This week's five highlights

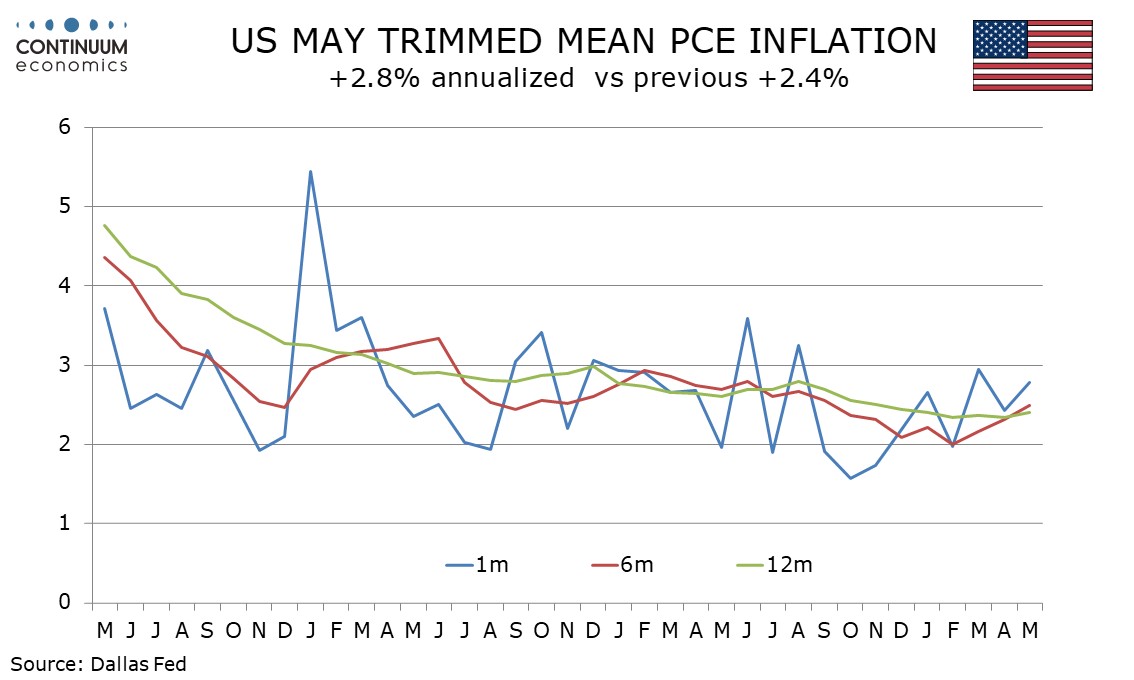

U.S. Trimmed Mean and Median PCE Price Indices not as strong as Core PCE

Other U.S. Data

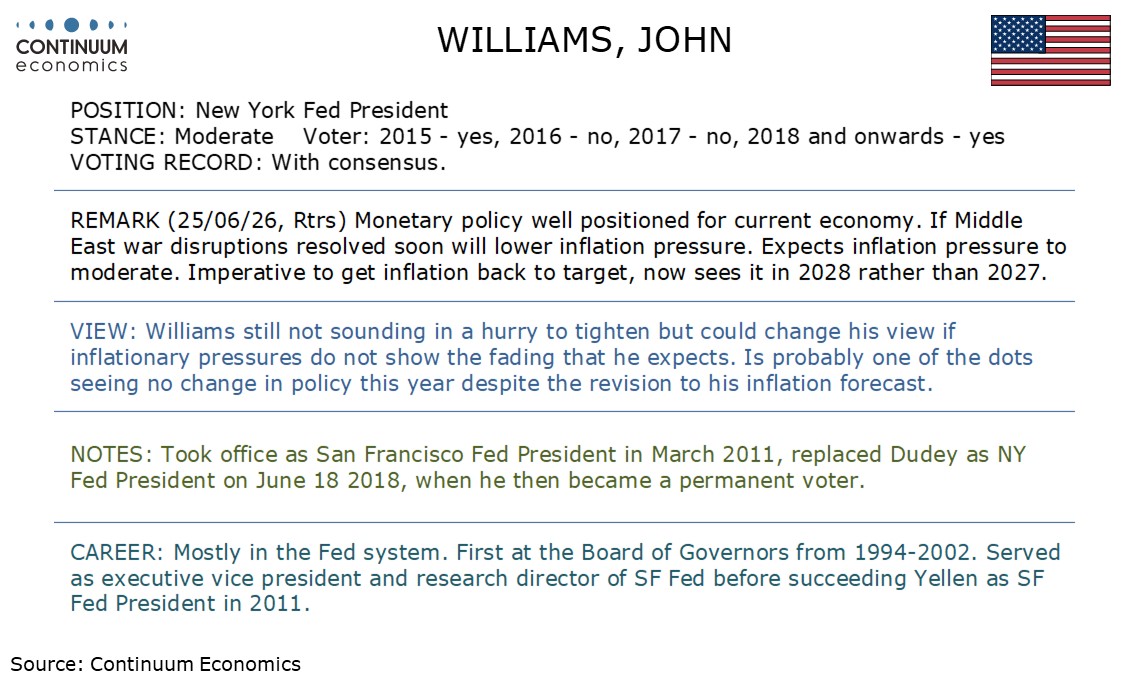

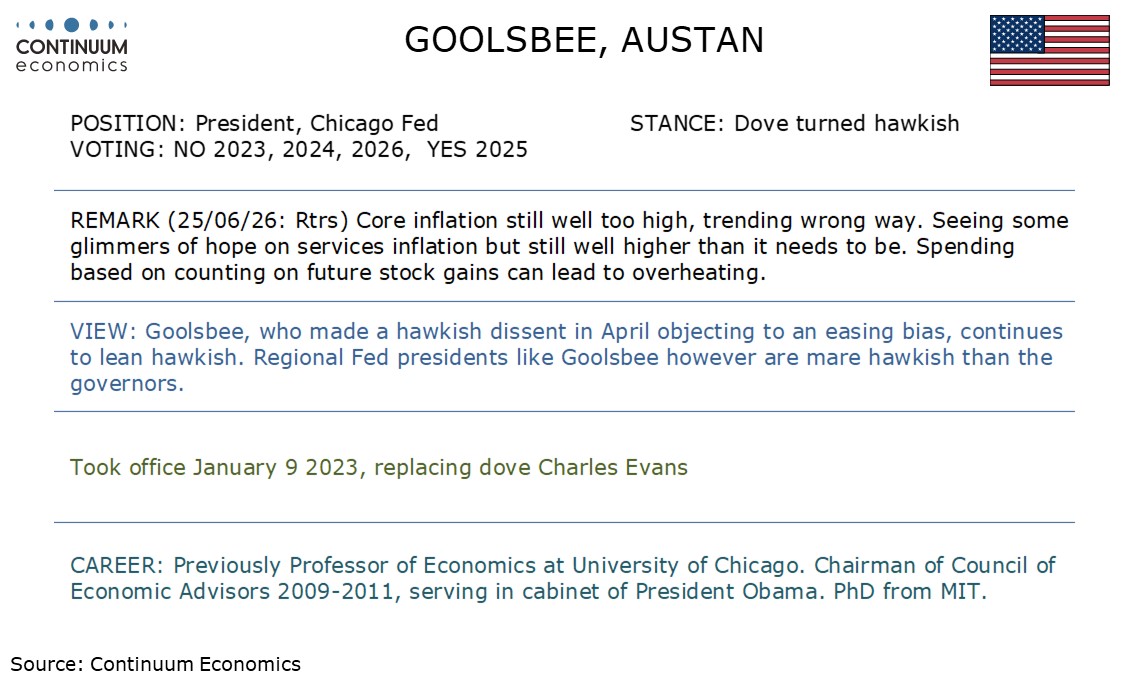

This Week's Fed Speakers

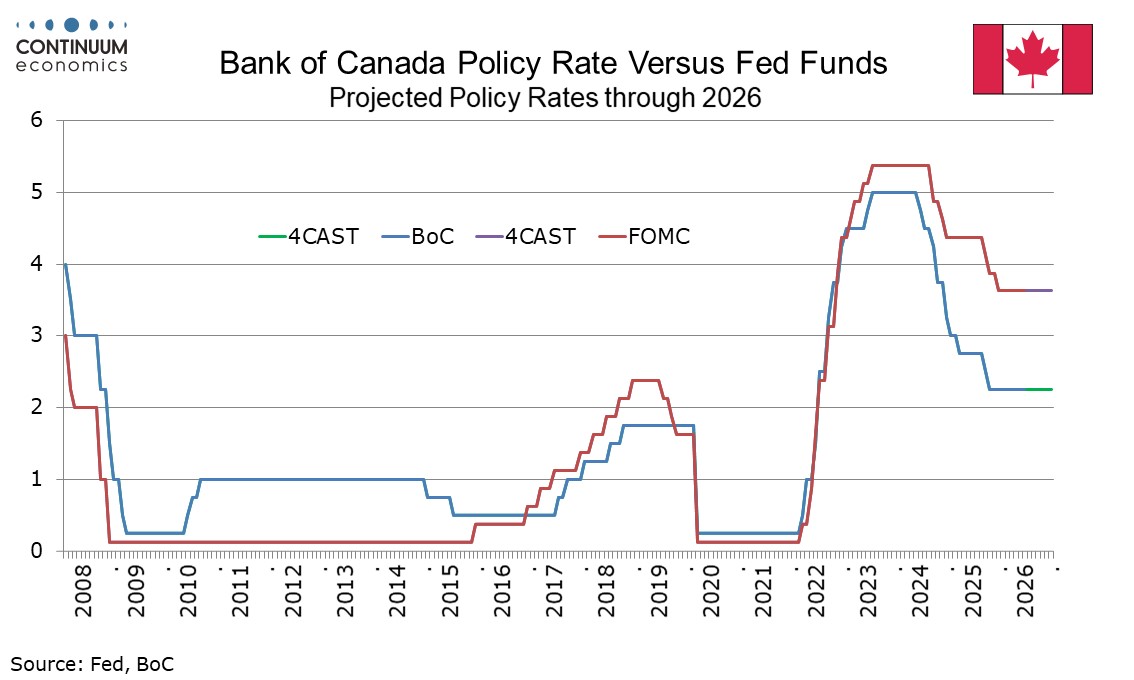

Balanced tone from Bank of Canada Minutes

