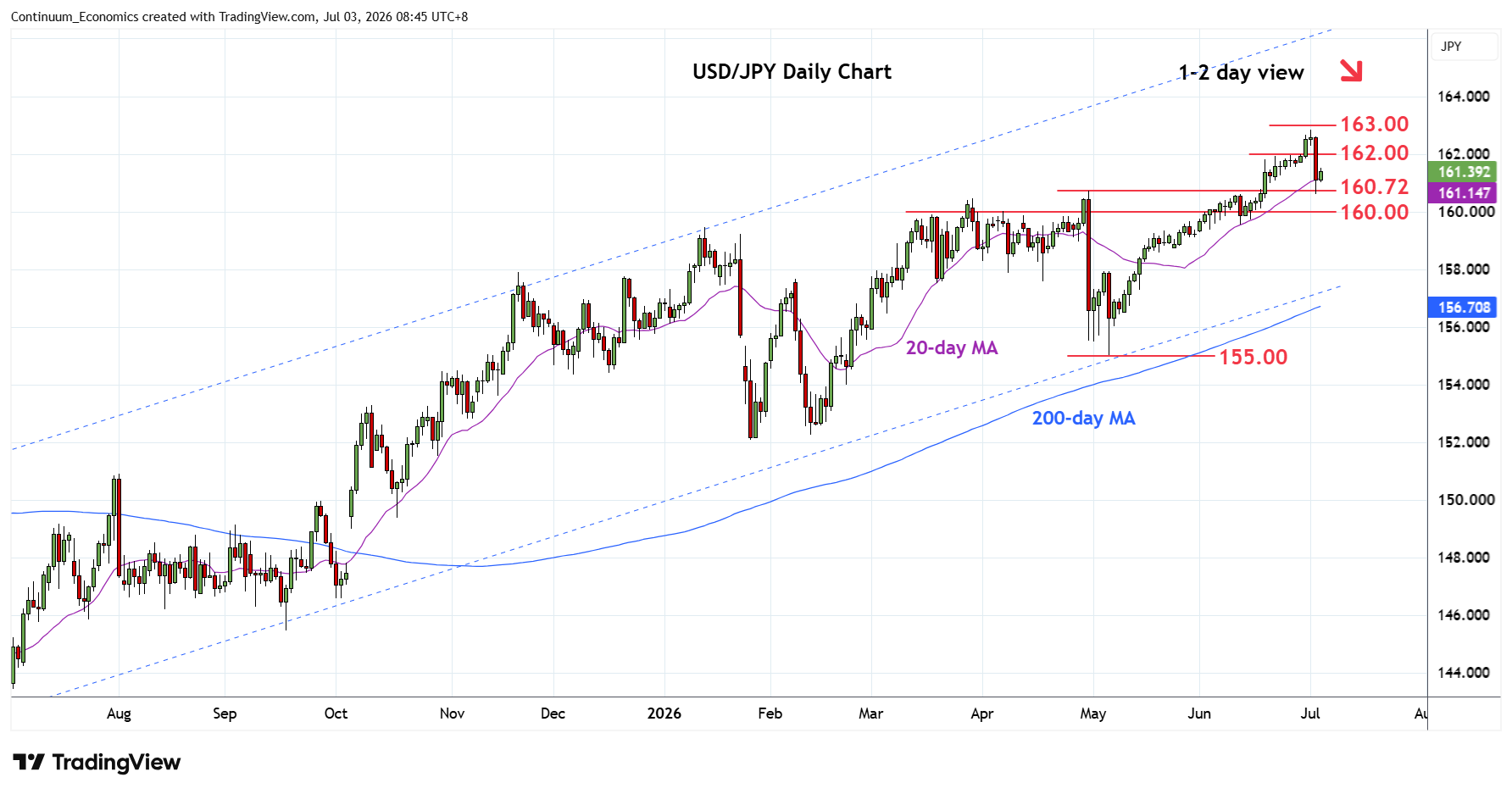

USD/JPY Corrects

June’s non-farm payroll is weaker than expected with a 57k increase, 49k private, with downward revisions to April and May. The slowing is consistent with an upturn in the initial and continued claims trends, though both were almost unchanged (-1k to 215k and +2k to 1.814m respectively) in the latest weekly release. Unemployment did slip to 4.2% from 3.3%, but this was on a fall in the labor force. Average hourly earnings were in line with expectations, up by 0.3%.

May’s payroll was revised lower to 129k from 172k with April revised to 148k from 179k, a net downward revision of 74k making the overall net figure negative. For private payrolls the net downward revision was 50k, just enough to leave a marginal net negative.

After a sharp deterioration in May’s trade deficit, previously positive forecasts for Q2 GDP need to be trimmed significantly, though there is still uncertainty over June data. We now expect a Q2 GDP increase of only 0.9%, down from a previous estimate of 2.3%. After an upward revision to Q1 our view for 2026 as a whole is not significantly changed, though the second half of the year may now look similar to the first rather than slowing from a stronger Q2.

Domestic demand is still likely to look strong in Q2, with a rise of 3.1% in final sales to domestic buyers (GDP less inventories and net exports), which would be the strongest increase since Q3 2025.

Figure: Headline HICP Plunges And Core Eases Modestly Too?

Contrary to some thinking, EZ HICP inflation continues to behave, both absolutely and relatively – ie to what looks ever excessive ECB price thinking. The question must be if and when the ECB chooses to note friendlier price and costs signals, rather than pander to the upside prices risks that only some (and may be fewer) pieces of data have been flagging. Regardless, the ECB cannot disregard the June HICP flash (Wed), which dropped markedly and with no sign of second-round effects, thereby suggesting that headline inflation has not only already passed its peak and maybe clearly so but should fall further even in the near-term and widely so. These data may have a material impact on ECB thinking, especially as the data arrive toward the end of this week’s key ECB monetary annual gathering in Sintra.

USD/JPY corrects on market fear for intervention. It is reported earlier in the week that the MoF and BoJ may have changed their intervention strategy to "silent intervention", where they stop jawboning before an actual intervention in the FX market. It clearly kept market participants being more suspicious in abnormal move and led to a quick drop of a figure on the same day being reported.

On the chart, consolidation below the 162.84 high gave way to sharp losses through the 161.00 level before finding support at 160.72 April high. Bounce here see prices settling into consolidation above the 161.00 level and unwinding oversold intraday studies. However, bearish pullback from the 162.84 high keep pressure on the downside and see scope for extension lower to retrace strong gains from the 155.00 May low. Lower will see room to support at the 160.00/159.50 area. Meanwhile, resistance is at the 162.00 congestion which is expected to cap and keep pressure on the downside.