This week's five highlights

Iran/U.S. Escalating to Deescalate

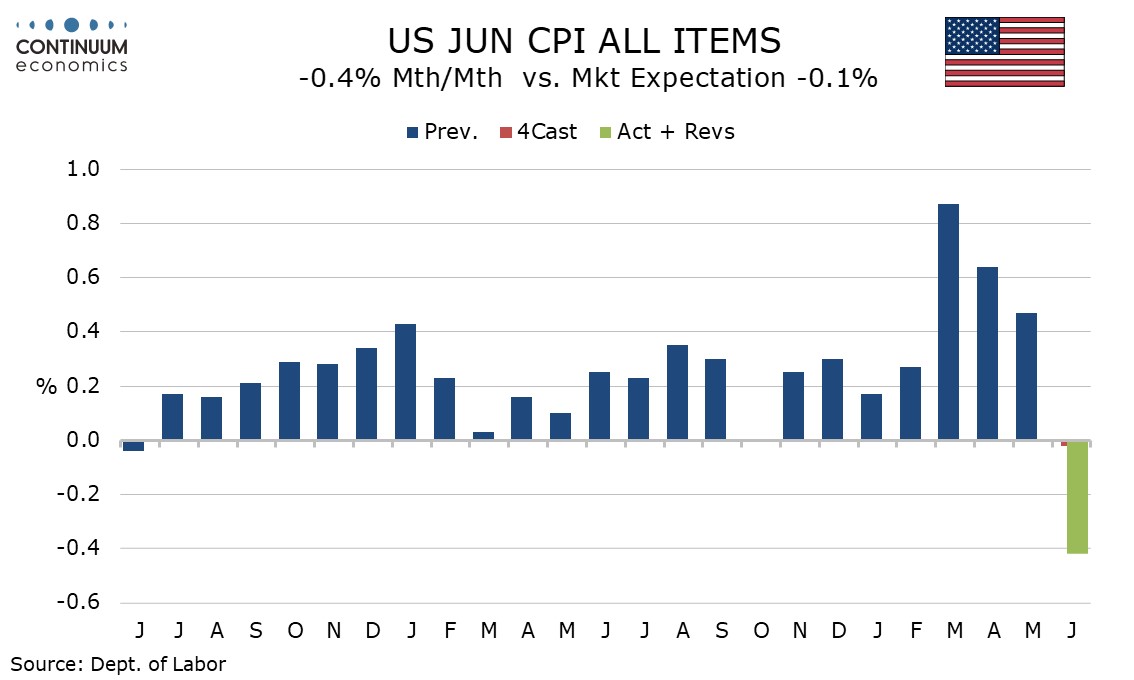

U.S. June CPI a clear relief for the Fed

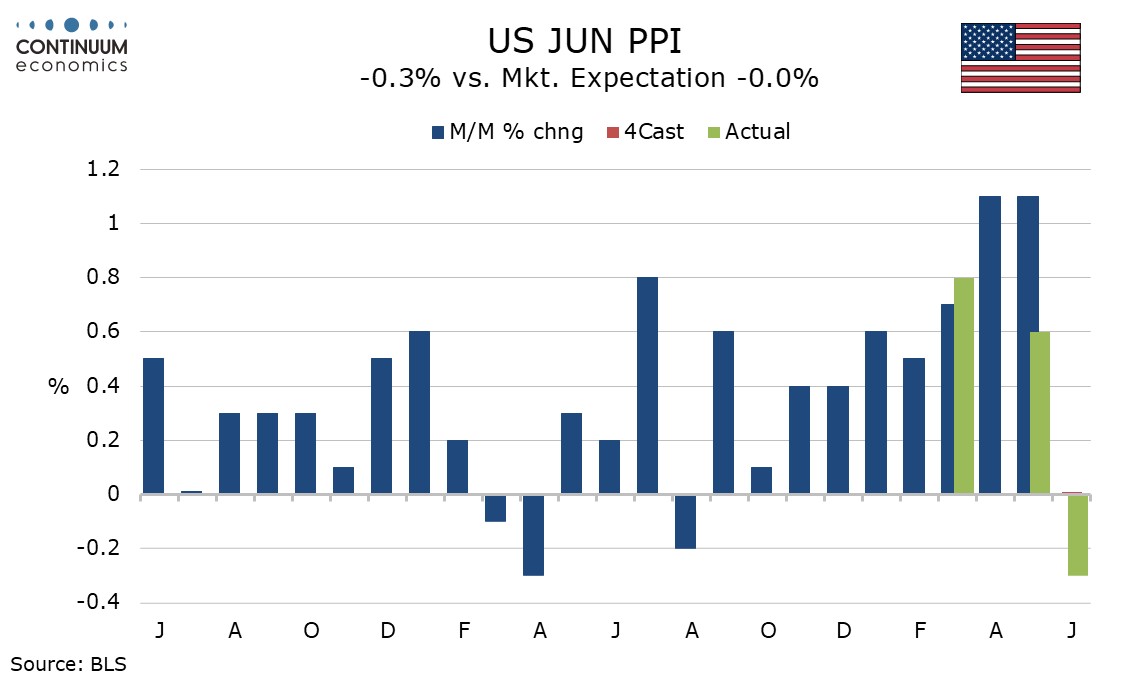

U.S. June PPI Lower than expected with May revised down

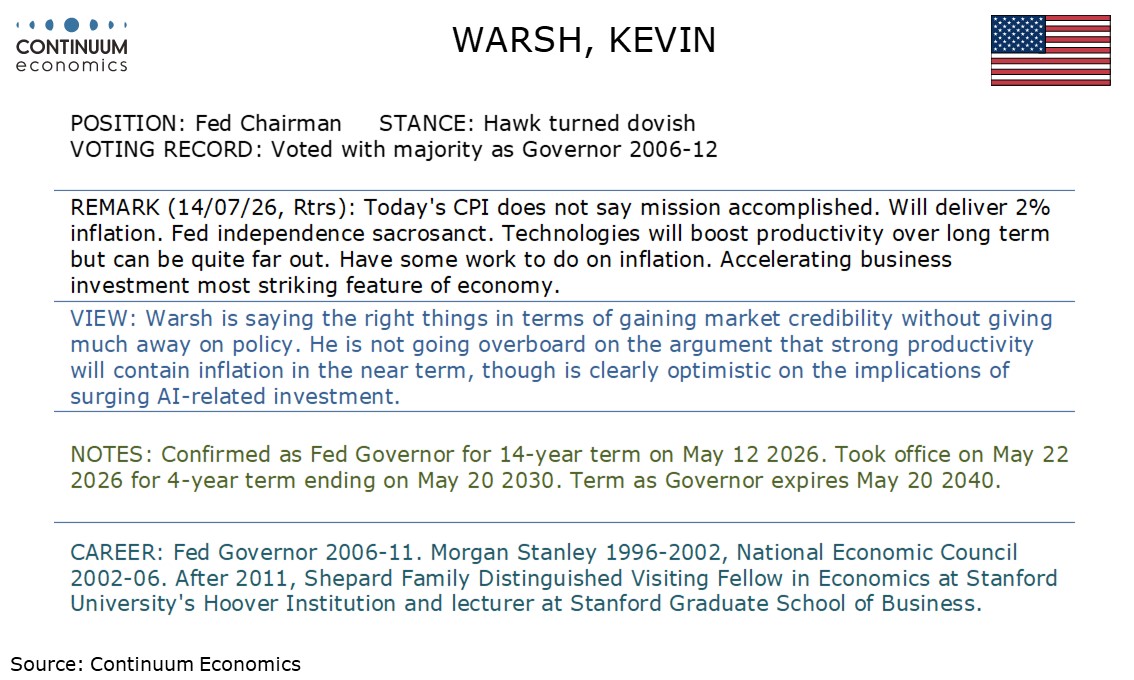

This Week's Fed Speakers

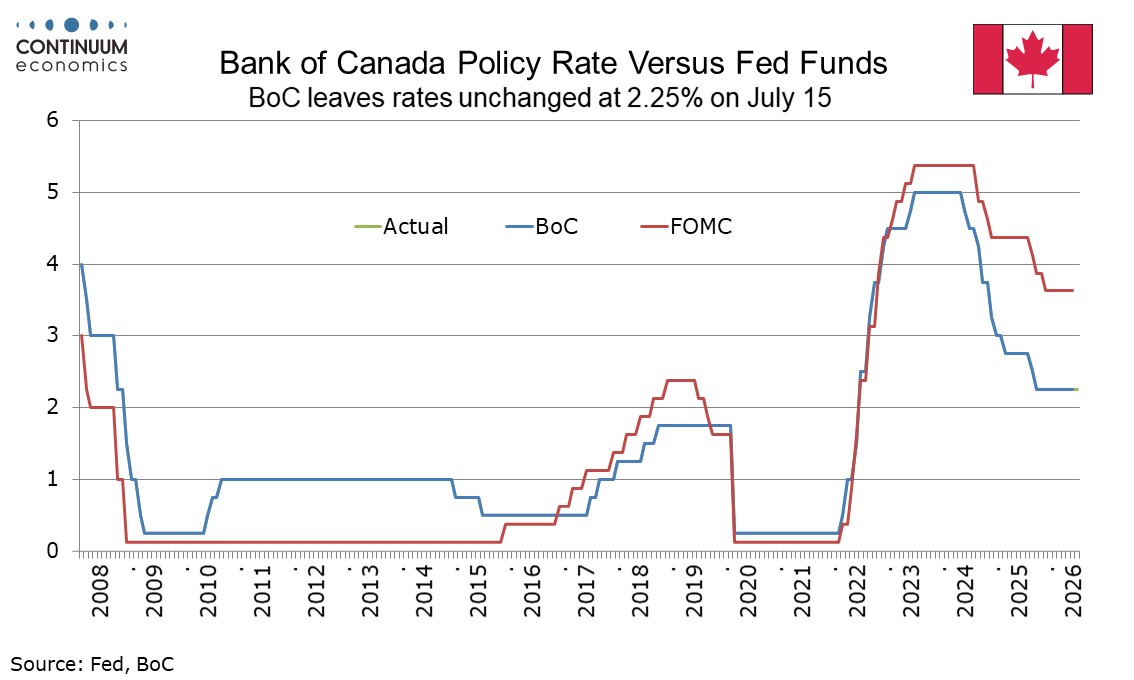

Bank of Canada Near term policy change looks less likely

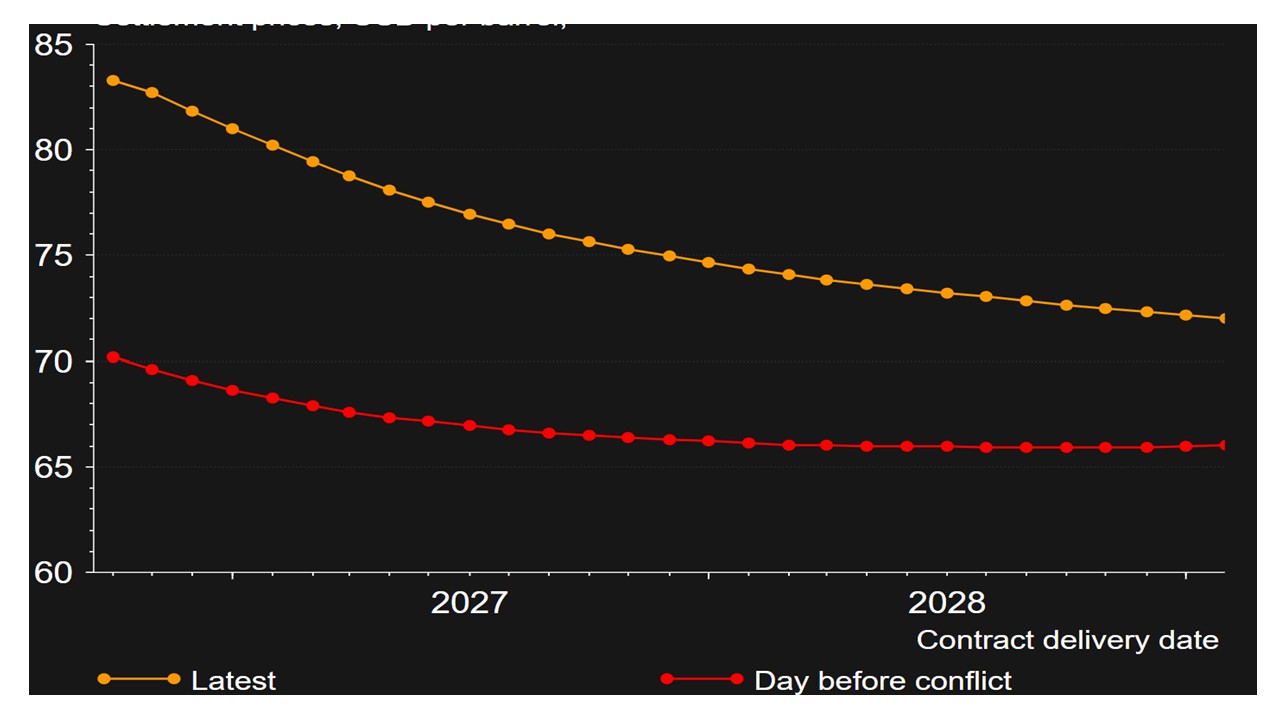

Figure: Brent Futures Curve Start of Conflict versus July 14 (USD)

Our baseline remains that the MOU will hold and that the Straits of Hormuz will reopen. Iran can be pressured economically by the U.S. naval blockade being re-established. Additionally, President Trump loves to escalate to de-escalate to get a deal, while the Republicans are under pressure before the mid-term elections for the Iran war worsening cost of living problems – gasoline could be heading back above USD4, with the latest bounce in oil prices. It is also noticeable so far that Iran attacks in the region have been focused on U.S. military bases and have not extended to hitting energy infrastructure. We still attach a 60% probability to the Straits of Hormuz