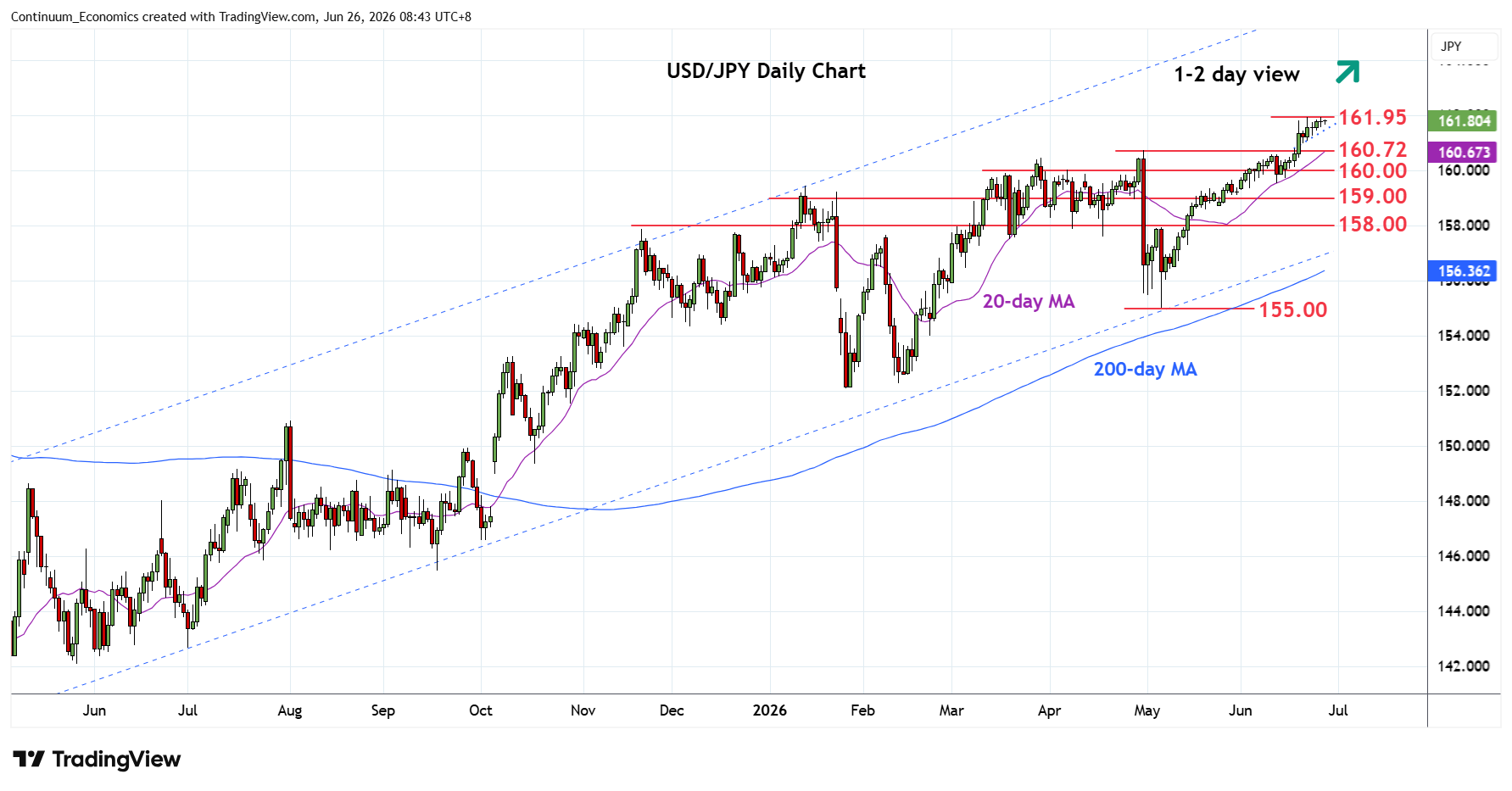

USD/JPY Slow Grind Towards 161.95 resistance

The Dallas Fed’s Trimmed Mean PCE inflation index, which is reported to be a series favored by Fed Chair Kevin Warsh, as well as the Cleveland Fed’s Median PCE price index, look a little less alarming than the Fed’s officially targeted Core PCE price index. This could be used as an argument against tightening by Warsh, though both series are stable significantly above 2.0%. The core PCE price index increased in May to 3.4% yr/yr and has been trending higher since slipping to 2.6% in April 2025. The Dallas Fed’s Trimmed Mean PCE price index is however showing only marginal signs of acceleration. Yr/yr growth at 2.41%, while up from 2.34% in April, has been running below 2.5% since December. On a one month basis the annualized gain was a little firmer at 2.78% but has not reached 3.0% since August 2025. The 6-month pace of 2.49% is at an 8-month high but the acceleration is moderate since February data touched 2.0%.

