This week's five highlights

The Strait of Hormuz Question

ECB Insurance Hike

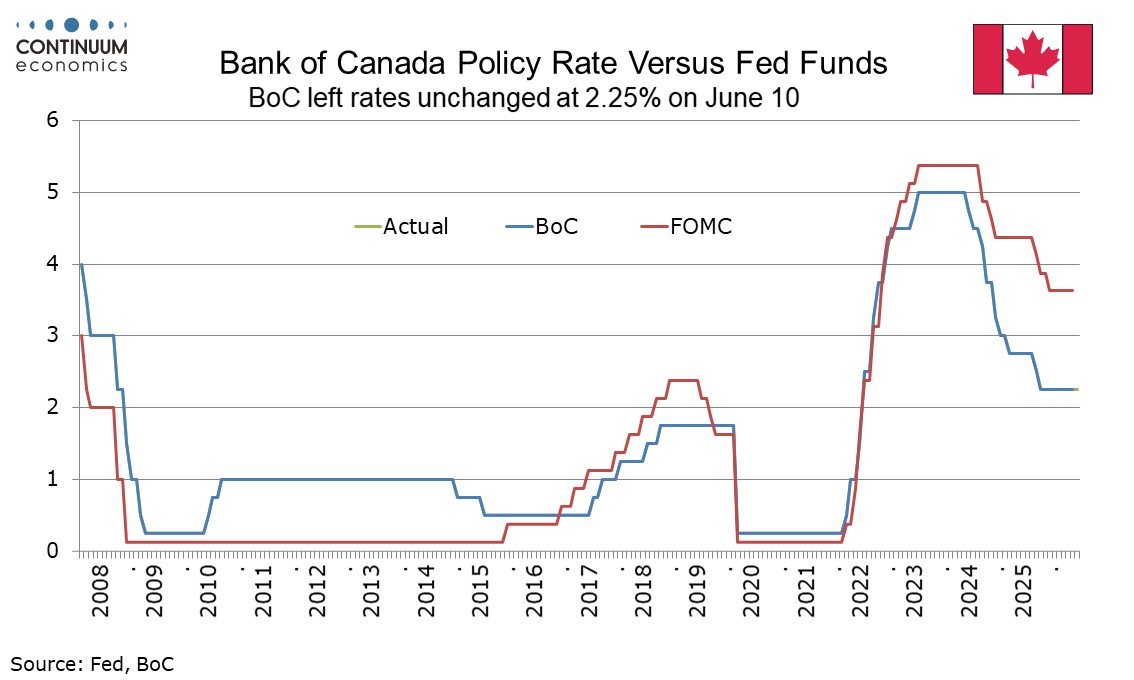

Bank of Canada On hold with balanced tone

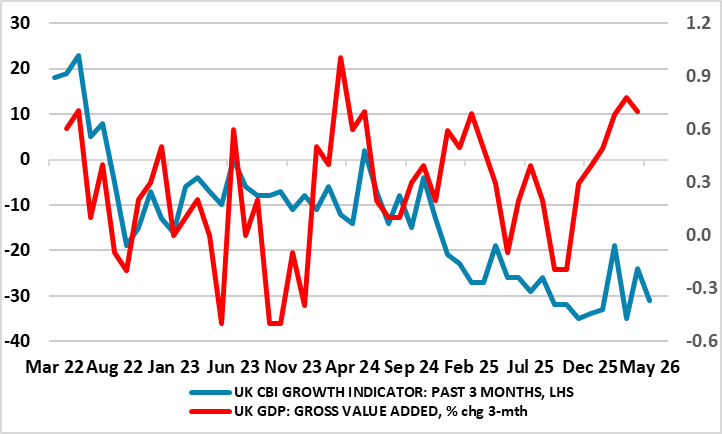

UK GDP Upside Surprises Persist

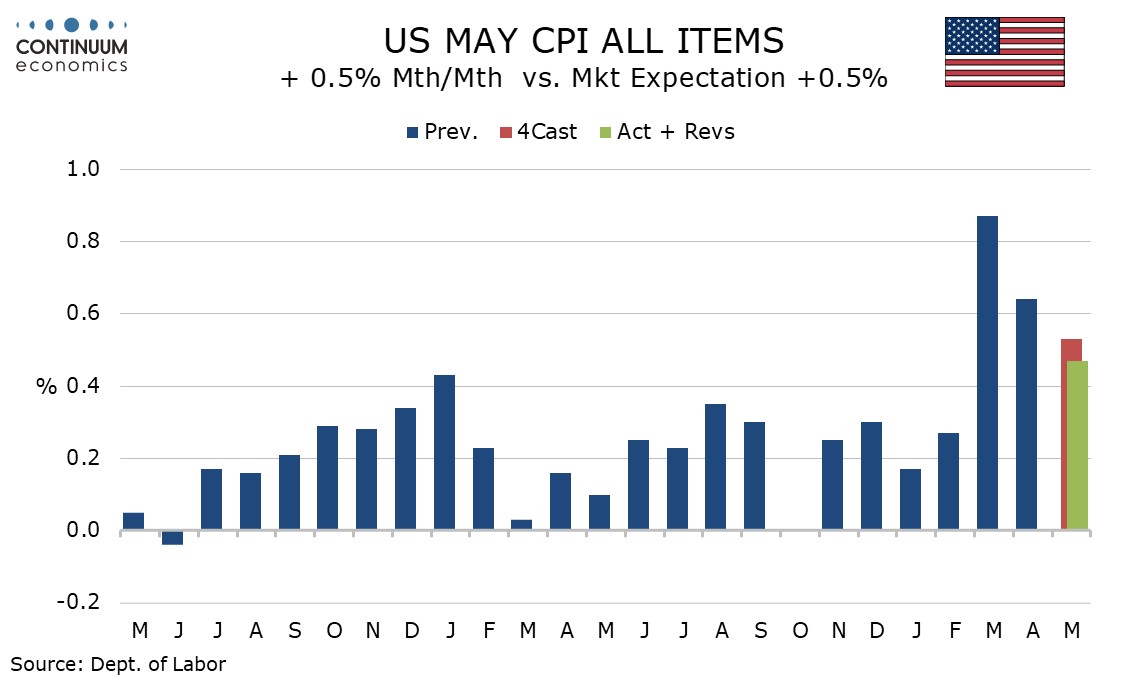

U.S. May CPI Shows Surprising fall in transport services

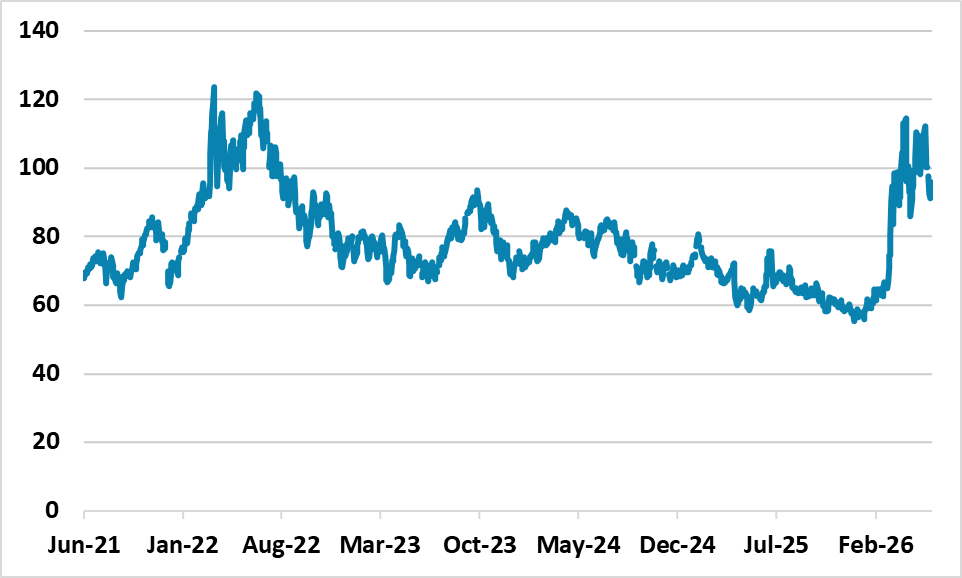

Figure 1: WTI Oil Prices (USD)

Though the U.S. and Iran have attacked each other June 10, talks to reopen the straits of Hormoz still continue and looks hopeful to reach a deal soon. An Iran/U.S. agreement to reopen the Straits of Hormuz could cure the risk of a demand/supply oil market imbalance and produce some psychological relief that could knock USD10 off oil prices but still leaving them at USD85 for WTO by end 2026. If this is not delivered by late summer/early autumn then oil prices could spike to USD120-150 by upset financial markets.

Financial markets remain divergent, with equities focused on the AI and wider corporate earnings story (with intermittent profit-taking), but bond markets apprehensive of 2nd round effects from existing energy prices and the risk of DM rate hikes. Financial markets relative calm reflects central bank communications that they do not need to overreact to higher energy prices. Of the major DM central banks, the ECB will kick off with a widely expected 25bps hike (here). However, the forward guidance will likely be that this could be followed by a further hike, but that the situation differs from 2022 when domestic demand was more buoyant/labor market tighter. The BOE, on June 18, will likely still signal risks of higher policy rates, but not guaranteed for July. The BOJ hike will be normalisation on June 16, but the BOJ is unlikely to accelerate the pace of normalisation. The Fed is expected to remain on hold, but the key will be the communication, with some Fed officials likely to highlight the risk of hikes but new Fed chair Warsh likely to maintain the status quo. A hawkish hold could spook the U.S. Treasury market.