reopening again, though this is unlikely to get back to pre-war shipping movements until the 60 day deal is extended and made semi-permanent. In Figure 2, we assume only partial reopening of the Straits of Hormuz, plus some temporary inventory rebuild, to keep oil prices elevated through end 2026.

Our alternative scenario (40% probability) is that the closure of the Strait of Hormuz extends beyond a couple of days and/or reoccurs in the coming months. Iran leadership appears split over the MOU with the U.S., with hardliners wanting to ensure that a southern route around Oman is not established and this was the cause of the recent escalation. Additionally, the fog of war could mean a military escalation. In the 1987-88 tanker wars, Iran hit a U.S. warship and prompted the U.S. to escalate by hitting Iran including oil fields.

June CPI is significantly softer than expected, both on the -0.4% headline and an unchanged outcome ex food and energy, with the respective figures before rounding being -0.422% and -0.017%. While there are a number of volatile declines in the breakdown and recent events in the Middle East present renewed upside risks to energy, the data argues against a rate hike at the July 29 FOMC meeting.

Energy fell by 5.7% in a partial reversal of there straight strong gains with gasoline down by 9.7%. Energy services also declined, by 0.7%, led by a 1.0% fall in electricity. Food saw only a modest increase of 0.2%. Commodities ex energy fell by 0.1% for a second straight month with a notable negative from tariff-sensitive apparel at -0.6%, its first decline since November and sharpest decline since January 2025. New vehicles were unchanged after two straight declines but used vehicles ell by 0.2% in a first fall in three months.

June PPI is on the low side of expectations, -0.3% overall, +0.2% ex food and energy and +0.1% ex food energy and trade. The weakness can be seen as corrective from preceding strength though a downward revision to May adds to the negative surprise. Overall May PPI now increased by 0.6% rather than 1.1% while ex food and energy has been revised down to a 0.1% increase from 0.4%. May’s ex food, energy and trade gain however is unrevised at 0.8%, and the 0.1% June ex food, energy and trade gain needs to be seen alongside that.

Energy fell by 6.4% after a rise of 8.4% in May, with gasoline down by 12.0% after a 20.9% rise in May, that was a third straight strong gain. Food also fell, by 0.6% after a 0.5% May increase, with grains falling by 12.0% after a 10.2% May increase.

The Bank of Canada left rates unchanged at 2.25% as expected and while expressing increased optimism over the Canadian economy, does not appear in any hurry to change rates. The statement did state the BoC was prepared to adjust policy as needed but explicit mentions of the possibility of moves in either direction seen after recent meetings were not repeated. We continue to expect unchanged policy through 2026.

After the April and June meetings, Governor Tiff Macklem warned over the possibility of consecutive tightenings on persistent inflation or easing should the US impose fresh tariffs. While Macklem still sees the conflict in the Middle East and the relationship with the United States as the two biggest risks the possibility of policy responses to the alternative scenarios was not stated so clearly. Oil moving off its highs reduces the upside risk somewhat, and while Trump remains unpredictable on trade policy, downside risks from tariffs appear to have been offset by a more positive assessment of the Canadian economy.