This week's five highlights

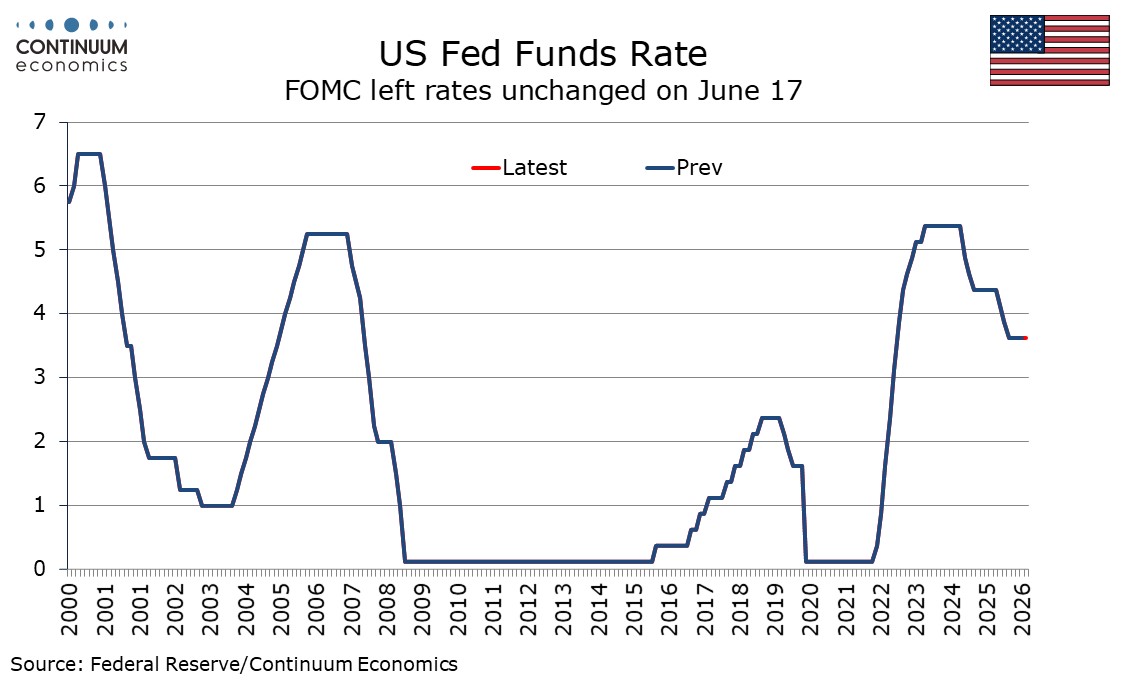

FOMC Policy may prove less hawkish than the dots

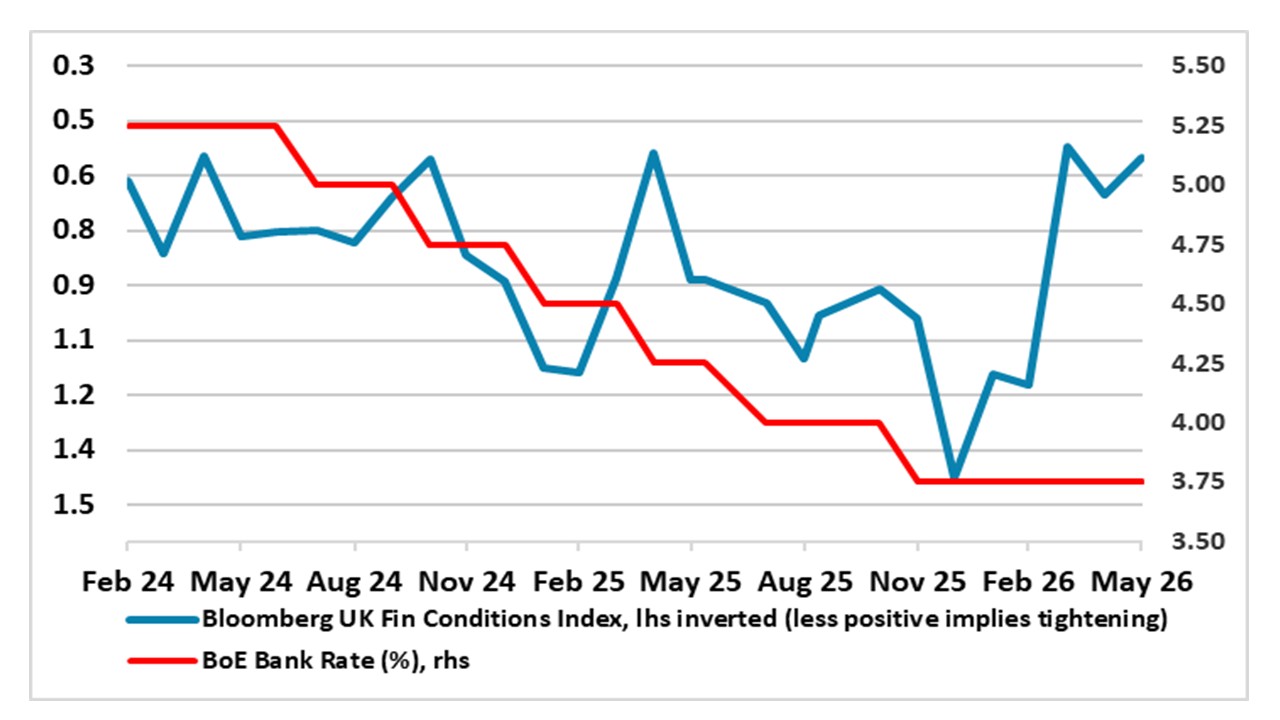

BOE Gang of 6 and Steady 2026 Rates

BoJ Reached One Percent

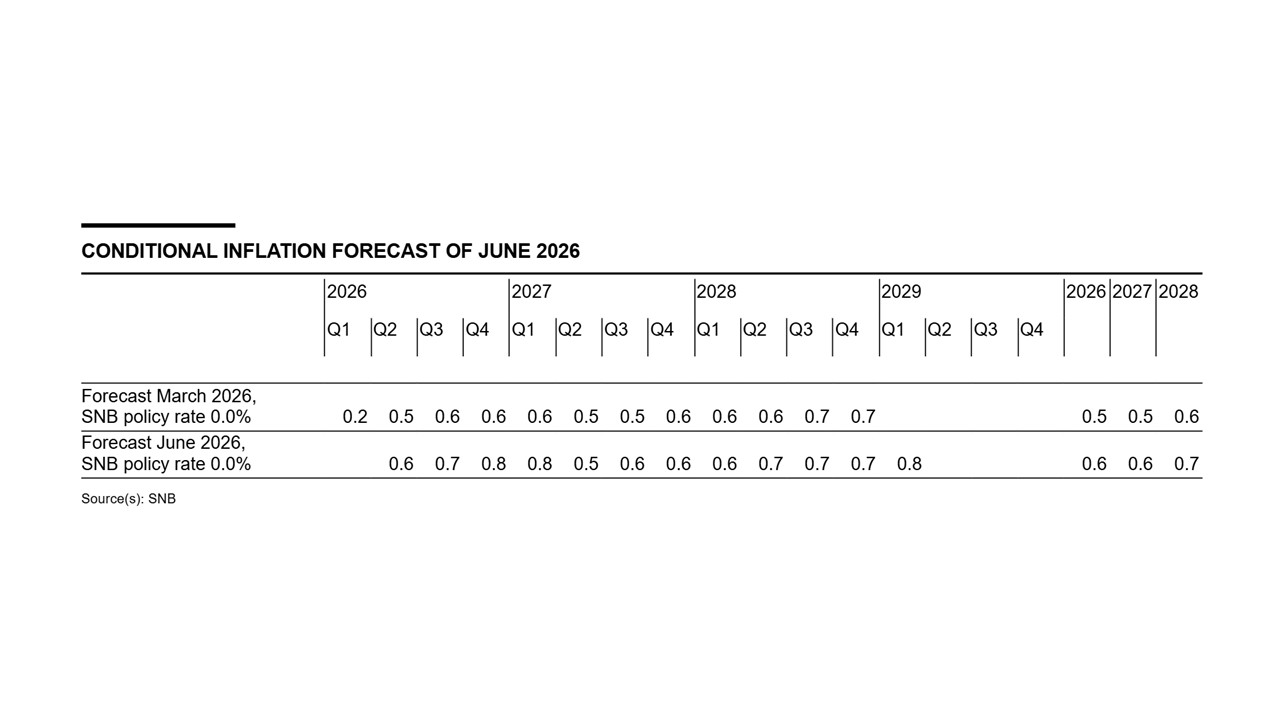

SNB Holding Steady on Rates

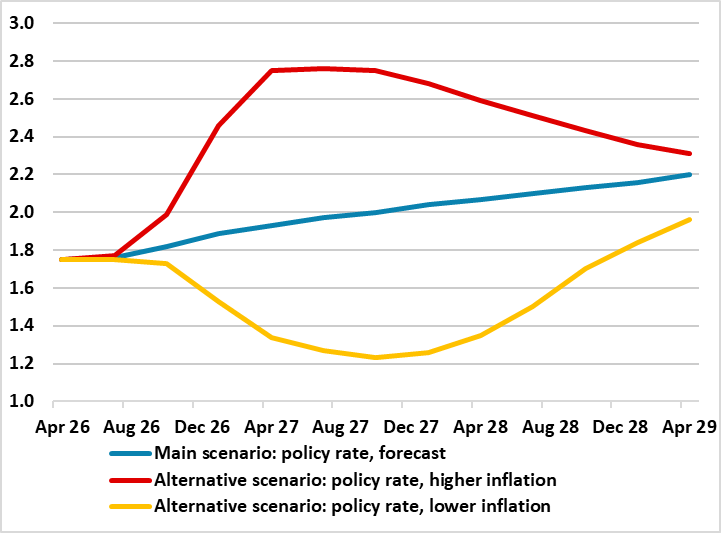

Sweden Riksbank Mild Tightening Bias Persist

The Fed dots show a clearly divided Fed with only a minority on the median rates view for 2026, for a 25bps hike, 2027, which sees a 25bps reversal, and 2027, which sees a further 25bps easing. There are several respondents on either side of the median but we believe the voters lean towards the dovish side. That suggests that under our view of a softening in data in the second half of the year, a rate hike can still be avoided, with 2027 seeing some easing, though it will be a heated debate at the Fed.