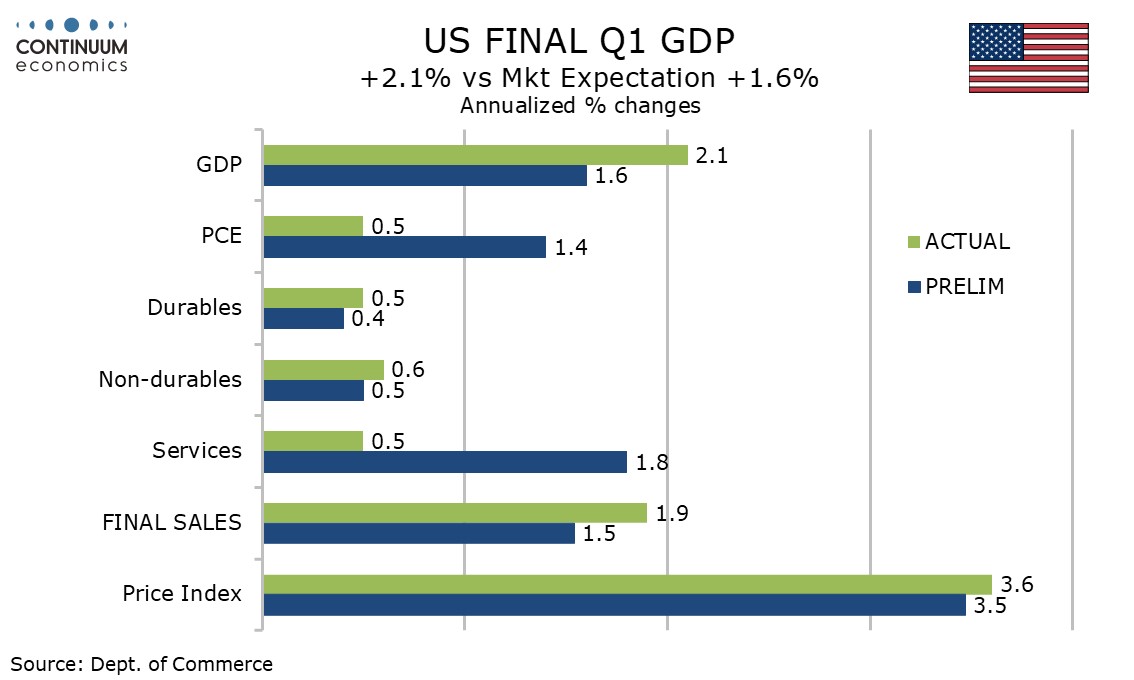

The latest US data is mostly strong, with an upward revision to Q1 GDP, stronger than expected May personal income and spending, still firm core PCE prices, lower initial claims and strength in May durable goods orders outside a fall in transport. However the Q1 GDP revision was mixed, with a significant downward revision to consumer spending. The upward revision was led by net exports. Q1 GDP was revised up to 2.1% from 1.6%, but consumer spending was revised down to 0.5% from 1.4%. The revision was fully due to services, now at 0.5% from 1.8%. Retail was revised slightly higher, durables to 0.5% from 0.4% and nondurables to 0.6% from 0.5%, but both remain subdued.

Minutes from the Bank of Canada meeting from June 10 do not provide many surprises, but confirm a fairly balanced tone that was evident after the meeting. The balanced tone does not however mean that policy will remain on hold, with high uncertainty meaning that risks could shift and the BoC agreeing it was important to reiterate the different possible paths for policy.

The BoC continued to note the risk of easing should the US impose new trade restrictions as the review of the Canada-US-Mexico trade agreement approaches, while also noting the possibility of tightening if the Middle East conflict continued and leads to ongoing generalized inflation. The risk of the latter has reduced, though not disappeared, since the meeting, suggesting markets should start turning their attention to the trade risks.

USD/JPY continues its slow grind upwards. The risk of imminent intervention fades as the pace of rally has been very slow and is not bothering the Japanese officials. The balance between BoJ and Fed is fragile with hawkish rhetoric from both sides, so as political headwinds. It is hard to see any immediate hike soon.

On the chart, the pair is pressuring the upside to tag the 161.95, July 2024 multi-year high. The resulting ascending triangle above the 161.00 level suggest potential for break to extend bullish gains from the 155.00 May low. Clearance will extend the underlying bull trend and see room towards 163.00/164.00 congestion area and high of December 1986. Meanwhile, support remains at the 161.00/160.72 area which should underpin. Would take break here to ease the upside pressure and open up room for deeper corrective pullback to support at 160.00/159.53 area.