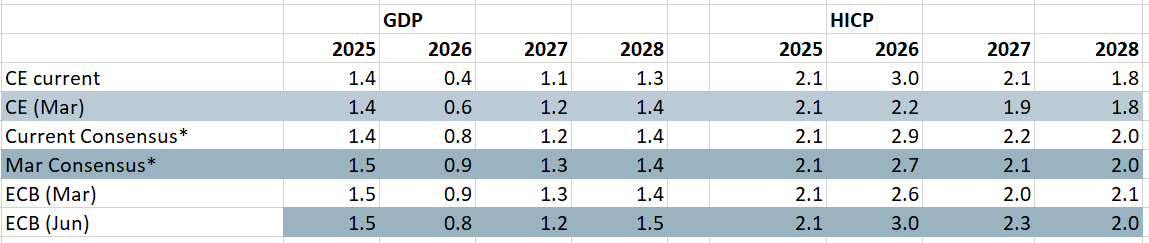

Figure: Economic Outlook from Various Perspectives

The 25 bp official rate hike unveiled today was so well-flagged it is hard to suggest that it is consistent with a decision process on a meeting-by-meeting basis. Similarly, the dominance of inflation upside risks, alongside another dose of optimistic real economy projections, is hardly proper data-dependency. All of which shows where the ECB focus lies (a sharp contrast perhaps to the BoE). But while the projections show HICP inflation back in line with target by Q4 next year, this though largely validates the market view of around three 25 bp hikes that the outlook is based on. But the projections show hardly any further damage to the GDP picture, with the ECB understating the combination of tight(er) financial conditions, banking sector reservations and ill sentiment that should combine to pull HICP inflation back to, if not below, 2% by mid-2027 and thus create both rationale and room for fresh policy easing. While a further hike cannot be ruled out given the ECB’s biased reaction function, we think that this 25 bp hike is more than enough and that this misplaced move will be more than reversed into 2027 (ie thinking largely siding with the OECD).

While recognizing that oil is around $10 per barrel higher than was assumed in its April Monetary Policy Report, the Bank of Canada left rates unchanged at 2.25% with a balanced tone to the statement. As long as core inflation does not start showing feed through from energy the BoC looks likely to avoid tightening until excess supply in the economy is reduced. We do not expect tightening until 2027.

After April’s meeting Governor Tiff Macklem stated that if the economy evolved in line with expectations policy close to current settings would be appropriate, but noted that policy might have to be nimble, noting the risk of consecutive tightenings on persistent inflation and easing if the US imposed significant new tariffs. While energy prices are now stronger than anticipated in April, Q1 GDP was weaker than expected at -0.1% annualized, which the BoC attributed to an unexpected decline in government spending, while April CPI at 2.8% was on the soft side of an April projection of about 3.0%. On inflation the BoC added that there has been little evidence of a broad based pass through of energy prices, with core CPI falling to around the 2% target and the share of components above 3.0% close to the historical average. CPI is now expected to hover around 3% in the near term before easing gradually to around the 2% target. On GDP the BoC expects growth to resume in Q2 but excess supply to persist. A strong May employment report was downplayed, with employment volatile and little changed since the start of the year. Senior Deputy Governor Carolyn Rogers stated that risks to the economy were about the same as where they were in April.

Figure: GDP Growth Hardly Strong and With Surveys Suggesting Increasing Downside Risks Ahead?

Perhaps it is a supreme irony that just as business surveys suggest clear weakness, if not fresh contraction, the actual real economy has surprised on the upside, even now into the second month after the Middle East conflict started. Indeed, and in perspective, official GDP data suggest that since Labour took office in July 2024, the economy has grown a cumulative 2%-plus, ie over 1% per year. And providing yet more apparent signs of such economic resilience and, once again exceeding expectations, GDP grew by 0.3% m/m in March 2026, following growth of 0.4% in February and only fell back 0.1% in April. We think this is more an aberration than a better trend and partly a result of poor seasonal adjustments, meaning that we see May GDP falling back further, this chiming with both weak(er) business survey activity (Figure 1) and employment signals and where what growth may actually have occurred likely to be short-lived boost in inventory building. But the data implies a much better productivity backdrop.

May CPI is in line with expectations at 0.5% overall but the core rate ex food and energy was softer than expected at 0.2%, with the rise before rousing being 0.208%. The most surprising restraint on the data was a 0.6% fall in transportation services, despite continued gains in air fares. Air fares rose by 2.7%, similar to their gains seen in March and April, but this was outweighed by a 1.7% fall in motor vehicle insurance, which has over twice the weighting of air fares. Public transportation rose by only 0.3% despite the rise in air fares, with declines seen in ship fares and intracity transportation.

Services less energy rose by 0.3%. Strength was seen in education and communication at 0.9% led by postage and delivery services which may be a pass on of transport costs, while miscellaneous personal services were strong at 2.1% led by tax preparation and other accounting fees, which does not appear related to energy. Medical care services rose by 0.5% after two straight flat months.