Incoming Chair Kevin Warsh has put his stamp on the statement which offers little forward guidance, which left rates unchanged with a unanimous vote. There was some discussion over whether a likely dropping of an easing bias would be replaced with a neutral one or one for tightening. The lack of forward guidance was confirmed by Warsh as a decision the Fed had taken, and one that he had earlier advocated. It is also somewhat convenient for a clearly divided Fed. Getting a reference to productivity growth and capital investment being strong into the statement is also likely to have been at Warsh’s suggestion. Inflation is described as elevated though in stating this is in part due to supply shocks, including for energy, it is not a particularly hawkish take. Activity is described as expanding at a solid pace despite elevated uncertainty. Job growth as keeping pace with the labor force and unemployment as having changed little.

Figure: Official Rate Level Far From the Whole Story

Though Megan Greene joined Huw Pill in calling for a one off 25bps risk management hike, 6 MPC members feel that disinflation is showing through and a soft economy and labor market warrants waiting to see energy prices and potential 2nd round effects. This gang of 6 also feels that markets have tightened financial conditions and wage growth are consistent with the inflation target. With the U.S./Iran interim deal this all argues against a 2026 rate hike. Indeed, as further disinflation comes through, we see the MPC consensus becoming dovish again and delivering 50-75bps of 2027 rate cuts.

The MPC minutes show that 6 MPC members take the view that recent data outturns provided some further evidence that underlying disinflation had been on track pre-conflict. Secondly, that upside risks to energy prices had receded, although they remained higher than pre-war. Finally, that the higher interest rates facing households and businesses were already acting to reduce inflation over time and therefore a hold in Bank Rate at this meeting was appropriate. This all suggests that the gang of 6 are not for hiking in the coming meetings (Catherine Mann was between the two camps, but did not join Greene/Pill in calling for a rate hike). Splits in the individual MPC member statements remain evident and around the three scenarios that the BoE is now projections all based on modest hiking of around 50 bp over the coming year in the April monetary report. Even so, BOE governor Bailey showed only a mild tightening bias, though could fade by the time of the new forecasts scenarios in the July monetary policy report.

As per preview, the BoJ hike rates to 1% in the June 16th meeting as underlying inflation is sustainably around target range with the help of stronger wage growth. It came at a time when Middle East's dust began to settle but the BoJ is already being optimistic beforehand. They believe corporate profit will be sufficient to cushion higher energy prices while government stimulus could help with private consumption.

They acknowledged the artificial compression of headline CPI from government stimulus and admitted the cost push pressure for Japanese business from oil is rising. They are expecting underlying CPI to also surpass 2% in upside risk scenario.

The market focus remain in bond purchase. Our forecast of a pause in the tapering in April 2027 was proven correct. Monthly purchase from then on will be at 2 trillion JPY monthly. While BoJ said long term JGB yields should be determined by market, it is evidentially they will try to not overstress the bond market. Like always, the BoJ will intervene if they see a spike that disrupts the bond market.

The forward guidance has a copy and paste message they want to send, hawkish. But in reality, we believe 1% will be terminal rate, at least before the next spring wage negotiation in March 2027, when if wage traction continues, could see rate to 1.5%.

Figure: SNB Inflation Outlook Little Changed

The June quarterly assessment saw little shift in the forecasts for either growth or inflation (Figure 1), with the tone of the economic outlook remained guarded due to concerns over the Iran war on the global economy (forecasts though look to have been completed before the U.S. Iran deal). With inflation forecast within the confines of its target range (defined officially as less than 2%), this will be enough to justify stable policy now and for some time. We still see policy remaining on hold until at least mid-2027, with only a slight possibility of a return to sub-zero rates given the high(er) bar seen by the SNB for this to occur. The strong Swiss Franc was also mentioned but its current strength needs the context of a still competitive Switzerland.

The SNB noted that CPI has rotated higher with the increase in energy prices and this has marginally pushed the CPI projections higher. Even so, the forecasts appear to have been completed before this week’s U.S./Iran war interim agreement and the near-term multi quarter inflation outlook could be revised down in September. As we have previously noted though the Swiss Franc strength has played a part in keeping inflation under control, weak domestic price pressures is also a disinflation force. Additionally, with a still soft 2026 GDP growth of around 1%, the sports adjusted GDP growth this year may be below 1% and thus some 0.5% below potential. This helps restrains domestic prices.

Figure: Riksbank Policy Rate Outlook Scenarios

Not only at the meeting this, we still see stable policy though to end-2027 rather than the small hikes markets and the Board are now pricing for late 2026. A similar profile has been offered by the Riksbank since last autumn (Figure) and it did bring forward its first hike hint a touch when it presented its updated Monetary policy report alongside this stable verdict. Indeed, in March, it tweaked its forward guidance by suggesting that, even amid Middle East conflict making the outlook very uncertain, it was in a good initial position to adjust monetary policy if required to safeguard the inflation target and no longer pointed to no change for some time to come. Somewhat better data in the last on both the GDP and CPI fronts may even harden this guidance, but underlying inflation is still well below Riksbank thinking while its own survey data and the labour market provide a timely reminder of on-going economic fragility.